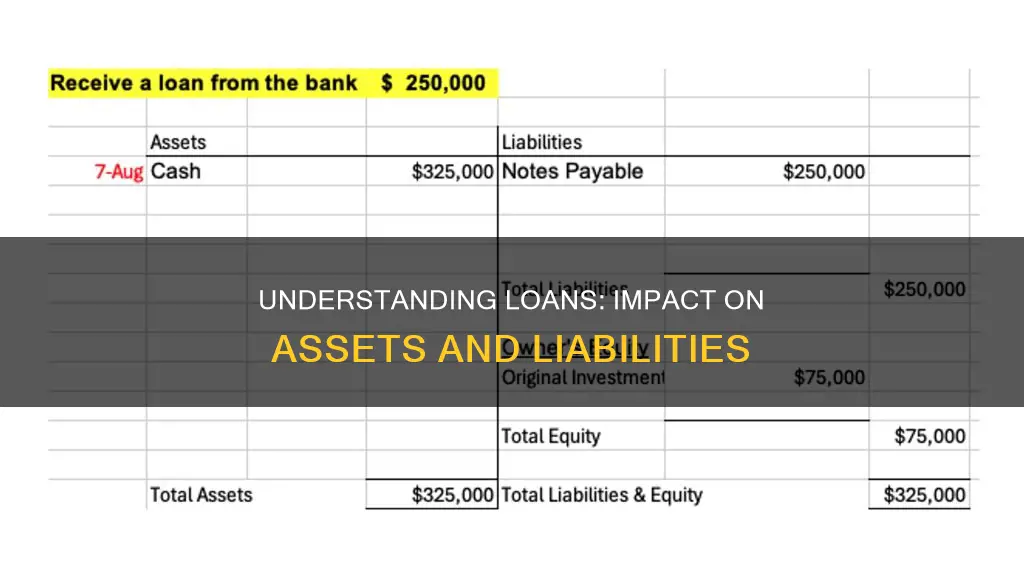

Loans and liabilities are closely related concepts in finance. A loan is a liability because it is a sum of money borrowed by an individual or company that is expected to be paid back, often in monthly instalments, with interest. Liabilities are usually settled over time through the transfer of money, goods, or services. When a company takes out a loan, it increases both its assets and liabilities by the same amount. For example, a company may take out a loan to purchase equipment, which would be recorded as a credit in the long-term debt account and a debit in the company's cash account. This equipment is then considered a fixed asset.

| Characteristics | Values |

|---|---|

| Loans as assets or liabilities | Loans are liabilities, i.e., what you owe to another individual or entity. Assets are what you own or are owed. |

| Types of liabilities | Current liabilities (due within a year), non-current liabilities (due in more than a year), contingent liabilities (may or may not have to be paid in the future) |

| Examples of liabilities | Loans, accounts payable, mortgages, deferred revenues, bonds, accrued expenses, rent, deferred taxes, payroll, pension obligations, warranties |

| Loans and balance sheets | A balance sheet lists a company's total assets and liabilities. A loan increases both a company's assets and liabilities by the same amount. |

| Debt-to-equity ratio | A measure of a company's financial health is its debt-to-equity ratio. A comfortable ratio is 1:1, i.e., $1 in debt for each $1 in equity. |

What You'll Learn

![]()

Loans as a liability

A loan is a liability for both individuals and companies. Liabilities are usually sums of money owed by a person or company, which are settled through the transfer of economic benefits, including money, goods, or services. They are recorded on the right side of a balance sheet and include loans, accounts payable, mortgages, deferred revenue, bonds, warranties, and accrued expenses.

Loans are generally repaid in monthly instalments, with the repayment made from regular income. This creates a cash outflow from future income, leaving less for future expenses and savings. Liabilities can be either long-term or short-term, with the distinction being whether they will be paid off within a year. Long-term liabilities are listed on the balance sheet as obligations but are not due for more than a year. Examples of long-term liabilities include bonds, rent, deferred taxes, payroll, and pension obligations.

For individuals, liabilities include taxes due, bills, rent or mortgage payments, loan interest, and principal due. If an individual borrows money to purchase a car, the loan is a liability, while the portion of the vehicle that they have already paid for is an asset.

For companies, liabilities are amounts owed to suppliers, short-term debt, long-term debt, and total equity contributions and retained earnings. A company's financial health can be assessed by looking at its debt-to-equity ratio, which ideally should be 1:1, meaning the company has $1 in debt for each $1 in equity. Loans can impact this ratio and increase a company's annual debt payments.

Loans: Credit Score Friend or Foe?

You may want to see also

![]()

Loans to increase assets

Loans can be used to increase assets, and this is a common practice for businesses. Asset-based lending involves loaning money with the agreement that the borrower's assets can be seized as collateral if they default on the loan. Lenders prefer liquid assets, such as securities, that can be easily converted to cash, but physical assets such as equipment are also used as collateral. The amount loaned depends on the type and value of the assets offered as security.

For example, a company seeking a $200,000 loan might pledge highly liquid marketable securities on its balance sheet as collateral. The lender may grant a loan equalling 85% of the face value of the securities, so $170,000. If the company pledges less liquid assets, such as real estate or equipment, the lender may only offer 50% of the required financing, so $100,000. In both cases, the discount represents the costs of converting the collateral to cash and its potential loss in market value.

Small and mid-sized companies that are stable and have physical assets of value are the most common asset-based borrowers. However, large corporations may also seek asset-based loans to cover short-term needs, such as an unexpected equipment purchase. For example, a new restaurant might only be able to obtain a loan by using its equipment as collateral.

Businesses may also take out loans to meet routine cash flow demands. For example, a business might obtain a line of credit to cover its payroll expenses if there is a delay in expected payments.

Loans can also be used by individuals to increase their assets. For example, an individual might take out a home loan, which can be beneficial if the asset appreciates in value over time.

Borrowing from Your 401(k): Withdrawal or Loan?

You may want to see also

![]()

Loans for business growth

When a company takes out a loan, both its assets and liabilities increase by the same amount. This is reflected in the company's accounting records, where the loan amount is entered as a credit in the long-term debt account and a debit in the company's cash account.

Loans are often necessary for business growth, especially when a company's regular income is insufficient to fund new projects or expansions. Business expansion loans are a common way for successful businesses to finance their growth and evolve their operations. These loans can be used to invest in a variety of growth projects, such as:

- Opening a new location or expanding into a new market

- Upgrading equipment or purchasing commercial real estate

- Hiring new team members

- Increasing inventory or fixed assets

- Generating new revenue streams

When considering a loan for business growth, it is important to assess the financial health of the company. A key indicator is the debt-to-equity ratio, which ideally should be 1:1, indicating that the company has $1 in debt for each $1 in equity. Lenders will also consider the business's ability to repay the loan, its credit history, and whether it meets size standards and legal requirements.

Business expansion loans are available from traditional lenders, as well as SBA lenders, online lenders, and nonprofit lenders. Some loans, such as those from the SBA, may offer unique benefits like lower down payments, flexible overhead requirements, and no collateral. It is essential to compare different loan options and understand the eligibility requirements and restrictions on fund usage.

Loans and Net Worth: A Complex Relationship

You may want to see also

![]()

Loans for personal assets

When considering taking out a loan, it is important to understand how it will impact your financial situation. Loans can be used to increase assets, but they also increase liabilities. A loan is a liability because it is an amount owed, often with interest, to a lender. This liability is increased over time as interest accrues on the loan.

Personal loans are typically used to borrow a lump sum of money, which is then repaid in monthly instalments over a fixed term. These loans can be used for a variety of purposes, such as making a large purchase, consolidating debt, or covering unexpected expenses. Personal loans can be secured or unsecured. A secured loan requires collateral, such as a vehicle or savings account, which can be seized by the lender if the borrower defaults on the loan. Unsecured loans do not require collateral, but generally have higher interest rates.

The impact of a loan on a person's assets and liabilities can be seen in their accounting equation. When a loan is taken out, the amount is recorded as a credit in the long-term debt account, increasing liabilities. The corresponding debit is made to the cash account, increasing the person's assets. As the loan is repaid, the cash account is credited and the long-term debt account is debited, reducing assets and liabilities by the same amount.

Taking out a loan to purchase an asset can be beneficial if the asset appreciates in value over time, such as in the case of a home loan. However, it is important to consider the financial implications of taking on debt, as the increased liabilities may impact a person's ability to save or invest in the future. It is also crucial to develop a repayment strategy to ensure the loan can be comfortably repaid and to avoid debt traps.

Life Insurance Loan: Impact on Premium Payments?

You may want to see also

![]()

Loans and debt management

For individuals, liabilities often include taxes, bills, rent or mortgage payments, loan interest, and principal due. An individual may also take out a loan to purchase a car or a home, in which case the loan is a liability, and the portion they own is an asset. Personal loans or credit card loans to meet regular expenses may indicate inefficient financial management and can lead to debt traps. However, liabilities taken to purchase assets can be beneficial if the asset appreciates over time, such as in the case of a home loan.

Businesses often take out loans to fund equipment purchases or expand their operations. For example, a company may borrow money to purchase equipment for its production line, recording the loan as a long-term debt and the equipment as a fixed asset. The proportion of debt to equity is a measure of a company's financial health, with a 1:1 ratio being generally comfortable. Companies also incur long-term liabilities such as rent, deferred taxes, payroll, and pension obligations.

Effective debt management is crucial for both individuals and businesses. It involves prudently balancing debt and equity to ensure financial stability and the ability to meet repayment obligations.

Frequently asked questions

Taking a loan can increase a company's assets and liabilities. A loan is considered a liability because it is something that is owed to another party. When a company takes out a loan, the bookkeeper records a credit in the amount of the loan into the long-term debt account (liability) and a debit to the company's cash account (asset).

Assets are things that you own or are owed to you, while liabilities are things that you owe to someone else.

Liabilities include loans, accounts payable, mortgages, deferred revenues, bonds, warranties, and accrued expenses.

Assets include cash in banks, accounts receivable, inventory, and fixed assets.