Getting approved for a mortgage can be a stressful process, but it doesn't have to be. Lenders will consider a variety of factors when assessing your application, including your credit score, income, assets, employment, valuation, and title. While there is no minimum income requirement, a good rule of thumb is that your monthly mortgage payment should not exceed 28% of your gross monthly income, and your total debt payments should not be more than 36%. Additionally, a higher credit score will increase your chances of approval and result in a lower interest rate. To improve your chances of approval, you can take steps such as improving your credit score, minimising debt, maintaining a stable income, and saving for a down payment.

| Characteristics | Values |

|---|---|

| Credit Score | Typically, a score of 620 is required for a conventional loan, but the higher the better. |

| Down Payment | A larger down payment improves your chances of approval. |

| Debt-to-Income Ratio | Lenders prefer a DTI of 36% or less, but the lower the better. |

| Income | A higher income improves your chances of approval. W2 income is the best sign of income consistency. |

| Employment History | A stable employment history is preferred. |

| Assets | Lenders will consider the consumer's assets to assess their ability to repay. |

| Pre-Approval | Pre-approval is not a guarantee but improves your chances of approval. |

| Application Process | The application process can be stressful and time-consuming. |

What You'll Learn

![]()

Credit score

To improve your credit score, you can take several steps. Firstly, pay down some debt to achieve a credit utilisation rate of under 30%. Secondly, ensure you make timely payments and, if possible, pay more than the minimum amount. Thirdly, stay under your credit limit, as exceeding it can negatively impact your score. Fourthly, maintain a longer credit history by keeping older credit cards open. Fifthly, diversify your credit mix by using different types of credit, such as a credit card and a line of credit. Finally, limit hard inquiries on your credit report, as frequent credit applications can lower your score.

Before applying for a mortgage, it is advisable to obtain a copy of your credit report and address any discrepancies or errors. This proactive step can help you identify areas for improvement and increase your chances of mortgage approval. By understanding the weightage of credit scores in the mortgage approval process, you can take informed steps to enhance your creditworthiness and secure a favourable loan outcome.

Understanding Rental Property Mortgage Debt on Your FAFSA

You may want to see also

![]()

Income

To assess your income, lenders will typically review your income tax returns for the past several years and your most recent pay stubs. They will also want to see that your income is established and consistent. For this reason, they usually require you to have at least two years of a given income type before they will consider it as part of your mortgage application. W2 income, or full-time employment, is generally seen as the best sign of income consistency.

In addition to your income, lenders will also consider your assets when assessing your ability to repay the mortgage. Liquid assets, such as cash or investments that can be easily converted into cash, are considered particularly valuable in this context. This is because they can be used to cover your monthly mortgage expenses if your income takes a hit or you face a period of unemployment.

It is worth noting that there is no hard and fast rule regarding the minimum income required to obtain a mortgage. The specific amount will depend on factors such as the property price, your credit score, and the lender's requirements. However, as a rule of thumb, lenders typically approve a mortgage loan with a monthly payment equal to 28% or less of your gross monthly income. In terms of the total loan amount, a good rule of thumb is 4.5 times your gross annual income. For example, a household with an annual income of $100,000 should be able to get a mortgage on a house worth up to $450,000.

Navy Federal: Your Mortgage Journey Companion

You may want to see also

![]()

Assets

When it comes to getting approved for a mortgage, one of the factors that lenders will consider is your assets. This is because they need to assess your likelihood and ability to repay the mortgage and the risk that you will default on the loan. The more assets you have, the more likely you are to be approved.

Lenders will look at your overall financial portfolio, including your income, debt, credit history, savings, home value, and loan program guidelines. They will also consider the valuation of the underlying asset, which is vital as the house or apartment can be seized in the case of a foreclosure to cover the debt.

Liquid assets, such as cash or investments that can be easily converted into cash, are considered more valuable in the overall assessment. This is because they can be quickly and easily used to cover mortgage payments in the event of a loss of income.

Before the 2007/2008 housing crisis, it was possible to get a NINJA (No Income, No Job, No Assets) mortgage loan, with the house acting as security for the loan. However, this is no longer the case, and lenders now place a much greater emphasis on assets and other financial criteria when considering mortgage applications.

To increase your chances of mortgage approval, it is important to have a strong financial portfolio, including a diverse range of assets that can demonstrate your ability to repay the loan. Lenders will also consider your debt-to-income ratio, credit score, and employment history, so it is crucial to address any issues in these areas before applying.

Nationwide Title's Mortgage Note: Recreating the Details

You may want to see also

![]()

Employment history

Lenders will want to see that you have a stable income and a good employment history. They will require information about your current employer and any former employers to determine if you will qualify for a loan. The purpose is to confirm that you are currently employed, that your income is stable and predictable, and that there is a likelihood of continuity.

Lenders will typically verify your employment when you initially apply for a mortgage and again shortly before your scheduled mortgage closing date. They will also require documentation of your income, such as W-2 forms and pay stubs, to verify that you have a steady income.

A two-year employment history is standard, but shorter employment histories may be permitted for applicants with stable jobs and incomes or other positive factors. For example, lenders will generally accept a two-year history of consistent work in the same line of work, even if it is not the same job. Lenders may also approve your mortgage without a two-year employment history if you have strong compensating factors, such as a large down payment, excellent credit score, low debt-to-income ratio, significant savings, or assets.

If you are self-employed, it is important to show that you have a steady income. Lenders will want to see documentation of your earnings, such as tax and financial statements. They will also want to confirm that your income is enough to make the payments on the loan.

Securitization Obscures Default Mortgages: Hiding in Plain Sight

You may want to see also

![]()

Down payment

The down payment is the percentage of the home's purchase price that you pay upfront when closing your home loan. It is separate from your closing costs. The down payment funds are held in escrow until the sale is complete, after which they are disbursed to the seller.

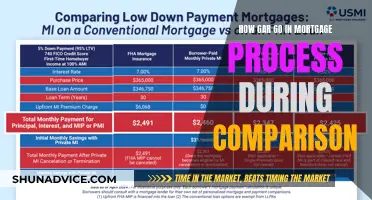

The down payment amount is usually between 3% and 20% for a primary residence. The minimum down payment for mortgage approval is typically 3-5%, although you may qualify for an FHA loan with a down payment as low as 3.5%, or a VA loan with no money down. If your down payment is less than 20%, you will likely have to pay private mortgage insurance (PMI), which increases your monthly payments.

The down payment amount is important because it lowers your loan-to-value ratio (LTV) and indicates how much you will owe on the home after your down payment. The higher your down payment, the lower your loan amount and LTV will be. A larger down payment may also help you purchase a higher-priced home or get a lower interest rate.

To increase your chances of mortgage approval, you should aim to improve your credit score, minimise debt, and save for a down payment. You can also get pre-approved before house hunting to strengthen your offer.

Becoming a Mortgage Advisor: Is It Simple?

You may want to see also

Frequently asked questions

It depends on several factors, including your credit score, income, debt, and the type of loan you're applying for. Lenders will also consider your assets, employment history, and the value of the property. Getting pre-approved for a mortgage can increase your chances of approval and make your application process smoother.

A credit score of 620 or above is typically required for a conventional loan, but the higher your score, the better your chances of approval. A score of 660 or above is generally considered "good".

The down payment requirement varies by lender and loan type. Typically, a down payment of 20% or more is preferred, as it lowers your loan-to-value (LTV) ratio and reduces the lender's risk. However, some lenders may accept a lower down payment, such as 3-5%, or offer specialised loan programs with no down payment.

The approval process typically takes around 30 to 45 days but can be shorter or longer depending on the complexity of the application, document verification, and the lender's workload. Getting pre-approved before starting the process can help expedite the approval timeline.