When it comes to where we live, most people have two options: renting or buying a home. While both refer to payments made to live somewhere, mortgages and rent are very different concepts. This paragraph will introduce the topic by highlighting the differences between renting and taking out a mortgage, and the factors that influence the decision to choose one over the other.

What You'll Learn

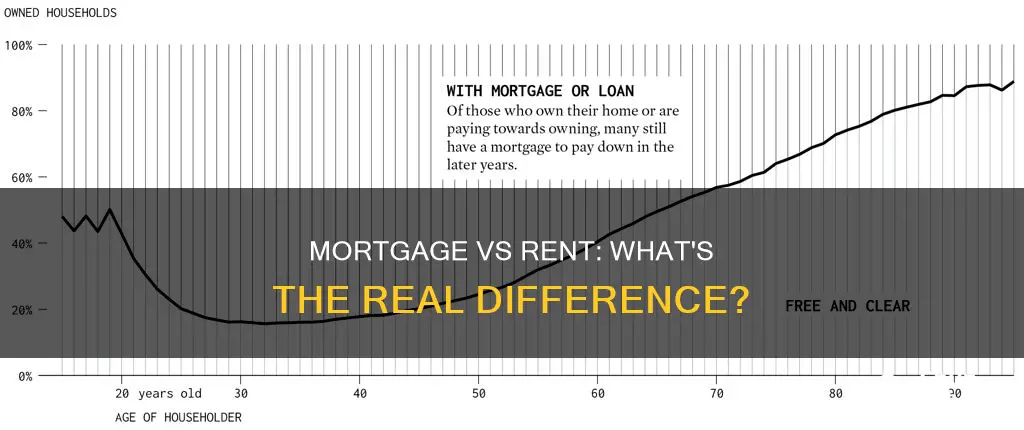

- Mortgages are loans to buy property, whereas rent is a payment for a right to occupy

- Renting offers flexibility, but mortgages provide ownership and more privacy

- Mortgage payments can improve credit scores and produce equity, whereas rent does not

- Renters have little responsibility for maintenance and repairs, unlike homeowners

- Renters may have to pay additional deposits and fees for pets, whereas homeowners can keep pets without restrictions

![]()

Mortgages are loans to buy property, whereas rent is a payment for a right to occupy

Mortgages and rent are very different concepts, although both refer to payments made to live somewhere. A mortgage is a loan taken out to buy property, whereas rent is a payment for the right to occupy a property owned by someone else.

When you take out a mortgage, you become the owner of the property, subject to the conditions of the mortgage documents and other contracts. You are then obliged to pay back the loan over a fixed period, which could be 10, 15, 20 or 30 years. The longer the mortgage period, the smaller the monthly payments, but the more interest you will pay overall. You will also need to make a down payment, which can be up to 20% of the property's asking price, as well as paying closing costs, which can include mortgage application and origination fees, and title and settlement costs.

Renting, on the other hand, involves paying a monthly fee to the landlord or property owner for a specific period, which could be anything from one month to a year or more. The tenant has the right to live in the property during this time, but the landlord may ask for a security deposit, which can be equivalent to one or two months' rent, in case of any damage. Renting offers more flexibility than owning a home, as it is easier to move, and there is little to no responsibility for maintenance and repairs. However, it does not offer the same financial benefits as owning a home, such as building equity and qualifying for tax deductions.

Whether you choose to rent or buy a home will depend on your personal circumstances. Buying a home is often an enormous financial commitment, so it is important to make a well-thought-out decision.

Mortgage Payment Options After a Borrower's Death

You may want to see also

![]()

Renting offers flexibility, but mortgages provide ownership and more privacy

Renting and mortgages are very different concepts, but both refer to payments made to live somewhere. Renting offers flexibility, but mortgages provide ownership and more privacy.

Renting is a payment made to the property owner for the right to occupy the place. The lease agreement can range from one month to several years, and the tenant can negotiate the length of their lease to suit their needs. Renting offers flexibility as tenants can more easily move to a different residence. Renting also comes with little to no responsibility for the property, as the landlord is responsible for repairs and maintenance.

On the other hand, a mortgage is a type of loan used to purchase real property, such as a house or condominium. The homebuyer has to make a down payment, which can be up to 20% of the asking price, as well as cover additional costs such as appraisal and inspection fees. The homeowner's mortgage may last up to 30 years, and they are responsible for all maintenance and repair payments.

While renting offers flexibility, a mortgage provides the benefit of ownership. Homeowners can do what they want on their property without worrying about restrictions, and they have more space to live in compared to renting an apartment. Additionally, mortgages can improve your credit score and produce equity in your home over time, which is not the case with renting.

HECM Mortgage: Death of Owners, What's Next?

You may want to see also

![]()

Mortgage payments can improve credit scores and produce equity, whereas rent does not

While both refer to payments made to live somewhere, mortgages and rent are very different concepts. A mortgage is a type of loan used to purchase real property, such as a house or condominium. The homebuyer has to make a down payment, which can be up to 20% of the house's asking price. On the other hand, rent is a payment made to the property owner in exchange for the right to occupy the place for a specific period.

In addition to a monthly mortgage payment toward the principal balance, homeowners will also pay monthly interest payments at a fixed rate. These home interest payments can be tax-deductible, whereas only some rentals qualify for the same type of deduction.

The decision to rent or buy depends on various factors, including income, cash on hand, and lifestyle preferences. Renting offers flexibility and lower upfront costs, while buying provides ownership, privacy, and freedom to make changes to the property.

Understanding Mortgage Payment Strategies and Management

You may want to see also

![]()

Renters have little responsibility for maintenance and repairs, unlike homeowners

One of the key differences between renting and owning a home is the level of responsibility for maintenance and repairs. Renters typically have little to no responsibility for maintaining the property they are leasing, and they can rely on their landlord to handle any necessary repairs. This can include anything from minor fixes to major projects like roof replacement, as well as appliance upkeep and replacement. Renters also don't have to worry about additional costs for things like homeowner's association (HOA) fees, utilities, lawn and yard maintenance, pest control, or renovations and upgrades.

On the other hand, homeowners are responsible for all maintenance and repair payments, which can be costly and time-consuming. They may also have to pay mandatory monthly or annual HOA fees if their property is part of a homeowners association. In addition, homeowners have to set up and pay for their own utilities, and they are responsible for regular lawn and yard maintenance, including potential costs for landscaping, lawn mowing services, and equipment. Pest control is another expense that falls to the homeowner, and over time, they may need or want to make costly improvements to their property.

The decision to rent or buy depends on a variety of factors, including financial considerations, lifestyle preferences, and personal circumstances. Renting offers flexibility and lower upfront costs, while buying a home provides the opportunity to build equity and take advantage of tax benefits. However, purchasing a home requires a significant financial commitment, and homeowners need to be prepared for unexpected maintenance and repair expenses.

While renting may provide less privacy and freedom than owning a home, it comes with the advantage of lower responsibility for maintenance and repairs, making it a more attractive option for those who cannot afford the upfront costs of buying or are not ready to commit to a particular location. Ultimately, the choice between renting and buying depends on an individual's specific situation and priorities.

HELOC vs Mortgage: Understanding the Key Differences

You may want to see also

![]()

Renters may have to pay additional deposits and fees for pets, whereas homeowners can keep pets without restrictions

When it comes to deciding between renting and taking out a mortgage to buy a home, there are several factors to consider. One notable difference is the freedom that homeowners have when it comes to keeping pets. While renters may face restrictions and additional costs associated with pet ownership, homeowners can generally enjoy the company of their furry friends without such concerns.

Renters often have to pay additional deposits and fees if they want to have pets in their rented property. This is because landlords want to protect their investment and ensure that any potential damage caused by pets is covered. The amount of the pet deposit can vary, but it is typically equivalent to one or two months' rent. This can be a significant expense, especially when combined with other upfront costs of renting, such as the security deposit, application fees, and credit check charges.

On the other hand, homeowners who have a mortgage generally do not have to worry about such restrictions or additional costs. Once they purchase the property, they are free to make changes and decisions regarding their pets without seeking approval from a landlord. This is because they are now responsible for any maintenance and repairs that may be needed due to pet ownership. As long as they comply with any relevant municipal codes or homeowner association stipulations, homeowners can enjoy the companionship of their pets without the added financial burden of pet deposits or rental fees.

It is worth noting that while renting may come with certain limitations and extra costs for pet owners, it can still be a preferred choice for those who cannot afford the upfront costs of buying a home or are not ready to commit to long-term homeownership. Renting provides flexibility and lower maintenance responsibilities, which can be attractive to those who are unsure about their long-term living situation or prefer to avoid the hassle of home maintenance and repairs.

Ultimately, the decision between renting and buying a home depends on various factors, including financial circumstances, lifestyle preferences, and personal priorities. Both options have their advantages and disadvantages, and it is essential to carefully consider all aspects before making such a significant decision.

HELOC vs Mortgage: Interest Calculation Differences Explained

You may want to see also

Frequently asked questions

A mortgage is a type of loan that is used to purchase a property, whereas rent is a payment made to the property owner for the right to occupy the place for a specific period.

When renting, tenants usually pay a security deposit, application fees, and a credit check fee. They may also have to pay additional deposits for pets. When taking out a mortgage, the homebuyer has to make a down payment, which can be up to 20% of the property's asking price, as well as cover closing costs and mortgage-related fees.

Renters usually pay a fixed monthly fee and may have to pay for utilities and renter's insurance. Mortgage payments are also made on a monthly basis and include interest payments, which can be tax-deductible. Homeowners are responsible for maintenance, repairs, and any additional costs associated with owning a home, such as HOA fees and utility bills.

Owning a home provides more privacy and freedom, and homeowners can benefit from tax deductions, improved credit scores, and building equity. Other advantages include having more living space and not having to pay additional deposits or fees for pets.