The yield curve is a graphical representation of the yields of equally rated bonds with different maturity dates. It is a benchmark for debts in the market, including mortgage rates. The yield curve can be normal, inverted, or flat. A normal yield curve indicates a healthy, growing economy, with higher interest rates for long-term bonds compared to short-term ones. An inverted yield curve, on the other hand, indicates a potential economic slowdown or recession, with short-term interest rates exceeding long-term rates. The yield curve impacts mortgage rates as it reflects market expectations about future interest rates and economic growth. While it is not the only factor influencing mortgage rates, understanding the yield curve can help homeowners and investors anticipate changes in mortgage rates and make more informed financial decisions.

| Characteristics | Values |

|---|---|

| Yield curve type | Normal, inverted, flat |

| Yield curve function | Benchmark for other debts in the market, including mortgage rates |

| Yield curve data | Available on the Treasury's interest rate websites by 6:00 p.m. ET each trading day |

| Yield curve and mortgage rates | Inverted yield curves can indicate a reduction in mortgage costs for clients |

| Mortgage spread | Not a measure of market distortions but a reflection of refinancing behaviour |

| Mortgage rate forecasting | The yield curve can be used to predict mortgage rates |

| Mortgage rate determination | Mortgage rates are determined by investor demand for mortgage bonds |

| Mortgage rate factors | Economic indicators, inflation, and housing market conditions also influence mortgage rates |

What You'll Learn

![]()

How an inverted yield curve impacts mortgage rates

An inverted yield curve is a graphical representation that shows short-term interest rates exceeding long-term rates. This is unusual, as investors typically expect higher returns when they lend money for longer periods. Inverted yield curves can indicate a coming recession, as investors are not confident in the long-term economic outlook and pull their money out of long-term investments.

For mortgages, an inverted yield curve can be a red flag, as it often foreshadows a slowdown in economic growth. This can lead to reduced demand for housing, as potential homebuyers may be less confident about their financial stability and job security during a potential recession. Additionally, tighter credit conditions may be imposed by lenders, making it more difficult for borrowers to obtain mortgage loans.

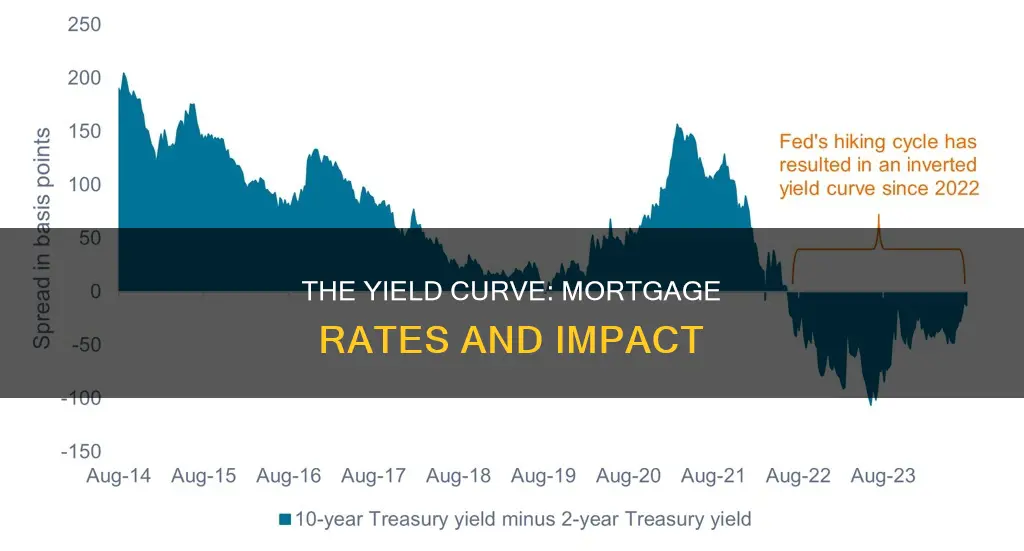

During an inverted yield curve, long-term mortgage rates may increase relative to short-term rates. This is because the yield curve inverts, shortening the expected duration of mortgages. In this scenario, short-duration assets have higher yields than longer-duration assets. As a result, 30-year mortgage spreads tend to increase relative to 10-year Treasury bonds.

However, it's important to note that an inverted yield curve does not directly cause a recession. Instead, it reflects changing expectations about the economy and can be a useful predictor of economic downturns. Investors closely monitor the yield curve and make investment decisions based on their expectations, which can further influence market conditions.

When the yield curve returns to its normal upward slope, with long-term bonds offering higher interest rates than short-term bonds, it can indicate that economic conditions are stabilizing. This disinversion can signal that inflation concerns are easing, and the Federal Reserve may be considering more accommodative policies. Realtors often view disinversion positively, as it can lead to a more favourable mortgage rate environment and increased buyer activity.

Mortgage Debt Proceeds: Co-Paying Strategies and Options

You may want to see also

![]()

How the yield curve predicts economic downturns

The yield curve is increasingly being relied on by economists as a forecaster of recessions. An inverted yield curve has often been a precursor to economic downturns, with investors expecting a decline in longer-term interest rates as a result of a deteriorating economic performance.

The yield curve's predictive powers are based on the spread between long- and short-term interest rates, which is a measure of the yield curve's slope. The smaller the interest rate spread between long- and short-term interest rates, the greater the probability of a recession. This is because the long-term yield reflects the path of short-term interest rates over the life of the bond, influenced by expectations about the business cycle and monetary policy. If market participants anticipate a downturn, they are likely to also expect that the FOMC will cut future policy rates to provide monetary policy accommodation. This expectation of lower future rates reduces longer-term rates, which can result in an inverted yield curve.

The 10-year to two-year Treasury spread has been a generally reliable recession indicator since the mid-1960s. For example, in 2006, the spread inverted for much of the year, and the Great Recession began in December 2007. However, it is important to note that an inverted yield curve does not cause a recession but rather reflects changing expectations about the economy.

While the yield curve can provide clues about the likelihood of a recession, it cannot guarantee the absence of one. For instance, in 1998, the Federal Reserve's quick interest rate cuts helped prevent a U.S. recession after the Russian debt default. Additionally, the yield curve inversion in 2019 did not predict the brief U.S. recession in 2020 caused by the COVID-19 pandemic.

Exploring Mortgage Relief: Understanding 1031 Exchange Benefits

You may want to see also

![]()

The yield curve as a benchmark for mortgage rates

The yield curve is a graphical representation of the yields of equally rated bonds with different maturity dates. It is a benchmark for other debts in the market, including mortgage rates. The yield curve can be normal, inverted, or flat. Each of these shapes has implications for the future economic climate, which in turn influences mortgage rates.

A normal yield curve is upward-sloping, indicating that long-term bonds have higher yields than short-term ones. This shape implies stable economic conditions and healthy economic growth. It is often accompanied by higher inflation and higher interest rates. An upward-sloping yield curve generally indicates a healthy, growing economy, where mortgage rates are stable or rising moderately. Homebuyers and investors often feel more confident in such environments, boosting the housing market.

An inverted yield curve slopes downward, indicating that short-term bonds have higher yields than long-term ones. This shape can signal an economic slowdown or even a recession. An inverted yield curve typically foreshadows a slowdown in economic growth, which can lead to reduced demand for housing, tighter credit conditions, and less favorable mortgage rates.

A flat yield curve indicates that short-term yields are equal to long-term yields. This shape can also signal an economic slowdown or recession.

While the yield curve is a helpful tool for understanding the future economic climate and its potential impact on mortgage rates, it is not the only factor influencing mortgage rates. Economic indicators, inflation, and housing market conditions also play a role. Therefore, it is advisable to consult a financial advisor or mortgage professional for personalized advice.

Rental Property Income: New Mortgage Game-Changer?

You may want to see also

![]()

How the yield curve influences mortgage decisions

The yield curve is a graphical representation of the yields of equally rated bonds with different maturity dates. It is a benchmark for debts in the market, including mortgage rates, and serves as a key economic indicator. The curve is plotted with bond yield on the vertical axis and the years to maturity of the bonds on the horizontal axis.

The yield curve can be normal, inverted, or flat. A normal yield curve indicates stable economic conditions and healthy economic growth, with long-term debt instruments having a higher yield than short-term ones. This can give homebuyers and investors more confidence, boosting the housing market. An upward-sloping curve also suggests that investors expect robust economic growth and higher future inflation, leading to higher interest rates.

On the other hand, a flat or inverted yield curve can signal an economic slowdown or even a recession. An inverted yield curve occurs when short-term bonds have higher interest rates than long-term ones, which is usually a warning sign of a coming recession. This can lead to reduced demand for housing, tighter credit conditions, and less favorable mortgage rates.

The slope of the yield curve is an important signal of investors' expectations for future interest rates and their expectations for future economic growth and inflation. For example, a household taking out a mortgage might decide to fix the interest rate on their loan for a certain number of years, and the bank will calculate the interest rate based on the relevant term on the yield curve.

While the yield curve can be a helpful tool for predicting mortgage rates and making informed financial decisions, it is not the only factor influencing mortgage rates. Economic indicators, inflation, and housing market conditions also play a significant role. Therefore, it is advisable to consult a financial advisor or mortgage professional for personalized advice.

Mortgage-Backed Securities: Boosting Economy Through Homeownership

You may want to see also

![]()

The impact of yield curve disinversion on long-term mortgage rates

A yield curve is a graphical representation of the yields of equally rated bonds with different maturity dates. It is a benchmark for other debts in the market, including mortgage rates and bank lending rates. The yield curve can be used to predict changes in economic output and growth over time and is influenced by economic indicators, inflation, and housing market conditions.

When the yield curve is in a normal, upward-sloping position, it indicates stable economic conditions and a normal economic cycle. This is because investors expect higher returns for locking in their money for extended periods due to potential risks like inflation or changes in economic conditions. An upward slope suggests confidence in economic growth, which tends to create a favourable environment for the housing market.

However, when the yield curve is inverted, it signals economic uncertainty and a potential slowdown in homebuying and investments. In this scenario, short-term interest rates exceed long-term rates, which is unusual as investors typically expect higher returns for long-term investments. An inverted yield curve can indicate that a recession may be approaching.

When the yield curve disinverts, it returns to its normal upward slope after a period of inversion. This can signal that economic conditions are stabilising and that inflation concerns are easing. For mortgages, disinversion can lead to lower interest rates, making long-term mortgages more affordable for homebuyers. Realtors can use this opportunity to advise clients on the optimal timing for buying or selling, as long-term mortgage rates may begin to fall.

Nationwide Title's Mortgage Note: Recreating the Details

You may want to see also

Frequently asked questions

A yield curve is a graphical representation that plots the interest rates of equally rated bonds with different maturity dates. It is a benchmark for debt in the market, including mortgage rates.

The yield curve can be used to predict changes in economic output and growth over time. It serves as a key economic indicator, reflecting market expectations about future interest rates and economic growth. For example, a steep yield curve indicates strong economic growth, often accompanied by higher inflation and interest rates. Conversely, a flat or inverted yield curve can signal an economic slowdown or recession.

An upward-sloping yield curve generally indicates a healthy, growing economy with stable or moderately rising mortgage rates. Homebuyers and investors often feel more confident in such environments, boosting the housing market. On the other hand, an inverted yield curve can foreshadow a slowdown in economic growth, leading to reduced demand for housing and less favourable mortgage rate environments. It is also a sign that economic conditions are stabilising, which could result in lower mortgage rates and increased buyer activity.