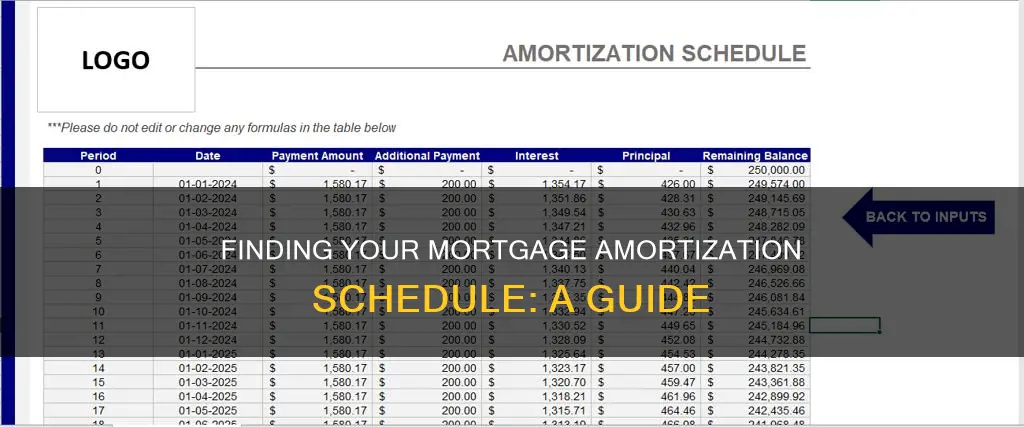

Amortization is the process of paying off a loan over time in predetermined installments. An amortization schedule is a document that keeps track of the progress of your mortgage home loan over time. It will show the original loan amount, interest rate, term (i.e., time frame), and the remaining loan balance after each payment. It is a table that lists how many monthly mortgage payments you’ll make, the amount you’ll be sending to your lender with each payment, and how much will go toward principal and interest.

| Characteristics | Values |

|---|---|

| Definition | A document that keeps track of the progress of your mortgage home loan over time |

| Purpose | To show the original loan amount, interest rate, term (i.e., time frame), and the remaining loan balance after each payment |

| Benefits | Budgeting, transparency, potential tax deductions, and the possibility of early repayment |

| Components | Monthly payment, the amount allocated toward the loan's principal balance, and the amount allocated to pay off interest |

| Calculation | Based on the loan amount, interest rate, and loan term |

| Types of Loans | Fixed-rate loans, adjustable-rate mortgages, variable-rate loans, and lines of credit |

| Extra Payments | Basic amortization schedules do not account for extra payments, but borrowers can make them to reduce the loan term and total interest costs |

| Online Access | Available through online banking services, such as U.S. Bank's "View, pay & manage" feature |

What You'll Learn

![]()

How to read an amortization schedule

An amortization schedule is a table that lists each monthly payment from the time you start repaying the loan until the loan matures or is paid off. It is a powerful tool that can help you budget, understand the full cost of the loan, and make better financial decisions.

To read an amortization schedule, start by locating the “Date" column, which tells you when each loan payment is due. Typically, loan payments occur once a month, on the same day of each month, making it easier for borrowers to remember the payment dates. Next, refer to the “Days" column for information on the number of days that the payment covers.

The “Payment" and “Interest percentage" columns are also essential. While these columns generally remain constant over the course of the loan, the final payment amount may differ due to the mathematics involved in setting up the loan payment amounts.

The most informative columns in the amortization schedule are the “Interest" and “Principal" columns. Each payment listed in the "Payment" column is divided into these two components. The interest payment is applied to the total interest charged for the loan and decreases with each payment, while the principal payment goes toward the actual money borrowed and increases with each payment. Regardless of these changes, the interest and principal amounts will always equal the value in the "Payment" column.

Additionally, the amortization schedule may include information on mortgage insurance, the remaining balance after each payment, and the loan-to-value ratio (LTV ratio), which reflects the outstanding loan balance divided by the purchase price.

Applying for Mortgage Relief: A Step-by-Step Guide

You may want to see also

![]()

How to create an amortization schedule

An amortization schedule is a table that lists each monthly payment from the time you start repaying the loan until the loan matures or is paid off. The schedule details how much will go towards each component of your mortgage payment, the principal, or the amount you borrowed, and the interest, or the cost of borrowing charged by lenders.

To create an amortization schedule, you will need to know the monthly payment on the loan. Take the total amount of the loan and multiply it by the interest rate on the loan. For a loan with monthly repayments, divide the result by 12 to get your monthly interest. Subtract the interest from the total monthly payment, and the remaining amount is what goes toward the principal. For the second month, do the same thing, but start with the remaining principal balance from the first month instead of the original loan amount. Repeat this process until you reach the end of the loan term, by which time your principal should be at zero.

There are also online amortization calculators that can help you with this process. You can input your loan amount, interest rate, and repayment term, and the calculator will generate an amortization schedule for you.

Enhancing Your Mortgage: Strategies for Financial Empowerment

You may want to see also

![]()

How to use an amortization calculator

An amortization calculator is a powerful tool that can help you understand your loan repayment process and make better financial decisions. Here's a step-by-step guide on how to use an amortization calculator:

Step 1: Understand Amortization

Amortization refers to the process of paying off a debt or loan over a fixed period of time in predetermined, equal installments. Each payment consists of two parts: the interest due on the loan and the principal amount, which is the unpaid loan balance excluding any interest or fees.

Step 2: Gather Loan Information

To use an amortization calculator, you will need to have specific details about your loan. This includes the loan amount, the length of the loan (also known as the loan term), the interest rate you are being charged, and the start date of the loan, which is usually the month of your first payment.

Step 3: Input Information into the Calculator

Once you have an amortization calculator, input the information gathered in Step 2. Enter the loan amount, loan term, interest rate, and loan start date into their respective fields. Ensure that the information is accurate to obtain precise calculations.

Step 4: Review the Amortization Schedule

After inputting the loan details, the calculator will generate an amortization schedule. This schedule is typically presented as a table, chart, or graph. It will outline the breakdown of each periodic payment, showing how much goes towards the interest and how much reduces the principal balance over time.

Step 5: Analyze the Schedule

Understanding how to read the amortization schedule is crucial. Early in the loan term, you will notice that a larger portion of each payment covers the interest due to the higher loan balance. As time progresses, the interest portion decreases, and a larger amount is allocated to reducing the principal amount. The schedule will also help you identify the total interest cost, which is essential for tax deductions and comparing loan offers.

Step 6: Make Financial Decisions

The amortization schedule provides valuable insights for financial decision-making. It helps with budgeting by showing exactly how much you owe each month. Additionally, understanding the total cost of the loan, including interest, empowers you to compare it with other loan offers. If you wish to accelerate your loan repayment, the schedule can also help you determine how much extra you can pay towards the principal.

By following these steps and utilizing an amortization calculator, you can effectively manage your loan repayment process and make informed financial choices.

Commercial Mortgage Application: A Step-by-Step Guide

You may want to see also

![]()

How to view your amortization schedule online

An amortization schedule is a document that keeps track of the progress of your mortgage home loan over time. It will show the original loan amount, interest rate, term (i.e., time frame), and the remaining loan balance after each payment. This is a powerful tool that can help you with budgeting, transparency, tax deductions, and early repayment.

To view your amortization schedule online, the process may vary depending on your bank. As an example, for U.S. Bank account holders, you can follow these steps:

- Select your mortgage account from the dashboard.

- If you have multiple U.S. Bank accounts, choose "View and manage". If you only have a mortgage, choose "View, pay & manage".

- For online banking users, select "My Loan" at the top of the page.

- Locate the "Amortization schedule" section and select "More details".

- A pop-up window will appear with your amortization schedule.

You can also use an amortization schedule calculator to view your schedule online. To do this, you will need to input the following information:

- Starting loan amount.

- Interest rate.

- Starting loan length (term).

Using this information, the calculator will be able to generate an amortization schedule for you. This can be a useful tool to estimate how much of each payment reduces your loan balance and how much goes to interest. Additionally, you can use the calculator to see the impact of making extra payments on your loan term and interest savings.

Applying for Mortgage Assistance: A Step-by-Step Guide

You may want to see also

![]()

How amortization works with adjustable-rate loans

An adjustable-rate mortgage (ARM) is a home loan with a variable interest rate. This means that the interest rate can change over time, which is different from a fixed-rate mortgage, where the interest rate remains the same for the entire loan period.

With an ARM, the initial interest rate is typically fixed for a certain period, usually between three and ten years, and is generally lower than the rates offered on fixed-rate mortgages. This is known as the \"initial rate period\" or \"introductory period\". After this period, the interest rate adjusts periodically, typically once a year or every six months, and can either increase or decrease depending on a benchmark index, such as the Secured Overnight Financing Rate (SOFR). This index reflects the broader market conditions and economic state.

The interest rate on an ARM is determined by the benchmark index and a fixed margin or \"margin amount\" charged by the lender. For example, if the index is 5% and the margin is 2%, the interest rate on the mortgage will adjust to 7%. The margin amount remains the same throughout the loan, but the index can fluctuate, causing the interest rate to vary.

ARM loans usually have two phases: the initial fixed-rate period, followed by an adjustable phase where the interest rate can move up or down. The frequency of these adjustments is specified by the lender and can vary from every six months to yearly or even monthly intervals. It is important to carefully read the terms and conditions of an ARM loan, as the potential for rate increases can make budgeting difficult and strain finances, especially if there are no rate caps in place.

In terms of amortization, which is the process of gradually paying off a debt through regular payments, all ARMs function on a 30-year amortization schedule. This means that it will take 360 months to pay off the loan in full, regardless of changes in the interest rate. However, it is important to note that some ARMs can lead to negative amortization, where the monthly payments are not sufficient to cover the interest rate, causing the amount owed to increase even when payments are made.

Choosing a Mortgage: What You Need to Know

You may want to see also

Frequently asked questions

An amortization schedule is a document that keeps track of the progress of your mortgage home loan over time. It shows the original loan amount, interest rate, term (i.e., time frame), and the remaining loan balance after each payment. It is a table that lists how many monthly mortgage payments you’ll make, the amount you’ll be sending to your lender with each payment, and how much will go towards principal and interest.

You can use an online amortization schedule calculator to calculate your amortization schedule. You will need to input the loan amount, the length of the loan, the interest rate, and the loan start date.

An amortization schedule can help with budgeting, as you will know exactly how much you owe each month. It also allows you to see the total interest cost, so you can understand the full cost of the loan and compare it against other loan offers. It can also help you to understand your tax deductions and see how reducing the loan balance with early payments can cut your total interest costs and shorten the loan term.

An amortization schedule is a table that shows your monthly payment, how much of it is allocated towards your loan’s principal balance, and how much will be allocated to pay off interest. An amortization calculator helps you understand how fixed mortgage payments work by showing you how much of each payment reduces your loan balance and how much goes to interest.