An annuity can be a great source of income to qualify for a mortgage or a reverse mortgage. The income from an annuity can be used to cover your mortgage payments every month. An annuity mortgage is popular with first-time buyers as it offers lower net costs at the beginning, with the expectation that the buyer will earn more over time. The monthly annuity income is added to other income sources to determine the mortgage one can afford. This approach can be used to generate a consistent cash flow to cover monthly mortgage payments.

| Characteristics | Values |

|---|---|

| Definition | A contract issued and distributed by an insurance company and bought by individuals. |

| Payment | A series of payments made at equal intervals based on a contract with a lump sum of money. |

| Payment Frequency | Weekly, monthly, quarterly, yearly, or at any other regular interval of time |

| Types | Fixed, variable, immediate, deferred, contingent, equity-indexed, annuity-due, annuity-immediate, ordinary, life, perpetuity, guaranteed, and more. |

| Uses | Retirement, death benefits, regular deposits to a savings account, monthly mortgage payments, insurance payments, pension payments, etc. |

| Qualification for Mortgage | Monthly annuity income is added to other income sources to determine the mortgage one can afford. |

| Tax Advantages | Earnings are not taxed until they are withdrawn from the account, allowing for tax-deferred growth. |

What You'll Learn

![]()

Annuity as a source of income to qualify for a mortgage

An annuity can be a great source of income to qualify for a mortgage to buy a home or for a reverse mortgage. It is a type of insurance contract that, after an initial premium, provides a guaranteed income stream now or in the future. The income from an annuity can be used to cover your mortgage payments month after month. This is because both the income from an annuity and the liability payments on a mortgage are consistent and predictable.

When you pair a mortgage payment with an annuity, it creates a conduit between an income source and a particular expense. By using an annuity aligned with the costs of the mortgage, you can guarantee enough steady income to cover principal and interest or more. For example, a 10-year multi-year guaranteed annuity (MYGA) can generate consistent cash flow, effectively covering a $1,250 monthly mortgage payment.

It is important to note that if you received a lump sum annuity payout, you can use that money for the down payment to buy a home but not as monthly income to qualify for the loan. Lenders require confirmation that your annuity income will continue for at least three years after you submit your loan application. If your annuity income is subject to change due to fluctuations in underlying assets, lenders may apply a discount to the income to account for a potential decrease in the future.

Another important consideration is the tax advantages offered by annuities. This is a benefit that many other investing vehicles like CDs or treasury bonds do not offer. Your earnings are not taxed until they are withdrawn from the account, allowing for tax-deferred growth until the withdrawal is made. Income annuity payments will only be taxable in proportion to the amount of untaxed growth within the contract, alleviating a substantial tax burden.

Adding a Co-Borrower: Adjusting Your Mortgage Agreement

You may want to see also

![]()

Using an annuity to pay off a mortgage

An annuity can be a great source of income to qualify for a mortgage to buy a home or for a reverse mortgage. It can be used effectively to cover a monthly mortgage by providing a predictable and consistent income stream. This strategy works well for retirees with 10 or fewer years left on their mortgage.

The most logical types of annuities for paying a mortgage are fixed annuities or income annuities. Both offer a consistent and guaranteed flow of money over the length of the contract. Fixed annuities typically have a maturity of between three and 10 years, making them a good strategy for those with shorter mortgage terms. With predictable income and expenses, payments can be automated, reducing a significant financial burden.

Income annuities offer flexible payment options. For a mortgage with a set end date, a period-certain annuity, designed to end at a specific time, could be a good option. This often provides higher payouts than other options. Alternatively, retirees may opt for lifetime payments, ensuring income continues even after the mortgage is paid off.

Annuities also offer tax advantages. Earnings are not taxed until they are withdrawn from the account, allowing for tax-deferred growth. Income annuity payments are only taxable in proportion to the amount of untaxed growth within the contract, reducing the tax burden compared to using distributions from an individual retirement account (IRA).

However, a key risk of using an annuity to cover mortgage payments is limited liquidity. Most fixed annuities allow only a 10% penalty-free withdrawal, and accessing more funds can trigger significant surrender charges. Income annuities, often irrevocable, provide minimal flexibility unless optional riders are added. It is important to consult with a financial advisor before using an annuity to cover mortgage payments, as they are complex financial products.

Requesting a Mortgage Settlement Conference: What You Need to Know

You may want to see also

![]()

Tax advantages of annuities

Annuities can be a great source of income to qualify for a mortgage to buy a home or for a reverse mortgage. They can also be used to cover your mortgage payments month after month. The most logical types of annuities for paying a mortgage are a fixed annuity or an income annuity. Both offer a consistent and guaranteed flow of money over the length of the contract.

There are several tax advantages to annuities. Firstly, your earnings are not taxed until they are withdrawn from the account, allowing for tax-deferred growth. This is a benefit that many other investing vehicles, like CDs or treasury bonds, do not offer. Income annuity payments will only be taxable in proportion to the amount of untaxed growth within the contract. This alleviates a substantial tax burden compared to using distributions from an individual retirement account (IRA).

If you choose a deferred annuity, you can add money to the annuity over time, and that money will compound at whatever rate you've contractually agreed to during the "accumulation phase". These earnings are tax-deferred as long as they remain in the annuity, allowing you to earn compound interest and amass a larger nest egg for retirement. On the other hand, if you opt for an immediate annuity, you'll deposit your money in a lump sum and won't receive this tax-deferred benefit during the accumulation phase.

Early withdrawals from a non-qualified annuity will likely result in taxes being assessed on the earnings withdrawn, with an additional 10% penalty on the withdrawn earnings. However, there are exceptions to these rules, such as if the policyholder becomes disabled.

Understanding Mortgages: A Guide to Home Loans

You may want to see also

![]()

Annuity mortgages vs. linear mortgages

An annuity is a great source of income to qualify for a mortgage to buy a home or for a reverse mortgage. Annuity income can be used to cover your mortgage payments month after month. The income from an annuity and the liability payments on a mortgage are consistent and predictable. This strategy is effective for retirees with 10 years or less left on a mortgage.

An annuity mortgage is one of the most common types of home loans in the Netherlands. In an annuity mortgage, the gross monthly costs remain fixed during the lifetime of the mortgage. The monthly repayments include both mortgage and interest, which may result in higher initial payments. The total cost of an annuity mortgage is higher than the total cost of a linear mortgage, as you pay a higher amount in interest. However, the monthly costs are initially lower. For a mortgage of €200,000 with an interest rate of 2.5% and a mortgage term of 30 years, the monthly costs for an annuity scheme will initially be €176 lower than a linear scheme.

A linear mortgage is often considered to be the cheaper option. The monthly costs are higher in the first couple of years, but they decrease over time. In a linear mortgage, you pay off more of your capital in the early stages. A linear mortgage may be more suitable if you plan to work part-time or stop working altogether.

Maximizing Private Mortgage Interest: What You Need to Know

You may want to see also

![]()

Calculating loan instalments with annuity factors

An annuity can be a great source of income to qualify for a mortgage to buy a home or for a reverse mortgage. Annuity factors are used to calculate present values of annuities and equated instalments. The simplest type of annuity is a finite series of identical future cash flows, starting exactly one period in the future.

Annuity factors are used to calculate equated loan instalments. For a loan drawn down in full at the start, the equated loan instalment formula is:

> Instalment = Principal ÷ annuity factor

For example, if you borrow £10m in a lump sum, to be repaid in annual instalments, the lender will require full repayment of the principal, plus interest. If the interest rate is 5% per year, the first year's interest, before any repayments, will be £10m x 5% = £0.5m. The annual instalment is calculated using the annuity factor (AF), which is the ratio of the equated annual instalment to the principal borrowed at the start. The AF is calculated as:

> AF = (1 – (1+r)-n ) ÷ r

Where:

- R = interest rate per period

- N = number of periods

For example, if r = 0.05 (5%) and n = 4 (years), then:

> AF = (1 – 1.05-4 ) ÷ 0.05 = 3.55

Therefore, the equated annual instalment is:

> Instalment = £10m ÷ 3.55 = £2.82m

There are four payments of £2.82m each, so the total repayments are:

> £2.82m x 4 = £11.3m

The total interest charges for the four years are:

> £11.3m less £10m = £1.3m

Add Your Mortgage Account: A Guide for Wells Fargo Customers

You may want to see also

Frequently asked questions

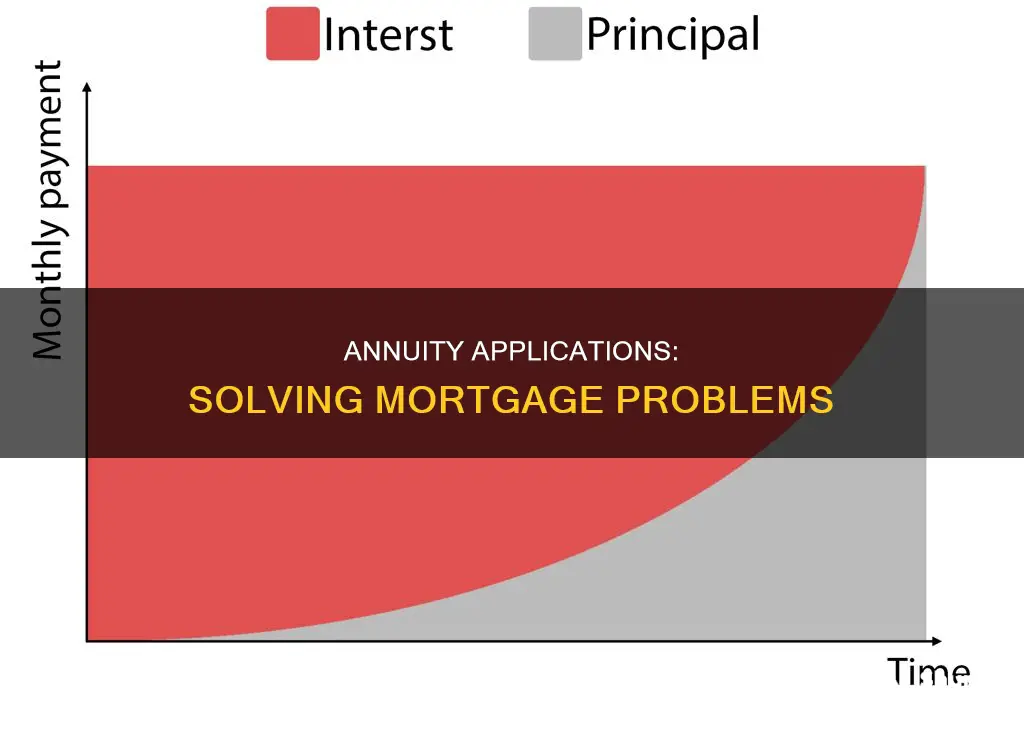

An annuity mortgage is a type of mortgage where you pay the same amount every month during the fixed interest rate period. This amount consists of two elements: the interest and the loan repayment.

During the initial period, you pay more interest and less of the loan. However, this interest is tax-deductible. Later, you pay more of the loan and less in interest.

First-time buyers can now choose between an annuity mortgage and a linear mortgage. Annuity mortgages are popular with first-time buyers because of the lower net costs at the beginning. Make sure to consider all factors carefully and consult a mortgage advisor before making a decision.