MOHELA, a student loan servicer, has been at the centre of a debate regarding loan consolidation. Several borrowers have sought guidance from the company on whether or not to consolidate their loans, particularly those with PSLF-qualifying positions. While some MOHELA representatives advised against consolidation, others provided conflicting information, leading to confusion and uncertainty among borrowers. This has sparked discussions on online platforms, with borrowers sharing their experiences and offering advice to one another. The issue of loan consolidation is a complex one, and it appears that even within MOHELA, there may be a lack of consistent and accurate information provided to borrowers.

| Characteristics | Values |

|---|---|

| Consolidating loans before the end of 2023 | Payment count toward PSLF and IDR will be set to zero |

| Consolidating loans after the end of 2023 | Payment count toward PSLF and IDR will be restored |

| Having different loan counts | All loans must be consolidated to be on the same timeline |

| Having split loans (e.g. graduate and undergraduate) | The earliest loans will be given credit |

| Having only Direct Loans | Consolidation is not needed; the payment count will automatically be applied to all loans |

What You'll Learn

![]()

MOHELA advising not to consolidate loans

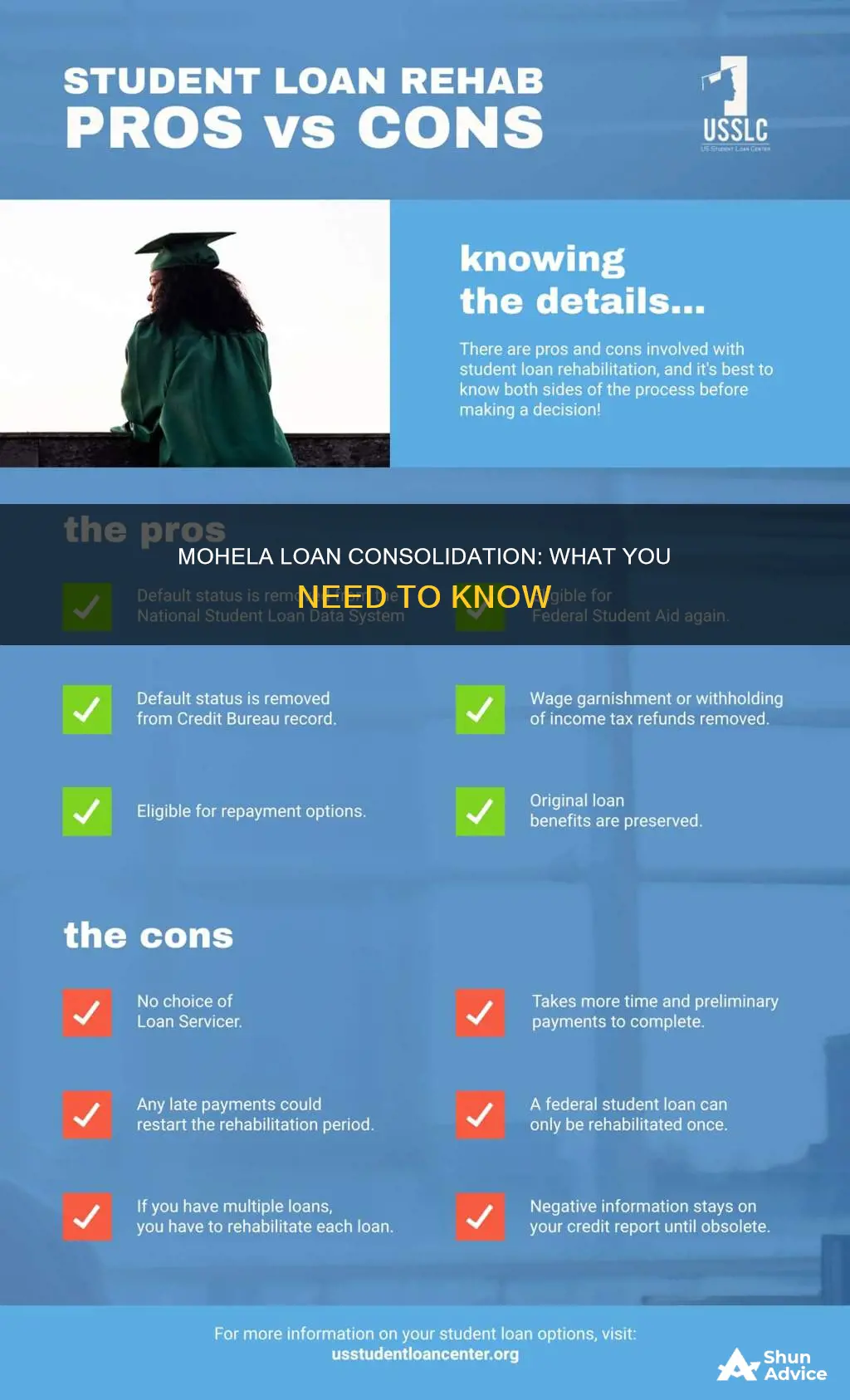

MOHELA, or the Missouri Higher Education Loan Authority, is a US non-profit organisation that assists borrowers in managing their federal student loan debt. While MOHELA does offer loan consolidation services, in certain circumstances, it may advise borrowers against consolidating their loans.

One such scenario is when an individual has already made a significant number of payments towards their loans separately and is close to fulfilling their repayment obligations. In this case, consolidating the loans may reset the payment count to zero, which would be detrimental to the borrower's progress. For example, if a borrower has made 112 out of 120 required payments towards their undergraduate loans and has separate graduate loans, consolidating these loans would mean that the count of 112 payments is lost, and they would have to start their payments anew.

Another reason MOHELA may advise against loan consolidation is if all of a borrower's loans are direct loans. In this case, there is no need to consolidate because the payments made towards one loan will automatically be applied to the others as well. Consolidating direct loans can also result in losing certain benefits associated with the original loan type. For instance, the consolidation standard plan is not eligible for Public Service Loan Forgiveness (PSLF).

It is important to note that there have been reports of MOHELA representatives providing inaccurate or conflicting information. Borrowers are advised to be cautious and well-informed about their specific loan details and requirements before making any decisions regarding consolidation or other repayment strategies. Seeking advice from a PSLF specialist or a financial advisor with experience in student loan management is recommended to ensure borrowers make informed choices about their debt obligations.

Gold Loan Impact: Cibil Score Changes After Manappuram Loan

You may want to see also

![]()

PSLF form submission after consolidation

The Public Service Loan Forgiveness (PSLF) Program is a promise to provide debt relief to teachers, nurses, firefighters, and other public servants by cancelling their federal student loans after 10 years of public service. PSLF removes the burden of student debt, making it possible for borrowers to stay in their jobs and enticing others to work in high-need fields.

To be eligible for PSLF, borrowers must make 120 qualifying student loan payments while working for the government or a nonprofit. Borrowers with loans from the Federal Family Education Loan (FFEL) Program, Parent PLUS loans, or Perkins loans must consolidate these loans to make them PSLF-eligible. However, if you already hold Direct Loans, there is no need to consolidate. Instead, you must verify that you work for an eligible employer and then submit a PSLF form through your loan servicer.

If you have different loan counts and want them to be on the same timeline, you must consolidate everything together. Once your loans are consolidated, you can submit a PSLF form for your current employer directly to Mohela for processing. After Mohela processes the application, you should reach 120 or more qualifying payments and wait for them to finalize the process.

The PSLF Help Tool at StudentAid.gov/PSLF can assist you in certifying periods of employment and tracking your progress toward forgiveness. It is recommended to use this tool to check your employer's eligibility for PSLF before consolidating your loans. Additionally, the Education Department will notify you upon receiving your paperwork, and you are not required to make loan payments while your application is being processed.

M&T Investment Loans: What You Need to Know

You may want to see also

![]()

IDR Waiver adjustment and loan count

The IDR Waiver is a one-time account adjustment by the Department of Education that gives federal student loan borrowers credit toward forgiveness. It was implemented by the Biden Administration and expired on June 30, 2024. The Department of Education originally set a deadline of September 1, 2024, to complete the IDR waiver adjustments in borrowers' accounts. However, this deadline was missed, and adjustments were still being made in January 2025.

The IDR Waiver was beneficial to borrowers as it allowed for a greater number of months spent in student loan repayment or on pause to count toward forgiveness, even if the borrower had never enrolled in an IDR plan before. This included months spent in the three-year pandemic forbearance. It also counted toward the 10-year Public Service Loan Forgiveness (PSLF) program.

To qualify for the IDR Waiver, borrowers needed to consolidate their loans by June 30, 2024. Consolidating loans before the end of 2023 would result in the payment count toward PSLF and IDR being temporarily set to zero, but after the IDR Waiver adjustment, those counts would be restored. If a borrower had split loans, such as graduate and undergraduate loans, they would be given credit for their earliest loans. For example, if they had 118 payments on their undergraduate loans and 30 payments on their graduate loans, the consolidated loan would be given credit for all 118 payments.

It is important to note that consolidating loans may not always be the best option, and borrowers should seek advice from a PSLF specialist or student loan consultant to determine the best course of action for their specific situation.

Loan Reports: Impact on Credit Report and Score

You may want to see also

![]()

Direct vs FFEL loans

Federal education loans are available through the William D. Ford Federal Direct Loan Program ("Direct Loans"). The Federal Family Education Loan Program ("FFEL Program" or "FFELP") is no longer making loans. Direct Loans are available through the Finaid section: Student Loans.

If you have a FFEL Program loan that is not held by ED, you must apply to consolidate your loan into a Direct Consolidation Loan before the one-time account adjustment. Typically, when you consolidate, the payments you made before consolidating won't count toward your IDR forgiveness. However, if you apply to consolidate before the IDR account adjustment occurs, all time spent in repayment before consolidating will count. These payments won't show up on your account until the adjustment officially occurs.

For your FFEL Program loans to qualify for Public Service Loan Forgiveness (PSLF), you must consolidate them into a Direct Consolidation Loan. Only Direct Loans are eligible for PSLF. Normally, when you consolidate, you won’t get credit toward PSLF for the payments you made before you consolidated. However, with the one-time account adjustment, you may get PSLF credit for those earlier payments if you consolidate into the Direct Loan program and meet other PSLF requirements. Keep in mind that this PSLF credit won’t show up on your account until the adjustment officially occurs.

Most FFEL Program loans are eligible for only one income-driven repayment (IDR) plan. However, you can get more IDR options if you consolidate your FFEL Program loan into a Direct Consolidation Loan. IDR plans base your loan payments on your income and family size, and these plans often provide lower monthly payments.

Title Loans in Michigan: What's the Law?

You may want to see also

![]()

Inaccurate information from MOHELA reps

There have been several reports of MOHELA representatives providing inaccurate information to customers. In one instance, a customer was told that they did not need to consolidate their loans, as all of their loans were direct loans, and the 112 payments would automatically be applied to their graduate loans. However, this contradicted information the customer had seen elsewhere, causing confusion and uncertainty. The same customer also reported that MOHELA reps provided conflicting information, first stating that their loans would not be eligible for the benefit and then, after following up for clarification, verifying that the loans would indeed be eligible.

In another case, a customer shared that they were incorrectly informed by MOHELA that consolidating their loans before the end of 2023 would result in the payment count toward PSLF and IDR being set to zero. This information was later corrected by another MOHELA representative, who confirmed that consolidating loans would result in credit for the earliest loans and that consolidation was necessary to receive this credit.

The issue of inaccurate information from MOHELA reps appears to be a recurring theme, with some customers attributing it to a lack of proper training or familiarity with forgiveness programs among the representatives. It is advised that customers seek clarification from multiple sources and specifically request to speak with a PSLF specialist when calling MOHELA to ensure they receive accurate and up-to-date information about their loan consolidation options.

It is important for borrowers to be vigilant and well-informed about their loan details and to not solely rely on the information provided by MOHELA reps. Seeking information from multiple sources, including official government websites and trusted experts in the field, can help ensure borrowers make informed decisions about their loan consolidation and repayment strategies.

Kids and Debt: Are Loans Passed on?

You may want to see also

Frequently asked questions

It is not clear whether Mohela consolidates loans. Some sources indicate that Mohela told borrowers not to consolidate their loans, while others suggest that consolidation is necessary to get certain benefits. It is always recommended to speak to a PSLF specialist for accurate information.

PSLF stands for Public Service Loan Forgiveness.

IDR stands for Income-Driven Repayment.