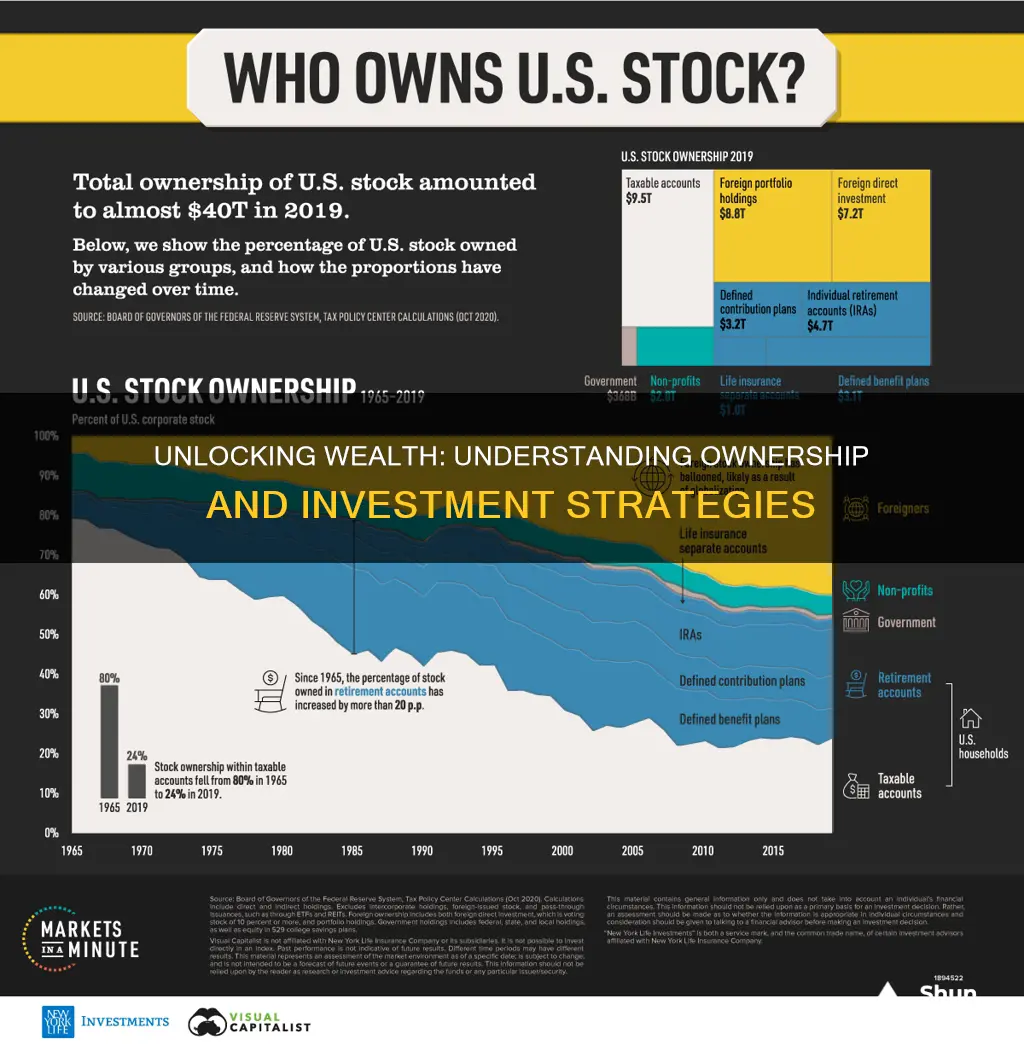

Ownership and investment are fundamental concepts in the world of finance and business. Understanding how these work is crucial for anyone looking to build wealth, whether through personal investments or by owning assets. Ownership refers to the legal right to possess and control an asset, such as a piece of property, a company, or a share of stock. Investment, on the other hand, involves allocating resources with the expectation of generating an income or profit. This can be done through various means, including buying and holding assets, trading financial instruments, or participating in crowdfunding campaigns. The interplay between ownership and investment is complex and dynamic, as the value of an asset can fluctuate based on market conditions, economic factors, and the actions of the owner or investor.

What You'll Learn

- Understanding Ownership: Legal rights and responsibilities of an owner

- Types of Investment: Stocks, bonds, real estate, and more

- Investment Strategies: Diversification, long-term vs. short-term, and risk management

- Market Analysis: Tools and methods for evaluating investment opportunities

- Tax Implications: How taxes affect ownership and investment returns

![]()

Understanding Ownership: Legal rights and responsibilities of an owner

Understanding ownership is a fundamental concept in the world of business and finance, and it involves a complex interplay of legal rights and responsibilities. When an individual or entity becomes an owner, they acquire specific legal rights and obligations that shape their relationship with the asset or company they own. This concept is crucial for investors, entrepreneurs, and anyone involved in business transactions.

The legal rights of an owner are extensive and include the right to use, control, and enjoy the benefits of the owned asset. For instance, a property owner has the right to live in, rent out, or sell their property. Similarly, a shareholder in a company has the right to vote at general meetings, receive dividends, and have a say in major corporate decisions. These rights are often protected by laws and regulations, ensuring that owners have the freedom to utilize their assets while also being held accountable for their actions.

Responsibilities come into play as well, and they are equally important. Owners are typically responsible for the maintenance, upkeep, and management of their assets. For example, a property owner must ensure the property is well-maintained, secure, and complies with local regulations. In the case of a company, owners are responsible for making strategic decisions, managing operations, and ensuring the company's financial stability. This includes fulfilling legal obligations, such as paying taxes, maintaining accurate records, and adhering to corporate governance principles.

The legal framework surrounding ownership often varies depending on the jurisdiction and the type of asset. For instance, real estate ownership laws differ from those governing intellectual property or shares in a company. Understanding these variations is essential for investors and entrepreneurs to navigate the legal landscape effectively. It ensures that owners are aware of their specific rights and duties, helping them make informed decisions and protect their interests.

In the context of investment, ownership rights and responsibilities become even more critical. Investors who purchase shares or assets become partial owners, and their rights and duties extend to the company or entity they have invested in. This includes the right to receive a fair return on their investment, participate in decision-making processes, and hold the company accountable for its performance. Understanding these aspects is vital for investors to make strategic choices and protect their financial interests.

Government Shutdown: Navigating the Investment Landscape

You may want to see also

![]()

Types of Investment: Stocks, bonds, real estate, and more

Understanding the various types of investments is crucial for anyone looking to grow their wealth and achieve financial goals. When you invest, you essentially allocate your money with the expectation that it will generate a return over time. This can be done through various vehicles, each offering different levels of risk and potential reward. Here's a breakdown of some common investment types:

Stocks: This is perhaps the most well-known investment type. When you buy a stock, you are essentially purchasing a small piece of a company. You become a shareholder and have the right to a portion of the company's assets and profits. Stocks are typically traded on stock exchanges, and their prices fluctuate based on market conditions and the company's performance. Investing in stocks can be a powerful way to build long-term wealth, as historically, the stock market has trended upwards over extended periods. However, it's important to note that stock prices can be volatile in the short term, and there's always the risk of losing some or all of your investment.

Bonds: Bonds are a type of investment that represents a loan made by an investor to a borrower, typically a government or corporation. When you buy a bond, you are lending money to the borrower, and in return, they promise to pay you back with interest over a specified period. Bonds are generally considered less risky than stocks, as they provide a steady stream of income through interest payments. The price of a bond can also fluctuate based on interest rate changes and the creditworthiness of the borrower. Government bonds are often seen as a safe haven, while corporate bonds may offer higher returns but with increased risk.

Real Estate: Investing in real estate involves purchasing property, such as land, buildings, or homes. This can be done directly by buying a property and renting it out or indirectly through real estate investment trusts (REITs), which are companies that own and operate income-generating real estate. Real estate investments offer the potential for both income and capital appreciation. Renting out a property can provide a steady cash flow, while the value of the property itself may increase over time, offering a potential return when you decide to sell. However, real estate investments often require a significant amount of capital upfront and can be illiquid, meaning it may take time to buy or sell a property.

Mutual Funds and Exchange-Traded Funds (ETFs): These are investment funds that pool money from many investors to invest in a diversified portfolio of stocks, bonds, or other assets. Mutual funds are typically managed by a fund manager, who makes investment decisions on behalf of the group. ETFs, on the other hand, trade like stocks and can be bought and sold throughout the day. Both offer an easy way to invest in a wide range of assets, providing instant diversification. This can be particularly appealing for beginners or those who prefer a more hands-off approach to investing.

Other Investment Options: There are numerous other investment avenues, including commodities (like gold or oil), derivatives (options and futures), and even peer-to-peer lending. Each of these investment types has its own unique characteristics, risks, and potential rewards. For example, commodities can be a hedge against inflation, while derivatives can be used for speculation or risk management.

In summary, investing is a powerful tool to grow your wealth, but it's essential to understand the different types of investments and their associated risks and rewards. Diversification is often key to managing risk, and consulting with a financial advisor can help you navigate the complex world of investing and make informed decisions based on your financial goals and risk tolerance.

Purchasing CDs with Chase You Invest: A Step-by-Step Guide

You may want to see also

![]()

Investment Strategies: Diversification, long-term vs. short-term, and risk management

Diversification

Diversification is a fundamental investment strategy that involves spreading your investments across various assets, sectors, and geographic regions to reduce risk. The core idea is to avoid putting all your eggs in one basket, as this can lead to significant losses if a particular investment underperforms. By diversifying, you create a balanced portfolio that can weather market volatility and provide more stable returns over the long term.

When constructing a diversified portfolio, consider the following:

- Asset Allocation: Divide your investments among different asset classes such as stocks, bonds, real estate, and commodities. For example, you might allocate 60% of your portfolio to stocks, 30% to bonds, and 10% to real estate.

- Sector Allocation: Invest in various sectors of the economy to reduce concentration risk. Diversify across industries like technology, healthcare, finance, and consumer goods.

- Geographic Diversification: Include investments from different countries and regions to mitigate country-specific risks. Consider global, regional, and local markets to capture growth opportunities worldwide.

Long-Term vs. Short-Term Investment Strategies

Investment decisions often involve a trade-off between long-term growth and short-term gains. Understanding the differences between these strategies is crucial for making informed choices.

- Long-Term Investment: This approach focuses on holding investments for an extended period, typically years or even decades. Long-term investors aim to benefit from compound interest, where returns are reinvested to generate additional earnings. They often ignore short-term market fluctuations and concentrate on the overall growth potential of their investments. This strategy is well-suited for retirement planning, wealth accumulation, and investing in index funds or exchange-traded funds (ETFs) that track broad market indices.

- Short-Term Investment: Short-term investors take a more active approach, aiming to capitalize on market trends and price movements within a relatively brief period. This strategy involves frequent buying and selling of assets, often driven by technical analysis and market timing. Short-term traders may use leverage or derivatives to amplify gains or losses. While this approach can be profitable, it requires a higher level of market knowledge and discipline to execute successfully.

Risk Management

Effective risk management is essential for successful investing, as it helps protect your capital and achieve your financial goals. Here are some key considerations:

- Risk Assessment: Evaluate the risk tolerance of your portfolio by considering factors such as your investment horizon, financial goals, and personal circumstances. Understand the risk associated with each asset class and investment strategy.

- Risk Mitigation: Diversification is a powerful tool for risk management. By spreading investments, you can reduce the impact of individual asset performance on your overall portfolio. Additionally, consider using stop-loss orders to limit potential losses and regularly review and rebalance your portfolio to maintain your desired asset allocation.

- Risk Monitoring: Stay informed about market trends, economic indicators, and news that may affect your investments. Regularly assess the performance of your portfolio and make adjustments as necessary to manage risk and align with your investment objectives.

Invest or Repay Debt: Navigating the Financial Dilemma

You may want to see also

![]()

Market Analysis: Tools and methods for evaluating investment opportunities

Market analysis is a critical process for investors to evaluate and understand the potential of investment opportunities. It involves a systematic examination of various factors that can influence the performance and attractiveness of an investment. Here are some tools and methods to conduct effective market analysis:

- Fundamental Analysis: This approach focuses on evaluating the intrinsic value of a company or asset by examining its financial health and performance. Investors analyze financial statements, including income statements, balance sheets, and cash flow statements, to assess revenue, profitability, debt levels, and overall financial stability. By studying historical financial data, investors can identify trends, growth rates, and potential risks associated with the investment. Fundamental analysis also involves industry research to understand market dynamics, competitive advantages, and future growth prospects.

- Technical Analysis: In contrast to fundamental analysis, technical analysis relies on historical market data and price movements to identify patterns and trends. It involves studying charts, price history, and trading volumes to predict future price movements. Technical analysts use various tools such as moving averages, relative strength index (RSI), and candlestick charts to identify support and resistance levels, potential breakouts, and market sentiment. While it may not provide an intrinsic value, technical analysis is valuable for timing investments and understanding market psychology.

- Industry and Market Research: Conducting thorough industry research is essential to grasp the broader market context. This includes analyzing industry trends, market size, growth rates, and competitive landscapes. Investors can identify dominant players, market share, and potential barriers to entry. Understanding industry dynamics helps in assessing the long-term viability of an investment and its sensitivity to market changes. Market research also involves studying consumer behavior, demographics, and preferences to gauge the demand for a product or service.

- Competitive Analysis: Evaluating competitors is crucial to understanding the investment's position in the market. This involves identifying direct and indirect competitors, assessing their strengths and weaknesses, and analyzing their market strategies. By studying competitors' pricing, product offerings, marketing approaches, and market share, investors can identify potential advantages or disadvantages of the investment in question. Competitive analysis helps in making informed decisions regarding market positioning and strategic responses.

- Data and Statistical Analysis: Utilizing data-driven approaches is essential for making quantitative assessments. This includes collecting and analyzing historical data on stock prices, sales, revenue, and other relevant metrics. Statistical methods can be employed to identify correlations, calculate risk-adjusted returns, and build predictive models. Data analysis provides a more objective view of investment opportunities and can help in backtesting investment strategies.

- Risk Assessment: A comprehensive market analysis should include a thorough risk assessment. This involves identifying and evaluating various risks associated with the investment, such as market risk, credit risk, liquidity risk, and operational risk. Investors should consider both systematic and unsystematic risks and develop strategies to mitigate potential losses. Risk assessment ensures that investors make informed decisions and are prepared for potential challenges.

Effective market analysis requires a combination of these tools and methods, tailored to the specific investment opportunity and the investor's objectives. It is an ongoing process that requires continuous learning, adaptation, and monitoring of market dynamics to make well-informed investment decisions.

ESG Investing: Who's On Board?

You may want to see also

![]()

Tax Implications: How taxes affect ownership and investment returns

Understanding the tax implications of ownership and investment is crucial for anyone looking to grow their wealth and make informed financial decisions. Taxes can significantly impact the returns you receive from your investments, and being aware of these effects can help you optimize your financial strategy. Here's a breakdown of how taxes influence ownership and investment returns:

Capital Gains and Losses: When you sell an asset, such as stocks, bonds, or real estate, for a profit, you incur a capital gain. Conversely, if you sell at a loss, it's a capital loss. These gains and losses are taxable events. For example, if you buy a stock for $100 and sell it for $150, you have a capital gain of $50. This gain is subject to capital gains tax, which varies depending on your income and the holding period of the asset. Short-term capital gains (held for less than a year) are typically taxed at your ordinary income tax rate, while long-term gains (held for more than a year) often qualify for a lower tax rate. On the other hand, if you sell the same stock for $50, resulting in a loss, you can use this loss to offset capital gains or other income, potentially reducing your taxable income.

Dividend and Interest Income: Owning stocks that pay dividends or holding bonds that generate interest income can provide a steady stream of revenue. However, these income sources are generally taxable. Dividend income is typically taxed at ordinary income tax rates, and some dividends may also be subject to a 3.8% net investment income tax for high-income earners. Interest income from bonds is also taxable and is generally treated as ordinary income. Understanding the tax treatment of these income sources is essential, as it can impact your overall investment strategy and tax planning.

Tax-Advantaged Accounts: To minimize the tax impact on your investments, consider utilizing tax-advantaged accounts. For example, contributions to traditional retirement accounts like 401(k)s or IRAs are often tax-deductible, allowing your investments to grow tax-deferred until withdrawal. Additionally, tax-free municipal bonds can generate interest income exempt from federal and state income taxes, making them an attractive option for certain investors. These accounts and investments provide a strategic way to reduce the tax burden on your returns.

Tax Deductions and Credits: Tax laws offer various deductions and credits that can indirectly affect your investment returns. For instance, certain business expenses related to investments, such as trading commissions or investment management fees, may be deductible. Additionally, tax credits for renewable energy investments or education expenses can provide financial benefits. Understanding these deductions and credits can help you optimize your investment strategy and potentially reduce your overall tax liability.

Long-Term Investment Strategies: Tax laws often provide favorable treatment for long-term investments. Holding investments for an extended period can result in lower tax rates on capital gains, as mentioned earlier. Additionally, tax-efficient investment strategies, such as tax-loss harvesting (selling losing investments to offset gains), can help manage your tax liability. It's essential to consider the tax implications of your investment decisions, especially when building a long-term investment portfolio.

Protecting Your Financial Future: Insuring Savings and Investments

You may want to see also

Frequently asked questions

Ownership and investment are related concepts but represent distinct aspects of a business or asset. Ownership refers to the legal right and control of an asset or company, where the owner has the authority to make decisions and derive benefits. This can be in the form of shares in a corporation or real estate. Investment, on the other hand, involves committing money or capital with the expectation of generating a return or profit. It is a strategy to grow wealth over time and can be in various forms, such as stocks, bonds, real estate, or other financial instruments.

Becoming an owner through investment typically involves purchasing assets or shares in a company. When you invest in a business, you are essentially buying a portion of that company, which grants you ownership rights. This can be done through various investment vehicles like stocks, mutual funds, or real estate investment trusts (REITs). By holding these investments, you become a part-owner and may benefit from dividends, capital appreciation, or increased property value over time.

Investing in ownership carries both risks and potential rewards. One of the main risks is the potential loss of capital if the value of the investment decreases. Additionally, there may be liquidity risks, meaning it could be challenging to sell the investment quickly at a favorable price. However, benefits include the potential for long-term wealth creation, income generation through dividends or rental income, and the ability to influence the company's decision-making processes as a shareholder or property owner.