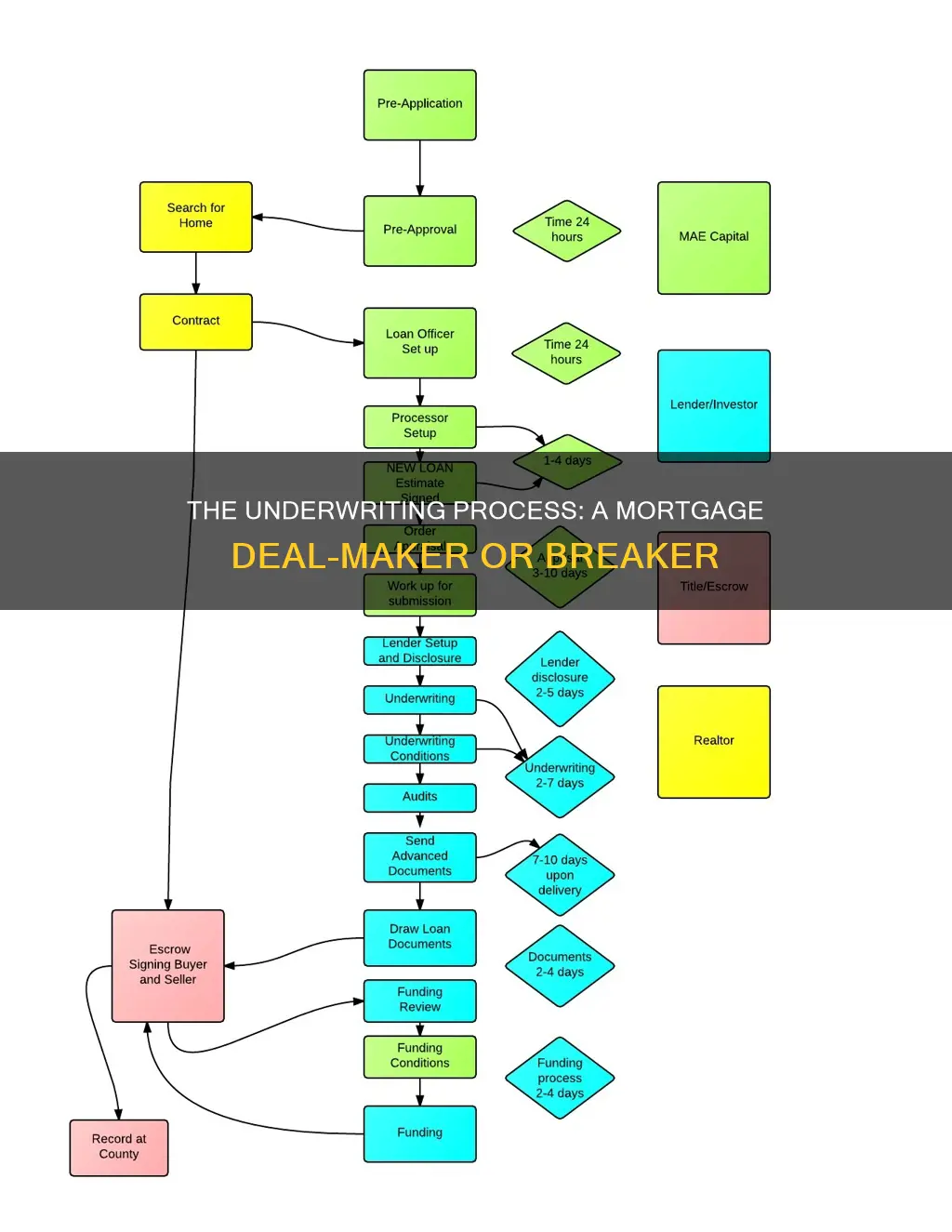

The mortgage underwriting process is an essential step in the home-buying journey, as it determines whether you are eligible for a loan and how much a lender is willing to offer you. The process involves a thorough review of your credit history, employment history, income, assets, and property details. It can take anywhere from a few days to a few weeks, and sometimes even longer, depending on various factors such as the completeness of your application, the type of loan, and the lender's workload. Understanding the underwriting process is crucial as it dictates whether you will get final loan approval, and without this approval, you cannot move forward with purchasing a home.

| Characteristics | Values |

|---|---|

| Importance | The mortgage underwriting process is important for both lenders and borrowers. It helps lenders decide on a borrower's eligibility for loan approval and helps borrowers understand their financial options. |

| Steps | The first step is filling out a loan application, which may be done online, over the phone, or in person. The underwriter then verifies the borrower's identity, checks their credit history, and assesses their finances, including income, assets, investments, debts, and employment history. The underwriter also reviews the property details, including its value and any legal claims. Finally, the underwriter approves or denies the loan application. |

| Timeframe | The mortgage underwriting process can take anywhere from a few days to a few weeks, or even longer in some cases. The timeframe depends on various factors, such as the completeness of the application, the type of loan, the lender's practices and volume of borrowers, and whether additional information or documentation is required. |

What You'll Learn

![]()

The role of the underwriter

Underwriters look at four main areas to get a complete picture of a borrower's financial profile: credit, income, assets, and property details. They review credit history, including payment history, to understand the borrower's past borrowing behaviour and predict their ability to pay back what they borrow. They also assess the borrower's employment history, income documentation, debts, and asset statements to confirm their financial readiness and ability to repay the loan.

Underwriters will also review the type of property the borrower wants to buy, as different properties carry different risks. For example, an investment property is considered riskier because borrowers are more likely to walk away from it in a difficult financial situation than their primary residence.

The underwriter will either approve, deny, or pend the loan application. If approved with conditions, the borrower will need to provide additional documentation such as signatures, tax forms, or prior pay stubs. The underwriter has the power to request additional documents or answers to their questions at any time during the process.

The timeline for the underwriting process can vary from a few days to a few weeks, depending on factors such as the completeness of the application, the borrower's financial situation, the type of loan, and the lender's workload.

Paying Off My Mortgage: Strategies for Faster Freedom

You may want to see also

![]()

The importance of a credit score

The mortgage underwriting process is a crucial step in the home buying journey. It is the process by which a lender decides on a borrower's eligibility for a loan. A mortgage underwriter is responsible for approving or denying a loan application. They do so by assessing the borrower's financial profile, including their credit score, income, assets, debts, and employment history.

A credit score is a significant factor in the mortgage underwriting process as it is a measure of a borrower's reliability. A higher credit score indicates lower risk to the lender, while a lower credit score can make it more difficult to secure a loan. Underwriters review the borrower's credit history, including their payment behaviour on previous loans and credit cards. Late payments, defaults, and bankruptcies can negatively impact the chances of loan approval.

Credit scores are assessed alongside other factors, such as income and assets, to determine the borrower's ability to repay the loan. A stable income and employment history are positive indicators, as they demonstrate the borrower's consistent ability to generate income.

Additionally, a good credit score can help secure a lower interest rate on the loan. A higher credit score signifies lower risk to the lender, which may result in more favourable loan terms. Conversely, a lower credit score may lead to a higher interest rate, making the loan more expensive.

Credit scores are also considered in relation to the loan-to-value (LTV) ratio, which is the mortgage amount compared to the appraised value of the property. A higher LTV ratio indicates a greater risk to the lender, as they could lose more money if the borrower defaults on the mortgage. Therefore, a strong credit score can help balance a higher LTV ratio and increase the chances of loan approval.

In summary, a credit score is a critical factor in the mortgage underwriting process as it helps lenders assess the borrower's reliability and ability to repay the loan. A higher credit score can lead to more favourable loan terms, while a lower score may result in higher interest rates or loan denial. Understanding the importance of a credit score is essential for prospective homeowners as it can significantly impact their chances of securing a mortgage loan.

Private Mortgage Investing: My Path to Getting Rich

You may want to see also

![]()

The need for a home appraisal

The mortgage underwriting process is a crucial step in the home-buying journey. It involves a financial expert, the underwriter, making the ultimate call on whether a borrower is eligible for a loan approval. The underwriter assesses the borrower's financial profile, including their credit history, income, assets, and debts. This process helps determine the borrower's ability to manage future payments and ensures responsible lending.

One critical aspect of the underwriting process is the home appraisal. A home appraisal is an evaluation of the property's worth conducted by a certified appraiser. This appraisal provides critical information for mortgage underwriting by assessing the property's value compared to the loan amount requested. It helps ensure that the borrower is not taking on more debt than the home is worth.

Appraisers inspect the property's interior and exterior, assessing the foundation, roof, electrical, plumbing, and HVAC systems. They also take pictures and measurements to determine the home's condition and features. This detailed report assists lenders and borrowers in making informed decisions about loan terms, interest rates, and necessary repairs. A home appraisal can cost anywhere between $600 and $2,000, and it is typically paid for by the buyer unless negotiated with the seller.

In summary, the home appraisal is a vital component of the mortgage underwriting process as it provides an independent and detailed valuation of the property, ensuring responsible lending and protecting both the borrower and the lender.

Mortgage Reserves: Critical for Home Loan Approval and Peace

You may want to see also

![]()

The time it takes

The timeline depends on various factors, including the complexity of your financial situation, the accuracy and completeness of your documentation, the lender's team structure and experience, and the type of underwriting process used (automated or manual).

For instance, if you are self-employed or have a complex financial history, the process may take longer. Delays can also occur if there are missing or incomplete documents in your application, or if you have made any changes to your credit during the underwriting period. Maintaining a strong credit score and providing necessary documents promptly can help expedite the process.

The lender's workload and practices can also impact the timeline. Some lenders may take longer due to operational inefficiencies or inexperienced staff. Additionally, the use of a manual underwriting process, which is often necessary for borrowers with unique circumstances, can result in a longer evaluation period compared to automated underwriting.

To ensure a smooth and timely process, it is advisable to be responsive to any requests from your loan officer and provide any required documentation as quickly as possible.

The High Cost of Mansion Mortgages: Average or Exception?

You may want to see also

![]()

The documents required

Proof of Identity

A copy of a photo ID, such as a driver's license or government-issued ID, is typically required for most loans.

Income Verification

Lenders will need to verify your income to confirm your financial readiness and ability to make monthly mortgage payments. You will likely need to provide W-2 forms from the last one to two years, pay stubs from the last 30 days, and income tax returns from the last two to three years. If you are self-employed or own a business, you may need to provide additional documents such as profit-and-loss statements, K-1s, balance sheets, and business tax returns.

Employment Verification

The underwriter will need to verify your employment status. They may contact your employer to confirm your employment and cross-reference the income information you provided.

Asset Verification

Underwriters will also review your assets, such as bank statements, investments, or other valuable possessions. Assets can increase your chances of mortgage approval as they demonstrate your financial stability and ability to cover closing costs.

Credit History and Score

Your credit history and score are crucial factors in the mortgage approval process. The underwriter will review your credit report to assess your creditworthiness and predict your ability to repay the loan.

Property Appraisal

An appraisal of the property is almost always required to ensure that the loan amount is in line with the value of the home. A certified appraiser will evaluate the property's worth and condition.

A title search is conducted to ensure there are no liens, claims, unpaid taxes, or other issues with the property. Once the title search is clear, you will need to provide proof of homeowner's insurance to protect against potential damage or loss to the property.

Additional Documents

Other documents that may be requested include a gift letter if you have received financial gifts for the down payment, mortgage statements, tax bills, and homeowner's insurance (if you currently own a home). It is a good idea to ask your lender for a specific list of required documents and start gathering them before beginning the application process.

Freedom Mortgage: My Journey to Requesting It

You may want to see also

Frequently asked questions

The mortgage underwriting process is when a lender decides whether to approve or deny a loan application. The underwriter will review the borrower's financial profile, including credit history, income, assets, debts, and property details.

The mortgage underwriting process can take anywhere from a few days to a few weeks, or even longer. The timeline depends on factors such as the borrower's financial situation, the type of loan, the lender, the current volume of borrowers, and whether any additional information or documentation is required.

A mortgage underwriter is responsible for reviewing the borrower's financial information and making the final decision to approve or deny a loan application. They assess the borrower's creditworthiness, financial stability, and ability to repay the loan.

The underwriter will typically need information about the borrower's income, assets, debts, credit history, and employment history. They may also require additional documentation, such as tax returns, bank statements, and proof of assets.

To improve your chances of approval, it is important to maintain a good credit score, respond promptly to any information requests, and regularly check in with your lender. It is also advisable to protect your credit score and avoid any major expenditures or changes to your finances during the underwriting process.