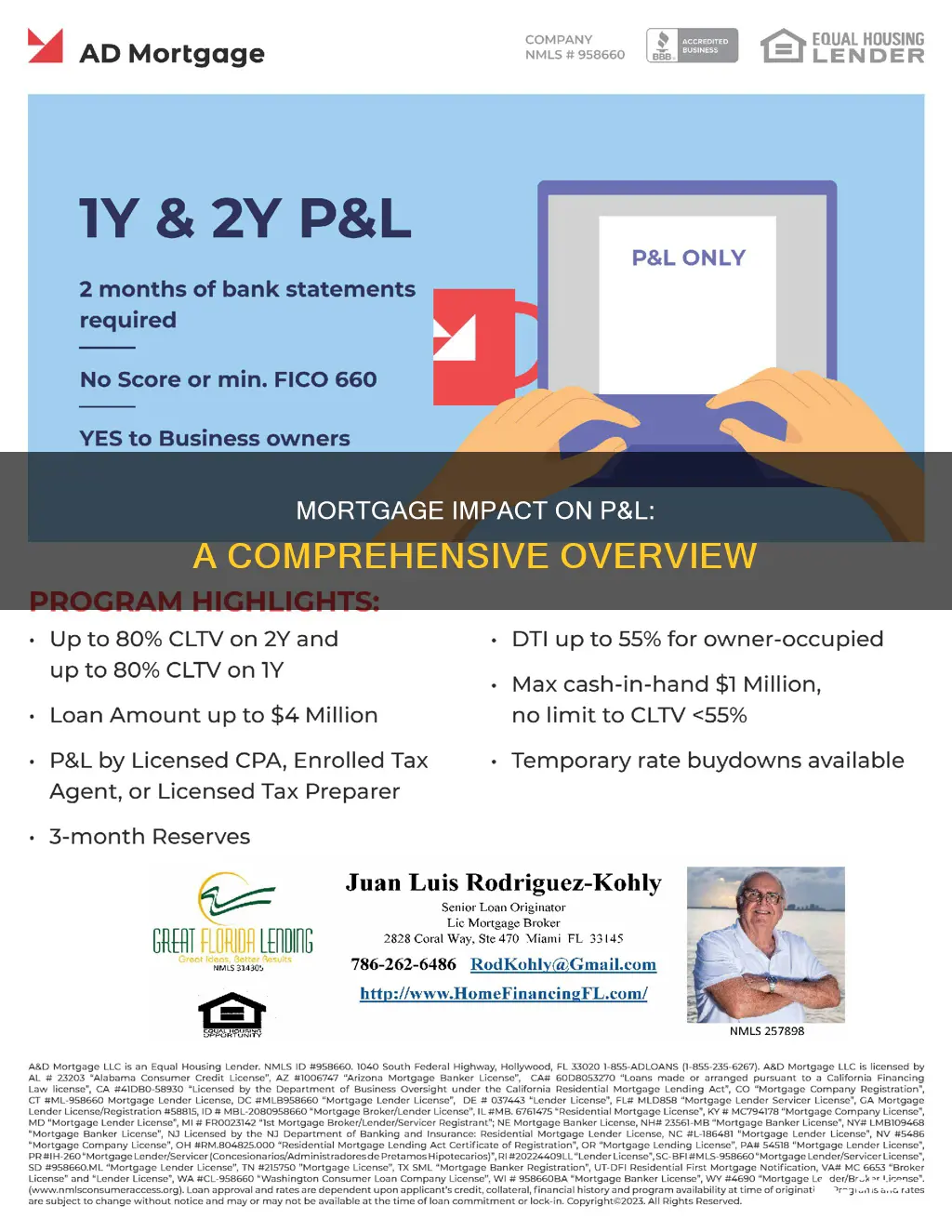

P&L, or Profit and Loss, mortgages are a type of loan designed specifically for self-employed individuals who want to become homeowners. These mortgages are unique in that they do not rely on traditional W-2 income statements or tax returns to assess a borrower's financial health and ability to repay a loan. Instead, they use profit and loss statements, bank statements, and other financial documents to evaluate a borrower's financial situation holistically. This approach is particularly useful for self-employed individuals who may have irregular incomes and unique tax deductions. While P&L mortgages can make homeownership more accessible to the self-employed, they also come with their own set of challenges, such as the need for accurate and well-organized financial records. It's also important to note that mortgage principal payments will not typically show up in a profit and loss report, but only in a balance sheet report.

What You'll Learn

![]()

P&L mortgages are designed for self-employed borrowers

P&L, or Profit and Loss, mortgages are specifically designed to help self-employed individuals secure home financing. These mortgages recognise the unique income streams and tax deductions that come with self-employment, and they evaluate a borrower's financial health holistically. This approach is particularly beneficial for those with irregular incomes or for whom tax returns do not reflect their actual earnings due to various deductions and business expenses.

P&L mortgages are also known as non-QM (non-qualified mortgages) because they do not follow the strict lending rules set by the Consumer Financial Protection Bureau (CFPB). Instead of focusing on a regular paycheck, P&L mortgages evaluate a borrower's average income over a specific period to determine their loan affordability. This makes it easier for self-employed individuals to qualify for a home loan.

To apply for a P&L mortgage, self-employed borrowers must provide detailed profit and loss statements, usually prepared by a certified accountant, along with bank statements and other financial records. These documents serve as proof of income and expenses, allowing lenders to assess the borrower's financial stability and ability to repay the loan. Maintaining well-organised and up-to-date financial records is crucial for streamlining the approval process.

P&L mortgages offer a promising solution for self-employed individuals seeking to achieve homeownership. By understanding the eligibility criteria and working with experienced mortgage brokers who specialise in P&L mortgages, self-employed borrowers can confidently navigate the mortgage application process and turn their homeownership dreams into reality.

Money Flows: Understanding Mortgage Money Trails

You may want to see also

![]()

P&L statements must be produced by a certified public accountant

P&L, or Profit and Loss, mortgages are specifically designed for self-employed borrowers. They are a financial tool that helps bridge the gap between salaried employees and self-employed individuals, who often experience fluctuating incomes. This variability can make it challenging to demonstrate financial stability to lenders.

P&L mortgages assess a borrower's income by examining their business's profit and loss statements, bank statements, and other financial documents. This offers a more accurate reflection of a self-employed borrower's financial health.

P&L mortgages can be used to purchase a primary residence, a second home, or an investment property. They can also be used to refinance an existing loan. Applicants need not produce tax returns or bank statements, and all or part of the down payment may be in the form of a gift.

Lower Fees, Bigger Benefits: Refinancing Your Mortgage

You may want to see also

![]()

P&L mortgages do not require bank statements

P&L mortgages, also known as profit and loss mortgages, are designed to help self-employed individuals and business owners secure home financing. Unlike traditional mortgages, P&L mortgages do not require bank statements, tax returns, or pay stubs, making them more accessible to those with non-traditional income sources.

P&L mortgages evaluate a borrower's financial health holistically, taking into account their unique income streams and tax deductions. The cornerstone of a successful P&L mortgage application is accurate profit and loss statements, which serve as proof of income and expenses. These statements are typically prepared by a certified public accountant and offer a method to show the net income of a business by considering its revenue and offsetting expenses.

By using profit and loss statements, self-employed borrowers can demonstrate their income stability and ability to repay the loan. This approach is particularly beneficial for those with inconsistent income or for whom tax returns do not fully reflect their actual earnings due to various deductions and expenses. P&L mortgages provide flexibility in the underwriting process, making it easier for self-employed individuals to qualify for home financing.

While P&L mortgages do not require bank statements, applicants should be prepared to provide detailed profit and loss statements, as well as other financial records that demonstrate the stability and profitability of their business. Maintaining a solid credit history and working with a lender experienced in handling self-employed borrowers are also crucial steps in securing a P&L mortgage.

Mortgages: Impacting Your Balance Sheet and Financial Stability

You may want to see also

![]()

P&L mortgages require a down payment

P&L (Profit and Loss) mortgages are a financial tool that helps self-employed individuals bridge the gap to homeownership. Traditional mortgage lenders rely on W-2 income statements, which makes it difficult for self-employed people to prove their ability to repay a loan. P&L mortgages, on the other hand, evaluate a borrower's financial health holistically, taking into account their unique income streams and tax deductions.

P&L mortgages typically require a down payment similar to traditional mortgages. The specific amount may vary depending on the lender and the loan program. All or part of the down payment may be in the form of a gift. While P&L mortgages do not require bank statements or tax returns, applicants must produce P&L statements prepared and signed by a certified public accountant. These statements must be accurate and up-to-date, as they serve as proof of income and expenses, allowing lenders to assess the borrower's financial stability.

To increase your chances of securing a P&L mortgage, it is recommended to maintain a consistent and reliable income, work on improving your credit score, and actively manage your debt. Lenders appreciate financial stability and a good credit history, so showcasing your financial responsibility can improve your chances of approval.

It is important to note that P&L mortgages may have slightly higher interest rates compared to traditional mortgages. Shopping around and comparing offers from different lenders is crucial to finding the most favourable terms for your unique financial situation.

Mortgage-Backed Securities: Boosting Economy Through Homeownership

You may want to see also

![]()

P&L statements are proof of income and expenses

P&L (profit and loss) statements are a critical component of the mortgage application process for self-employed individuals. They serve as proof of income and expenses, providing lenders with a comprehensive view of the applicant's financial health and stability.

P&L statements offer a detailed breakdown of a business's revenue and expenses, ultimately reflecting its net income. For self-employed borrowers, these statements are essential in demonstrating their ability to repay a loan. Unlike traditional W-2 income statements, P&L statements consider the unique income streams and tax deductions associated with self-employment. This recognition of variable income is particularly advantageous for self-employed individuals, who often face challenges in proving their financial stability due to fluctuating incomes.

The P&L statement is just one aspect of the mortgage application process for self-employed borrowers. Lenders may also require additional documentation, such as bank statements and other financial records, to make an informed decision. It is important for applicants to maintain well-organized and up-to-date financial records to streamline the approval process.

While P&L statements are a valuable tool for self-employed borrowers, it is worth noting that they may not always accurately reflect an individual's true financial situation. As such, lenders should evaluate a borrower's financial health holistically and consider additional factors beyond the P&L statement. This includes assessing the borrower's debt management, credit score, and overall financial responsibility.

In summary, P&L statements play a crucial role in the mortgage application process for self-employed individuals by serving as proof of income and expenses. They provide lenders with valuable insights into the applicant's financial stability and ability to repay a loan. However, it is important to complement the information provided by P&L statements with other financial documents to make a comprehensive assessment of the borrower's financial health.

Understanding Mortgages in 1031 Exchanges: What You Need to Know

You may want to see also

Frequently asked questions

A P&L mortgage, also known as a profit and loss mortgage, is a financial tool that helps self-employed individuals secure a mortgage. It assesses the borrower's income by examining their business's profit and loss statements, bank statements, and other financial documents.

To qualify for a P&L mortgage, you must provide detailed profit and loss statements, bank statements, and other financial records that demonstrate the stability and profitability of your business.

P&L mortgages make homeownership more accessible and attainable for self-employed individuals by recognizing their unique income streams and tax deductions. It offers a more accurate reflection of a self-employed borrower's financial health.

Securing a P&L mortgage can be challenging due to the fluctuating incomes of self-employed individuals, making it difficult to demonstrate financial stability to lenders. Additionally, maintaining well-organized and up-to-date financial records is essential but can be time-consuming.

A mortgage loan payable contains the principal amount owed on a mortgage loan. Any principal to be paid within 12 months of the balance sheet date is reported as a current liability, while the remaining amount is reported as a long-term liability.