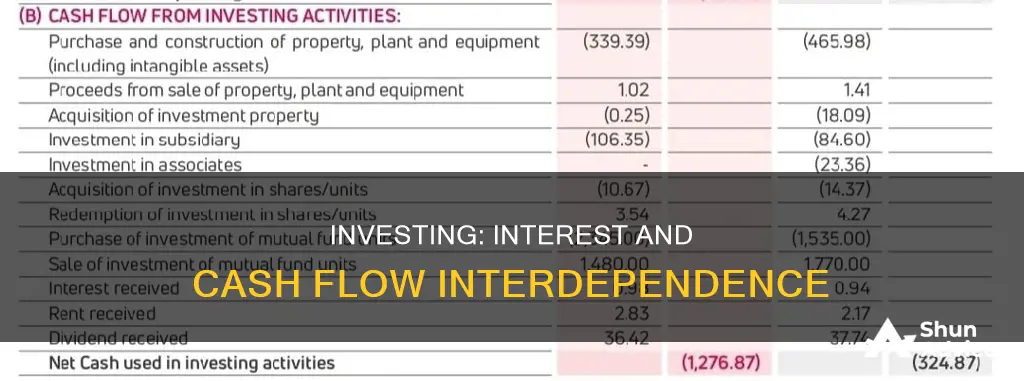

Interest and dividends are a key part of cash flow from investing. Cash flow from investing activities is the section of a company's cash flow statement that shows how much money has been used in (or generated from) making investments during a specific time period. Entities that invest in assets or provide financing to customers as a main business activity are required to classify interest and dividends received as cash flows from investing activities.

| Characteristics | Values |

|---|---|

| Interest payments | Part of cash flow from investing activities |

| Interest received | Part of cash flow from investing activities for entities that do not conduct specified main business activities |

| Interest paid | Part of cash flow from financing activities for entities that do not conduct specified main business activities |

| Interest and dividends | Part of cash flow from investing activities for entities that conduct specified main business activities |

What You'll Learn

![]()

Interest payments or dividends

Interest and dividends received are classified as cash flows from investing activities, while interest and dividends paid are classified as cash flows from financing activities. This distinction is made between entities that invest in assets or provide financing to customers as a main business activity and entities that do not engage in such activities.

For example, cash flows from loans are classified as cash flows from investing activities, even if the reporting entity subsequently reclassifies the loans as held for sale. This concept is known as symmetry.

In financial modelling, it is critical to understand how to build the investing section of the cash flow statement. This includes all income and expenses related to normal business operations, such as debt, equity, or other forms of financing, and the depreciation of capital assets.

Invest Wisely, Live Comfortably Off Your Interest

You may want to see also

![]()

Debt, equity, or other forms of financing

Interest payments are a part of cash flow from investing activities. Cash Flow from Investing Activities is the section of a company's cash flow statement that displays how much money has been used in (or generated from) making investments during a specific time period.

Interest and dividends received are classified as cash flows from investing activities, while interest and dividends paid are classified as cash flows from financing activities. This distinction is made between entities that invest in assets or provide financing to customers as a main business activity and those that do not.

Cash flows from loans are also classified as cash flows from investing activities, even if the reporting entity subsequently reclassifies the loans as held for sale. This concept is known as symmetry.

Therefore, interest is indeed a part of cash flow from investing, and it is essential to have a solid understanding of how to build the investing section of the cash flow statement.

Understanding the Power of Compounding: Doubling Investments

You may want to see also

![]()

Depreciation of capital assets

Interest payments and dividends are part of the cash flow from investing activities. This is the section of a company's cash flow statement that displays how much money has been used in (or generated from) making investments during a specific time period.

Interest and dividends received are classified as cash flows from investing activities, while interest and dividends paid are classified as cash flows from financing activities. This distinction is made between entities that invest in assets or provide financing to customers as a main business activity and entities that do not engage in such activities.

For example, cash flows from loans are classified as cash flows from investing activities, even if the reporting entity subsequently reclassifies the loans as held for sale. This concept is known as symmetry.

Monthly Interest Payments: Do Investments Reap Benefits?

You may want to see also

![]()

Income and expenses related to normal business operations

Interest payments and dividends are classified as cash flows from investing activities. However, this is only the case for entities that do not conduct specified main business activities. For entities that do conduct these activities, interest and dividends received are classified in the operating category.

Cash Flow from Investing Activities is the section of a company's cash flow statement that displays how much money has been used in (or generated from) making investments during a specific time period. This includes cash flows from loans, the purchase of receivables from third parties, and collections from sales of financial assets.

It is critical to have a solid understanding of how to build the investing section of the cash flow statement when conducting financial modelling. This understanding should include all income and expenses related to normal business operations.

Interest Rates, Investments, and Planned Spending: What's the Link?

You may want to see also

![]()

Cash flows from investing activities

Interest payments and dividends are part of the cash flow from investing activities. Cash Flow from Investing Activities is the section of a company's cash flow statement that displays how much money has been used in (or generated from) making investments during a specific time period. Entities that invest in assets or provide financing to customers as a main business activity are required to classify some income and expenses in the operating category that would otherwise be classified in the investing category or the financing category. Cash flows from these loans should continue to be classified as cash flows from investing activities, even if the reporting entity subsequently reclassifies the loans as held for sale.

Maximizing Returns: Strategies for High-Interest Investments

You may want to see also

Frequently asked questions

Cash flow from investing activities is the section of a company's cash flow statement that displays how much money has been used in or generated from making investments during a specific time period.

Cash flow from investing activities includes interest and dividends received, as well as interest and dividends paid. It also includes cash flows from loans, even if the reporting entity subsequently reclassifies the loans as held for sale.

Cash flow from investing activities is distinct from cash flow from operating activities and cash flow from financing activities. Entities that conduct specified main business activities may need to classify some income and expenses in the operating category that would otherwise be classified as investing or financing activities.

Yes, interest payments are included in cash flow from investing activities.

Yes, it's critical to have a solid understanding of how to build the investing section of the cash flow statement. This includes considering all income and expenses related to normal business operations.