Understanding the safe rate for investments is crucial for anyone looking to grow their wealth over time. The safe rate refers to the expected return on an investment that is considered secure and reliable, typically offering a balance between risk and reward. This rate is often influenced by factors such as market conditions, economic stability, and the specific characteristics of the investment vehicle. Investors often seek a safe rate to ensure their capital is protected while still allowing for potential growth, making it an essential consideration in financial planning and portfolio management.

What You'll Learn

- Historical Safe Rates: Past data on safe investment returns over time

- Inflation Impact: How inflation affects the real value of safe investments

- Risk-Free Rate: The theoretical rate of return on risk-free investments

- Market Conditions: Economic factors influencing safe investment rates

- Regulation and Policy: Government rules and policies affecting safe investment rates

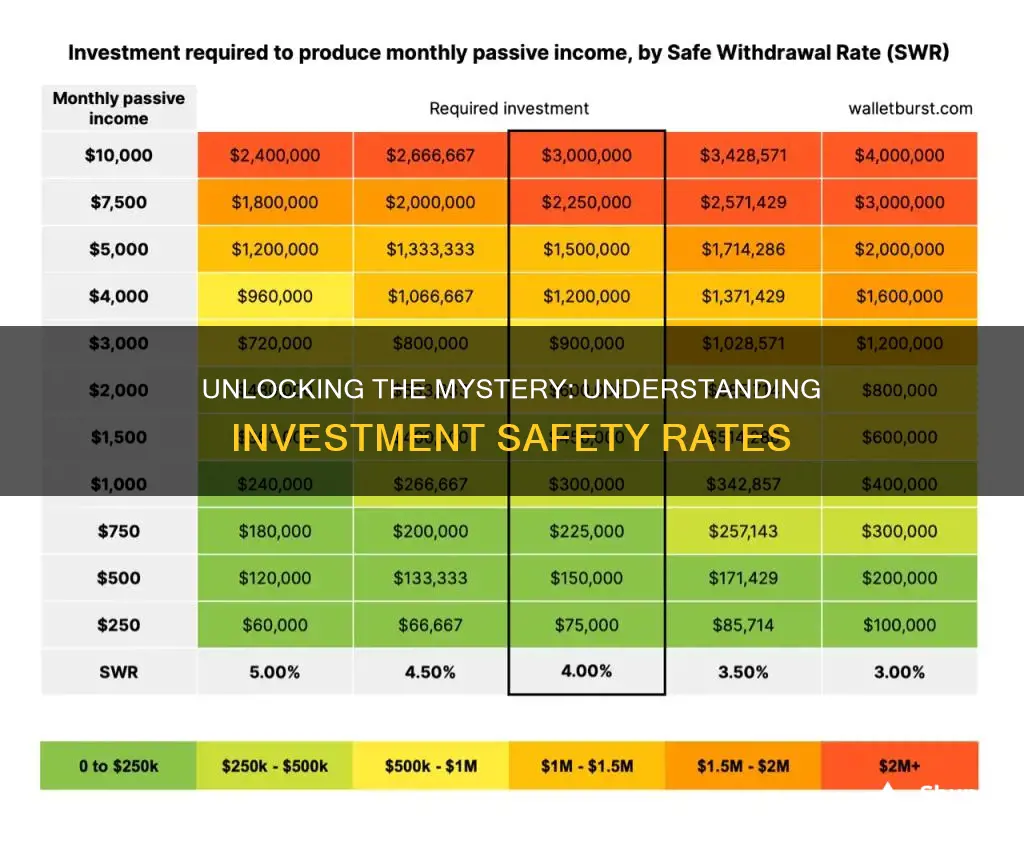

![]()

Historical Safe Rates: Past data on safe investment returns over time

The concept of a "safe rate" for investments is often associated with the idea of a guaranteed return on an investment with minimal risk. While there is no single, universally accepted definition of a safe rate, it typically refers to the long-term average return of a diversified portfolio of low-risk assets. Historically, this safe rate has been a topic of much debate and analysis, as it is influenced by various economic factors and market conditions.

Over the past several decades, the safe rate has been a subject of extensive study and has been influenced by several key factors. One of the most significant influences is the performance of government bonds, particularly long-term Treasury bonds. These bonds are often considered a safe haven for investors due to their low default risk and the perception of government stability. Historically, long-term Treasury bond yields have served as a benchmark for the safe rate, with investors often using these yields as a reference point for evaluating the attractiveness of other low-risk investments.

Data from the past reveals that the safe rate has not remained constant and has fluctuated significantly over time. For instance, during the post-World War II era, the safe rate in the United States was relatively high, often exceeding 5% annually. This was primarily due to the strong economic growth and the high demand for government bonds as a safe investment option. However, in more recent decades, the safe rate has gradually declined, with long-term Treasury bond yields falling below 3% in many developed countries. This trend is partly due to the global shift towards lower interest rates, which has been influenced by factors such as aging populations, technological advancements, and the increasing role of central banks in managing monetary policy.

Another critical aspect of historical safe rates is the impact of inflation. Inflation erodes the purchasing power of money over time, and as such, it plays a significant role in determining the real return on an investment. Historically, the safe rate has often been adjusted for inflation to provide a more accurate representation of the actual return an investor can expect. For example, during periods of high inflation, the nominal safe rate may have been relatively low, but the real return, after accounting for inflation, could have been significantly higher.

Understanding historical safe rates is essential for investors as it provides valuable context for evaluating current investment opportunities. By studying past trends, investors can gain insights into the potential future behavior of safe investments and make more informed decisions. Additionally, this historical perspective can help investors manage their expectations and risk tolerance, ensuring that their investment strategies are aligned with their financial goals and risk preferences.

India Stack: Investing in India's Digital Transformation

You may want to see also

![]()

Inflation Impact: How inflation affects the real value of safe investments

Inflation is a critical factor that significantly influences the real value of safe investments. When inflation rises, it erodes the purchasing power of money over time, meaning that the same amount of money will buy fewer goods and services in the future. This phenomenon directly impacts the returns on safe investments, which are typically expected to provide a stable and predictable income.

Safe investments, such as government bonds, certificates of deposit (CDs), and money market funds, are often considered low-risk options for investors seeking capital preservation and a steady income stream. These investments are generally considered 'safe' because they offer a degree of security and liquidity, especially during economic downturns. However, the real value of these investments is not immune to the effects of inflation.

As inflation increases, the interest rates on safe investments tend to rise as well. This is because lenders and investors demand higher returns to compensate for the loss in purchasing power. As a result, the nominal returns on these investments may appear attractive, but the real returns, after accounting for inflation, can be significantly lower. For instance, if an investor purchases a 5-year government bond with a 3% annual interest rate, and during that period, inflation averages 2.5%, the real return on the investment would be just 0.5%. This means that the investment's real value and purchasing power are effectively reduced.

Over time, this erosion of purchasing power can have a substantial impact on investors. For long-term investors, especially those planning for retirement or other long-term financial goals, the cumulative effect of inflation on safe investments can be detrimental. It may result in a situation where their investments do not keep up with the rising cost of living, leading to a decrease in their standard of living.

To mitigate the impact of inflation, investors can consider a few strategies. One approach is to invest in inflation-indexed securities, such as Treasury Inflation-Protected Securities (TIPS), which are designed to adjust their principal value based on inflation. Another strategy is to maintain a diversified portfolio that includes assets with the potential to outpace inflation, such as real estate or certain stocks. Additionally, investors can regularly review and adjust their investment portfolios to ensure that they are aligned with their financial goals and the prevailing economic conditions, including inflationary pressures.

Oil and Gas Royalties: Safe or Risky Investment?

You may want to see also

![]()

Risk-Free Rate: The theoretical rate of return on risk-free investments

The concept of the risk-free rate is a fundamental principle in finance, representing the theoretical rate of return on investments that are entirely free from risk. This rate serves as a benchmark for evaluating the attractiveness of other investments, as it provides a baseline for assessing the potential returns that can be expected without any associated risk. In essence, it represents the minimum return an investor can expect for giving up their money, which is typically the interest rate on a risk-free asset, such as government bonds.

In the world of finance, the risk-free rate is a crucial concept for several reasons. Firstly, it helps investors and financial analysts understand the minimum return they can expect from an investment without taking on any additional risk. This is particularly important when comparing different investment options, as it provides a standard to measure the potential gains against. For instance, if an investor is considering a bond that offers a 3% risk-free rate, they can use this as a reference point to assess the profitability of other investments.

Secondly, the risk-free rate is a critical component in the calculation of the required rate of return, which is used in the Capital Asset Pricing Model (CAPM). This model is a widely accepted method for estimating the expected return on an investment based on its risk. The CAPM uses the risk-free rate to determine the expected return for an investment with a given level of risk, providing a comprehensive framework for investment analysis.

It is important to note that the risk-free rate is a theoretical concept and may not always be achievable in practice. In reality, no investment is entirely free from risk, and even government bonds, which are often considered the safest, carry some level of risk due to factors like inflation, default risk, and market fluctuations. However, the risk-free rate serves as a valuable tool for financial professionals to make informed decisions and manage portfolios effectively.

In summary, the risk-free rate is a theoretical rate of return that represents the minimum return an investor can expect without taking on any risk. It is a critical concept in finance, providing a benchmark for evaluating investment options and a foundation for more complex financial models. While it may not always be achievable, it remains an essential tool for investors and financial analysts to navigate the complex world of investment decisions.

A Guide to Investing in Microsoft from India

You may want to see also

![]()

Market Conditions: Economic factors influencing safe investment rates

Understanding the concept of a "safe rate for investments" is crucial for investors seeking to balance risk and reward. This rate represents the minimum return an investor expects to achieve without compromising their financial security. It's a critical consideration in a dynamic market, where economic factors play a pivotal role in determining investment safety.

Economic conditions significantly influence the safe rate for investments. During periods of economic growth, central banks often raise interest rates to control inflation. This leads to higher borrowing costs, making fixed-income investments less attractive. As a result, investors might seek alternative investments with potentially higher returns, but these may also carry increased risk. Conversely, in a recession, central banks typically lower interest rates to stimulate the economy, making borrowing cheaper and potentially increasing the appeal of fixed-income investments.

Inflation is another critical economic factor. When inflation rises, the purchasing power of money decreases, eroding the real return on investments. This can prompt investors to seek investments that outpace inflation, such as real estate or commodities. However, during periods of high inflation, the overall market may become less predictable, increasing the challenge of identifying safe investments.

Market volatility also plays a significant role. Volatile markets can lead to unpredictable investment returns, making it difficult to determine a safe rate. Investors often seek investments with a history of stable performance during such periods. This might include government bonds, which are generally considered less risky due to their backing by government entities.

Additionally, global economic events, such as geopolitical tensions or financial crises, can impact investment safety. These events can cause market turmoil, leading to fluctuations in asset prices and interest rates. Investors must stay informed about these events to make informed decisions and adjust their investment strategies accordingly.

In summary, economic factors are pivotal in determining the safe rate for investments. Market conditions, including interest rates, inflation, volatility, and global economic events, significantly influence investment decisions. Investors should carefully consider these factors to ensure their investments align with their risk tolerance and financial goals.

Is Wahed Invest Safe? Unveiling the Truth

You may want to see also

![]()

Regulation and Policy: Government rules and policies affecting safe investment rates

The concept of a "safe rate for investments" is often associated with the idea of earning a reasonable return on an investment while minimizing the risk of loss. This rate can vary depending on various factors, including market conditions, the investor's risk tolerance, and the type of investment. When it comes to government regulations and policies, they play a crucial role in shaping the investment landscape and determining what constitutes a safe rate.

One of the primary ways governments influence safe investment rates is through the establishment of financial regulations. These rules are designed to protect investors and maintain the stability of the financial system. For instance, regulations may require investment firms to provide transparent information about their products, ensuring investors understand the risks and potential returns. This transparency helps investors make informed decisions and can contribute to a more stable investment environment. Additionally, regulations might set standards for the valuation and disclosure of assets, which can impact the overall risk and return expectations for investors.

Government policies also significantly impact interest rates and the cost of borrowing, which in turn affects investment rates. Central banks, often under government control, have the power to set monetary policies, including setting interest rates. Lower interest rates can stimulate investment by making borrowing cheaper, encouraging businesses and individuals to invest. Conversely, higher interest rates might be implemented to curb inflation and stabilize the economy, which could lead to more cautious investment strategies. These interest rate fluctuations can directly influence the safe rate, as investors may seek to match their investment returns with the cost of borrowing or the prevailing interest rates.

Furthermore, tax policies and incentives can shape investment decisions and, consequently, the safe rate. Governments may offer tax benefits or deductions for certain types of investments, encouraging investors to allocate their capital accordingly. For example, tax-advantaged retirement accounts or specific industry-related incentives can attract investors to particular sectors or asset classes. These policies can create a demand for specific investments, potentially driving up their safe rates. On the other hand, tax increases or changes in tax laws might discourage certain investment strategies, leading to a more conservative approach and potentially lower safe rates.

In summary, government regulations and policies have a direct impact on the safe rate for investments. Through financial regulations, interest rate settings, and tax incentives, governments can influence market dynamics and investor behavior. Understanding these regulations and policies is essential for investors to navigate the investment landscape effectively and make informed decisions that align with their financial goals and risk preferences. Staying informed about changes in government policies can help investors adapt their strategies and ensure their investments remain within a safe and sustainable range.

Is Investing in Spying Safe? Unveiling the Risks and Rewards

You may want to see also

Frequently asked questions

The safe rate for investments can vary depending on various factors such as your risk tolerance, investment goals, and the current market conditions. Generally, it is recommended to consider a conservative approach and aim for a rate that aligns with your financial objectives and risk profile. A common strategy is to diversify your investments across different asset classes, such as stocks, bonds, and real estate, to balance risk and potential returns.

Assessing your risk tolerance involves evaluating your financial situation, investment goals, and emotional comfort with market volatility. Consider factors like your age, income stability, and financial obligations. Younger investors might be more inclined to take on higher risks for potential long-term gains, while older investors may prefer more conservative strategies to preserve capital. It's essential to regularly review and adjust your investment strategy as your circumstances change.

While there are no guaranteed safe investments, certain options offer lower risk profiles. These include government bonds, which are typically considered low-risk due to their backing by governments, and savings accounts or certificates of deposit (CDs) offered by banks, which provide a fixed rate of return over a specified period. However, it's important to note that even these options carry some level of risk, and market conditions can impact their performance.

Diversification is a key strategy to manage risk and ensure a safer investment approach. By spreading your investments across various asset classes, sectors, and geographic regions, you reduce the impact of any single investment's performance on your overall portfolio. This strategy helps to balance risk and provides a more stable return over time. Diversification allows you to capture the benefits of different markets and minimize the potential losses associated with a single market downturn.

Regular portfolio reviews are essential to ensure your investments remain aligned with your financial goals and risk tolerance. It is generally recommended to review your portfolio at least annually or whenever there are significant life changes or market shifts. These reviews help you make necessary adjustments, rebalance your portfolio, and ensure that your investments are performing as expected. Staying proactive and informed about your investments is crucial for long-term success.