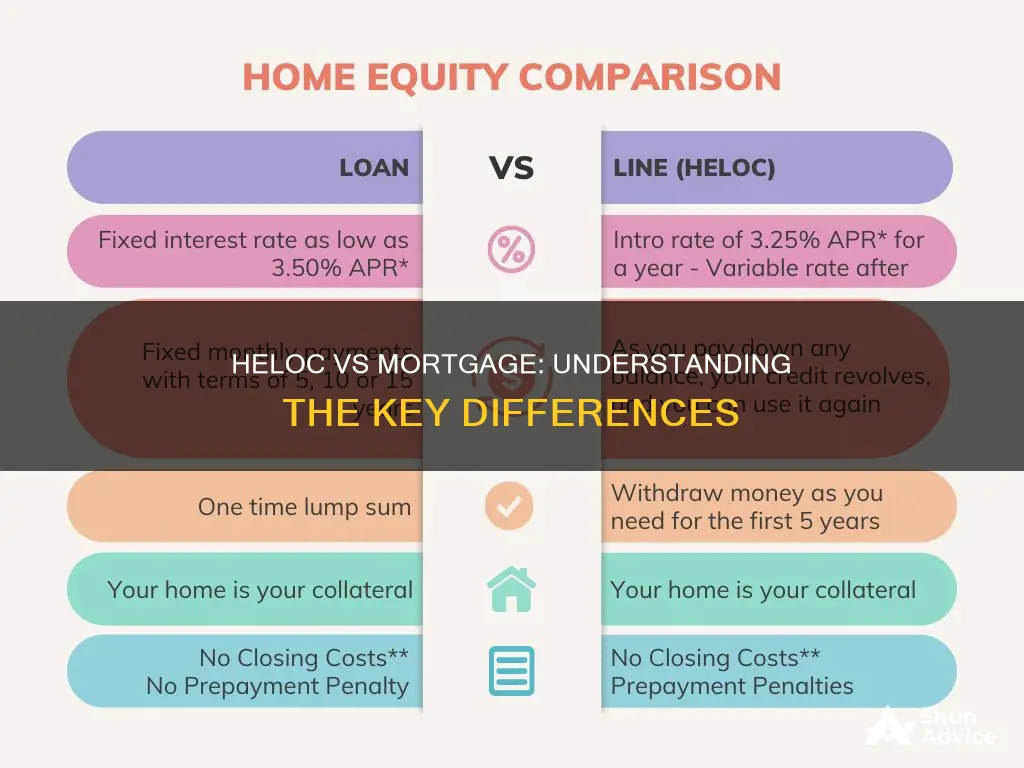

A mortgage is a loan used to buy a property, while a HELOC (Home Equity Line of Credit) is a line of credit borrowed against the available equity of your home. Mortgages are usually paid back over a long period, often 25 years or more, and you receive all the funding upfront. HELOCs, on the other hand, are more flexible, allowing you to access funds up to your credit limit, repay them, and reuse the credit as needed. However, HELOCs can lead to significant debt due to their easy-to-access cash and flexible repayment terms.

What You'll Learn

- Mortgages are primary loans, while HELOCs are secondary loans

- Mortgages are used to buy property, while HELOCs are used to borrow against equity

- Mortgages are larger amounts, while HELOCs are limited by the value of the home

- Mortgages have less flexible repayment terms, while HELOCs are more flexible

- Mortgages are repaid over a long period, while HELOCs are paid off more quickly

![]()

Mortgages are primary loans, while HELOCs are secondary loans

A mortgage is a loan designed to purchase, build on, or refinance a piece of real estate. It is a primary loan used to buy property and covers most of a property's price. Mortgage amounts are often much larger than HELOC amounts, which are limited by an existing home's value. Mortgage repayment terms are typically less flexible than those of a HELOC, and repayment happens on a strictly defined schedule decided by the lender.

A HELOC, or Home Equity Line of Credit, is a line of credit borrowed against the available equity of your home. It is a secondary loan used to borrow against the equity in your home. Your home's equity is the difference between the appraised value of your home and your current mortgage balance. HELOCs are flexible, allowing you to access funds up to your credit limit, repay them, and reuse the credit as needed. However, because of their flexibility, they can lead to significant debt.

Mortgages are considered lower risk to lenders than HELOCs. In the event of default, the mortgage takes priority for repayment, and the home could be at risk. With a mortgage, you receive all the funding upfront and are expected to repay it over a long period, often 25 years or more. On the other hand, a HELOC is a revolving credit line, much like a credit card, that you can draw upon as needed. You only pay interest on the amount you borrow, and there is no prepayment penalty.

While a mortgage is used to purchase a home, a HELOC can be used for various purposes, such as large purchases, unexpected expenses, education costs, or funding home renovations. A HELOC can be obtained even without a mortgage, but it depends on having equity in your home.

Mortgage Pre-Approval: Essential Step for Home Loan Success

You may want to see also

![]()

Mortgages are used to buy property, while HELOCs are used to borrow against equity

Mortgages and HELOCs (home equity lines of credit) are both loans that use your home as collateral. However, they are used for different purposes. Mortgages are used to buy property, while HELOCs are used to borrow against equity.

A mortgage is a loan specifically designed to purchase, build on, or refinance a piece of real estate. It covers most of a property's price and is usually paid back over a long period, often 25 years or more. The repayment terms for mortgages are typically less flexible than those of a HELOC.

On the other hand, a HELOC is a line of credit borrowed against the available equity of your home. Your home's equity is the difference between its appraised value and your current mortgage balance. With a HELOC, you can borrow a portion of your equity and spend it on various expenses, such as large purchases, home improvements, education costs, or debt consolidation. HELOCs offer flexible repayment terms, and you only pay interest on the amount you borrow.

It's important to note that both mortgages and HELOCs have their own set of pros and cons, and it's essential to carefully consider the risks and have a repayment plan before taking out any loan.

Understanding Conversion Mortgage Repayment: What You Need to Know

You may want to see also

![]()

Mortgages are larger amounts, while HELOCs are limited by the value of the home

Mortgages and HELOCs (home equity lines of credit) are both loans that use your home as collateral. However, they differ in several ways, including the amount that can be borrowed. Mortgages are typically larger amounts, designed to cover most of a property's price, whereas HELOCs are limited by the value of the home.

Mortgages are usually primary loans used to buy a property. The amount borrowed is often large, reflecting the high cost of purchasing real estate. For example, a typical mortgage might cover 80% or more of a home's value. This means that mortgage amounts can easily reach hundreds of thousands of dollars or more.

On the other hand, HELOCs are lines of credit borrowed against the available equity of your home. Equity is the difference between the appraised value of your home and your current mortgage balance. Lenders will usually allow you to borrow up to a certain percentage of this equity, which means that the amount is limited by the value of your home. For instance, if you owe money on your mortgage, the maximum HELOC amount you can receive will be smaller.

The difference in amounts between mortgages and HELOCs is also reflected in their repayment terms. Mortgages are typically repaid over long periods, often 25 years or more, with a fixed schedule for repayments. HELOCs, on the other hand, offer more flexibility in repayment terms. You only pay interest on the amount you borrow, and you can repay the balance at any time. However, this flexibility can be a double-edged sword, as it may lead to significant debt if not managed carefully.

In summary, the key difference in amounts between mortgages and HELOCs stems from their nature and purpose. Mortgages are designed to finance the purchase of a property and thus involve larger sums of money. HELOCs, on the other hand, are secondary loans that allow you to access a portion of your home's equity, with the amount limited by the value of your home minus any outstanding mortgage debt.

HECM Mortgage: Death of Owners, What's Next?

You may want to see also

![]()

Mortgages have less flexible repayment terms, while HELOCs are more flexible

A mortgage is a loan designed to purchase, build on or refinance a piece of real estate. Mortgage repayment terms are typically far less flexible than those of a HELOC. When you take out a mortgage, you receive all the funding upfront and are expected to repay it over a long period, often 25 years or more. Repayment happens on a strictly defined schedule that's decided by your lender, and there may be penalties for early repayment.

A HELOC, or home equity line of credit, is a line of credit borrowed against the available equity of your home. It is a revolving credit product secured by your home. This means that you can access funds up to your credit limit, repay them and reuse the credit as needed. You only pay interest on the amount you borrow, and you can make payments or repay the balance at any time. HELOCs are flexible because you can borrow what you need and pay off the entire balance when you want to, without any prepayment penalty. However, this flexibility can lead to significant debt if not managed carefully.

Mortgages and HELOCs both use your home as collateral, but there are important differences between the two. A mortgage is a primary loan, while a HELOC is a second loan or second mortgage. The maximum amount you can borrow with a HELOC depends on the value of your home and your existing mortgage balance. Mortgage amounts are often much larger than HELOC amounts, which are limited by a home's value.

While a mortgage is intended to cover most of a property's price, a HELOC can be used for things like large purchases, unexpected expenses, education costs, and funding home renovations. A home equity loan, or second mortgage, is a separate type of loan that allows you to borrow against the equity in your home. It is typically paid out as a one-time, lump sum, and borrowers make regular payments that cover both interest and principal on a set schedule.

Retirement Savings: Mortgage Application Considerations for Your 401k

You may want to see also

![]()

Mortgages are repaid over a long period, while HELOCs are paid off more quickly

Mortgages and HELOCs (home equity lines of credit) are both loans that use your home as collateral, but they differ in several ways, including repayment terms. Mortgages are repaid over a long period, often 25 years or more, whereas HELOCs are typically paid off more quickly.

Mortgages are designed to cover most of a property's price, so mortgage amounts tend to be much larger than HELOC amounts. With a mortgage, you receive all the funding upfront and are expected to repay it over a long period. Repayment happens on a strictly defined schedule set by your lender, and there may be penalties for early repayment. Mortgages usually offer a choice between fixed-rate and variable-rate options.

HELOCs, on the other hand, are revolving lines of credit that allow borrowers to access funds up to a credit limit, repay them, and reuse the credit as needed. This flexibility can make it easier to fall into significant debt, and interest rates may rise. HELOCs are borrowed against the available equity of your home, and you only pay interest on the amount you borrow. Repayment schedules are more flexible than with mortgages, and there are no prepayment penalties. However, failure to make payments could result in losing your home.

While mortgages are typically used to buy property, HELOCs can be used for various purposes, such as large purchases, unexpected costs, education expenses, or debt consolidation.

Paying Off My Mortgage: Strategies for Faster Freedom

You may want to see also

Frequently asked questions

HELOC stands for Home Equity Line of Credit. It is a line of credit borrowed against the available equity of your home.

A mortgage is a loan specifically designed to purchase, build on or refinance a piece of real estate.

HELOCs are second loans used to borrow against equity, while mortgages are primary loans used to buy property. HELOCs are also more flexible than mortgages, which have less flexible repayment terms.