A mortgage payable is a liability recorded on a company's balance sheet, representing the amount owed to a lender for a mortgage loan. This liability includes both the principal amount borrowed and the interest accrued, but only the principal is considered a mortgage payable. The interest portion is recorded as an expense on the income statement. The mortgage payable account is reduced with each payment made, reflecting the company's decreasing liability. The mortgage payable on the balance sheet can indicate the company's financial health, with high levels of debt potentially causing concern for investors and lenders, while low mortgage payable suggests responsible debt management. This article will explore how mortgage payable is listed on a balance sheet, the factors influencing it, and its implications for a company's operations and financial standing.

| Characteristics | Values |

|---|---|

| What is a mortgage payable? | A liability recorded on the balance sheet that represents the amount of money a company owes to a lender for a mortgage |

| Type of liability | Long-term |

| What does it include? | Both the principal and the interest, but only the principal amount is considered a mortgage payable |

| How is it structured? | Paid back over many years (commonly 15 or 30 years) |

| What is the collateral? | The property |

| What happens if the borrower defaults? | The lender can seize the property and sell it to recover the amount lent |

| How is it recorded on the balance sheet? | As a debit to the asset account, such as "Property, Plant, and Equipment," for the amount of the property or asset being purchased |

| How is it balanced? | As a credit to the liability account "Mortgage Payable" |

| How does it change over time? | As payments are made towards the mortgage, the company records the reduction in the mortgage payable on the balance sheet |

| How are payments recorded? | Each payment made will involve a debit to the "Mortgage Payable" account and a credit to the "Cash" account, reflecting the reduction in liability and the use of cash |

| How does it impact a company's credit rating? | A high level of debt can make lenders hesitant to lend additional funds, while a low mortgage payable can be viewed as a safer investment |

What You'll Learn

![]()

Mortgage payable and a company's credit rating

A mortgage payable is a long-term liability account on a company's balance sheet, representing the amount of money owed to a lender for a mortgage loan. It includes both the principal and any interest accrued, but only the principal portion is considered a mortgage payable. Each payment made towards the mortgage reduces the mortgage payable account on the balance sheet. The interest portion is recorded as an expense in the income statement.

The mortgage payable on the balance sheet reflects a company's financial health and can impact its credit rating. A high mortgage payable may indicate that the company is struggling financially and is taking on significant debt to finance its operations. This could be a concern for lenders, making them hesitant to lend additional funds. On the other hand, a low mortgage payable suggests that the company is managing its debt responsibly, which is favourable for investors and may lead to better lending terms.

Several factors influence the mortgage payable balance sheet:

- Interest rates: Higher interest rates result in higher mortgage payable amounts over the life of the loan.

- Property value: The higher the value of the property purchased, the higher the mortgage payable.

- Economic conditions: Factors such as inflation, unemployment, and interest rates can impact a company's ability to repay its debt.

- Debt repayment schedule: Longer repayment schedules can lead to higher mortgage payable accounts as the principal and interest are spread out over a more extended period.

It is important to note that a company's credit rating is influenced by more than just its mortgage payable. Credit scores are based on credit history, including timely bill payments and total debt. Lenders use credit scores to assess the likelihood of loan repayment and determine interest rates and fees. Therefore, companies should focus on maintaining a healthy balance sheet and efficiently managing their debt obligations to ensure a positive credit rating.

Beating Foreclosure: My Second Mortgage Nightmare

You may want to see also

![]()

Interest rates and property value

Firstly, interest rates play a crucial role in determining the amount of interest a company must pay over the life of the loan. Higher interest rates generally lead to higher mortgage payable amounts. The interest rate, along with the principal amount, determines the monthly or periodic payments that a company must make towards their mortgage loan. The interest portion of the payments is typically calculated based on the outstanding principal balance, with early payments consisting of a larger proportion of interest. As the company makes payments, the interest portion decreases, while the principal portion increases. This dynamic continues until the mortgage is fully paid off.

Secondly, the property value, or the value of the asset purchased using the mortgage payable, directly impacts the balance sheet. A higher-valued property will result in a higher mortgage payable amount. For example, consider a company that purchases a new office building for $1 million and takes out a mortgage loan with a 5% interest rate and a 10-year repayment period. The monthly mortgage payment, including both principal and interest, will be relatively high compared to a lower-valued property.

The interplay between interest rates and property value becomes evident when considering their combined effect on the mortgage payable balance sheet. Higher interest rates coupled with a higher-valued property can significantly increase the mortgage payable amount, potentially impacting the company's financial health. This could lead to concerns about the company's ability to manage its debt obligations and may influence its credit rating and attractiveness to investors.

On the other hand, favourable interest rates and a reasonably valued property can result in a lower mortgage payable, indicating that the company is managing its debt responsibly. This can be a positive signal to investors and lenders, suggesting the company is financially stable and capable of meeting its financial commitments.

In summary, interest rates and property value are critical components in determining the mortgage payable balance sheet. They directly influence the amount of interest and principal a company must pay over the life of the loan, impacting the company's overall financial position and perception in the market.

Understanding Interest-Only Mortgage Amortization

You may want to see also

![]()

Economic conditions

During periods of high inflation, the cost of doing business tends to increase, affecting a company's operational expenses and profitability. This, in turn, may impact the company's ability to service its debt obligations, including mortgage payables. Similarly, high unemployment rates can lead to decreased consumer spending and slower economic growth, potentially reducing a company's revenue and affecting its capacity to repay its debts.

Interest rates are another critical economic factor. Higher interest rates generally result in higher borrowing costs for companies, increasing their overall debt burden. This can be particularly impactful for companies with variable-rate loans, where an increase in interest rates can lead to higher monthly payments and a larger portion of the payments being allocated to interest rather than principal reduction. Consequently, higher interest rates can prolong the repayment period and increase the total cost of the loan.

On the other hand, favourable economic conditions, such as stable inflation, low unemployment, and favourable interest rates, can enhance a company's financial stability and ability to manage its debt obligations effectively. This can lead to a more positive perception among investors and stakeholders, indicating responsible financial management.

In summary, economic conditions are a critical factor in assessing a company's financial health and its ability to manage mortgage payable obligations. Unfavourable economic conditions can strain a company's debt servicing capacity, while favourable conditions can enhance financial stability and positively impact the company's reputation and stock prices.

BPO Report Generation: Mortgage Process Simplified

You may want to see also

![]()

Long-term liability

A mortgage payable is a type of long-term debt used to finance the purchase of property or other assets. The borrower agrees to make regular payments over a set period, typically with interest, until the loan is fully repaid. The lender uses the property or asset as collateral for the loan.

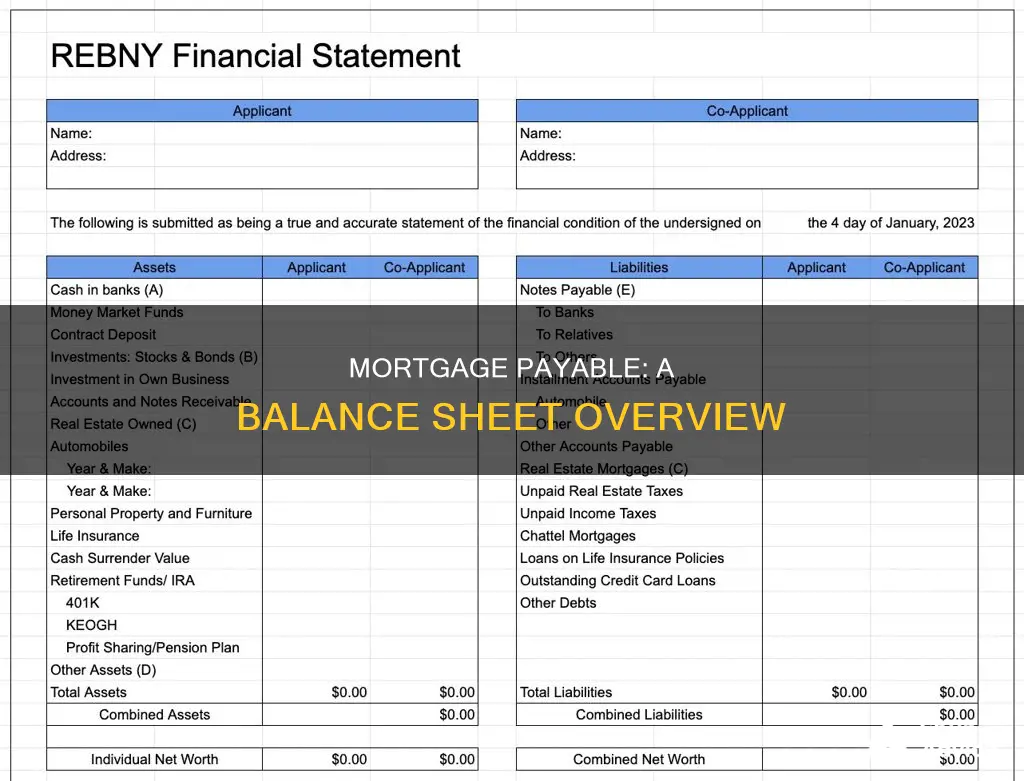

A mortgage payable on a balance sheet is a liability recorded on the balance sheet that represents the amount of money a company owes to a lender for a mortgage. This liability is typically long-term, meaning it will not be paid off within a year. The interest rate on the mortgage payable affects the amount of interest the company must pay over the life of the loan.

To record a mortgage payable on a balance sheet, a company must first determine the total amount of the mortgage loan, including the principal amount and any interest accrued. The company will then need to determine the length of the loan and the interest rate. Once the terms of the mortgage have been established, the accounting entries can be made to record the mortgage payable on the balance sheet. The initial entry will be a debit to the asset account, such as "Property, Plant, and Equipment," for the amount of the property or asset being purchased. This will be balanced by a credit to the liability account "Mortgage Payable."

As payments are made towards the mortgage, the company will need to record the reduction in the mortgage payable on the balance sheet. The interest portion is reported as an expense in the income statement, while the principal payment reduces the mortgage payable liability on the balance sheet. The principal amount owed on a mortgage loan is reported as a long-term liability (or non-current liability) on the balance sheet.

Mortgages: Better Options for a Better Future

You may want to see also

![]()

Current and long-term portions

When it comes to the presentation of mortgage payables on a balance sheet, the current and long-term portions are crucial. These portions are typically classified based on the timing of payments due.

The current portion represents the amount of the mortgage debt that is payable within the next 12 months or the upcoming fiscal year. This includes both the principal amount and any accrued interest that is due to be paid within this period. This current liability is significant as it reflects the company's short-term obligations and their ability to meet them. It provides insight into the company's liquidity and their capacity to manage their immediate financial commitments.

On the other hand, the long-term portion of the mortgage payable represents the amount due after the upcoming fiscal year. This portion is classified as a long-term liability on the balance sheet. It includes the principal amount and the interest that will accrue over the long term. Separating the long-term portion from the current portion is essential for understanding the company's long-term financial health and stability. It provides an indication of the company's ability to manage its debt obligations over an extended period.

The separation of current and long-term portions is crucial for financial statement users, such as investors and creditors, as it offers a more comprehensive understanding of the company's financial health. It allows them to assess the company's liquidity, solvency, and ability to meet its short-term and long-term obligations. This distinction is particularly important for mortgage payables, as they often involve substantial amounts and long repayment periods.

Additionally, the classification of these portions can impact the company's financial ratios and key performance indicators. For example, the current ratio (current assets/current liabilities) and debt-to-equity ratio (total debt/shareholder equity) are commonly used metrics that can be influenced by how the current and long-term portions of mortgage payables are presented on the balance sheet. Proper classification ensures that these ratios accurately reflect the financial health and stability of the company.

Paying Off My Mortgage: Strategies for Faster Freedom

You may want to see also

Frequently asked questions

A mortgage payable is a long-term liability account on a balance sheet that represents the amount of a loan borrowed to purchase real estate that is yet to be paid to the lender.

A high mortgage payable can make lenders hesitant to lend additional funds as it may be seen as high risk. A low mortgage payable can be viewed as a safer investment and may lead to favourable lending terms.

A mortgage payable includes both the principal amount and the interest, but only the principal amount is considered a mortgage payable. The interest portion is reported as an expense in the income statement.

To record a mortgage payable on the balance sheet, a company must first determine the total amount of the mortgage loan, including the principal amount and any interest accrued. The company will then need to determine the length of the loan and the interest rate. Once the terms of the mortgage have been established, the accounting entries can be made to record the mortgage payable on the balance sheet.