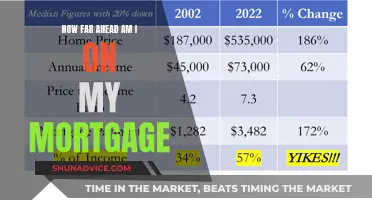

The mortgage market has changed significantly over the years, evolving from the lending practices of the 14th century to the modern-day home loans we know today. The modern mortgage market dates back to the 1930s and 1940s when Congress passed laws to promote homeownership and protect homebuyers and lenders, leading to the creation of the Federal Housing Administration (FHA) and Fannie Mae. Today, the mortgage market is influenced by various factors such as supply and demand, interest rates, economic policies, and government interventions. While the COVID-19 pandemic brought record-low mortgage rates, the market has since faced challenges due to increasing rates, high home prices, and economic uncertainties. These factors have impacted housing affordability and buyer behaviour, with many homeowners opting to stay put due to the lock-in effect of low mortgage rates. As of 2025, Americans owe $12.61 trillion on 85.10 million mortgages, highlighting the integral role of the mortgage market in the economy.

| Characteristics | Values |

|---|---|

| Supply and demand | There is less supply than demand, and people have more at stake |

| Employment | There are more jobs, so people can get multiple jobs to pay their mortgage |

| Interest rates | Mortgage rates are high, but they have been declining since the start of 2025 |

| Housing market activity | Activity is sluggish due to high interest rates and high home prices |

| Housing bubble | The housing bubble collapsed in 2008, in part because of increased investments in subprime mortgages |

| Mortgage debt | Americans owe $12.61 trillion on 85.10 million mortgages |

| Delinquencies | Only 0.70% of borrowers are seriously delinquent |

| Foreclosures | The number of foreclosures hasn't dramatically increased |

| Home prices | The median home price has increased |

| Inventory | There is more inventory on the market |

| Real estate agents | Buyers must sign an agreement that sets the agent's compensation before they can view homes |

What You'll Learn

![]()

The impact of the 2008 housing bubble collapse

The 2008 housing bubble collapse, also known as the Subprime Mortgage Crisis, had a significant impact on the mortgage market and the global economy. Here are some key impacts of the 2008 housing bubble collapse:

- Economic Recession: The collapse led to a severe economic recession, resulting in job losses and business bankruptcies. Millions of people lost their jobs, and many businesses went bankrupt, requiring government intervention to stabilize the financial system.

- Increase in Mortgage Defaults: The collapse of the housing bubble resulted in an unprecedented number of borrowers missing mortgage repayments and becoming delinquent. This was due to high-interest rates and the collapse of housing prices, leading to a loss of equity for homeowners.

- Mass Foreclosures: The high rate of mortgage defaults triggered mass foreclosures, further devaluing housing-related securities and contributing to the financial crisis.

- Impact on Financial Institutions: Financial institutions, particularly those with significant exposure to the housing market, suffered substantial losses. This included government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac, as well as private lenders and Wall Street banks. Some institutions, like Lehman Brothers, faced bankruptcy due to mounting losses and liquidity crises.

- Government Intervention: The U.S. government intervened with measures such as the Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA) to stabilize the financial system and provide support to homeowners struggling with mortgage debts.

- Changes in Lending Practices: The crisis led to a reevaluation of lending practices and regulations. There was a shift away from risky lending practices, and new safeguards and regulations were implemented to prevent a similar crisis from occurring in the future.

- Housing Market Recovery: While the recovery timeline varied across different geographic areas, it generally began in 2011, and home prices had fully recovered by 2012. However, the crisis highlighted the dangers of excessive risk-taking and the importance of proper oversight in financial innovation.

- Impact on Consumer Spending: The collapse of the housing bubble affected consumer spending, as many people had reduced their monthly mortgage payments through refinancing at lower interest rates or withdrawn equity from their homes during the housing boom.

Affording an Expensive Mortgage: $1000 Monthly Commitment?

You may want to see also

![]()

The role of the Federal Housing Administration

The mortgage market has changed significantly over the years, with the modern market dating back to the 1930s and 1940s when Congress passed laws to promote homeownership. One of the key developments during this period was the creation of the Federal Housing Administration (FHA).

The FHA was established in 1934 during the Great Depression to protect homebuyers and mortgage lenders and stimulate the housing market. The agency became part of the US Department of Housing and Urban Development (HUD) in 1965. The FHA offers mortgage insurance to approved lenders, providing protection against losses, especially in the case of borrower defaults. This insurance is funded by mortgage insurance premiums (MIPs) collected from FHA-insured loans.

The FHA's role is particularly important for borrowers who cannot make large down payments, have lower credit scores, or do not qualify for conventional mortgages. By providing insurance to lenders, the FHA makes it possible for more people to qualify for mortgages and buy homes. This was especially critical during the Great Depression when bank failures and widespread unemployment led to a significant decline in homeownership, with between 40 and 50% of all home mortgages in default by 1933.

However, the FHA has also faced criticism for its implementation of policies such as redlining, which prevented Black citizens from accessing the same programs as their White peers, exacerbating racial wealth inequities. Additionally, the FHA's shift from an emergency source of housing finance to the bedrock of the housing finance system has raised concerns about its accuracy in pricing risk, its lack of systemic oversight or regulation, and its ability to provide countercyclical relief during financial crises.

In recent years, the FHA has continued to play a significant role in the housing market, particularly in the reverse-mortgage market. The Home Equity Conversion Mortgage (HECM) program, established in 1992, allows households with members aged 62 or older to borrow money using the equity in their homes as collateral. The FHA guarantees repayment on these qualifying reverse mortgages, encouraging lenders to issue them more readily. While the HECM program has faced scrutiny and been modified to reduce risks and costs, it continues to be a focus of federal housing policy.

Comparing Your Mortgage: How Does it Stack Up?

You may want to see also

![]()

Changes in interest rates

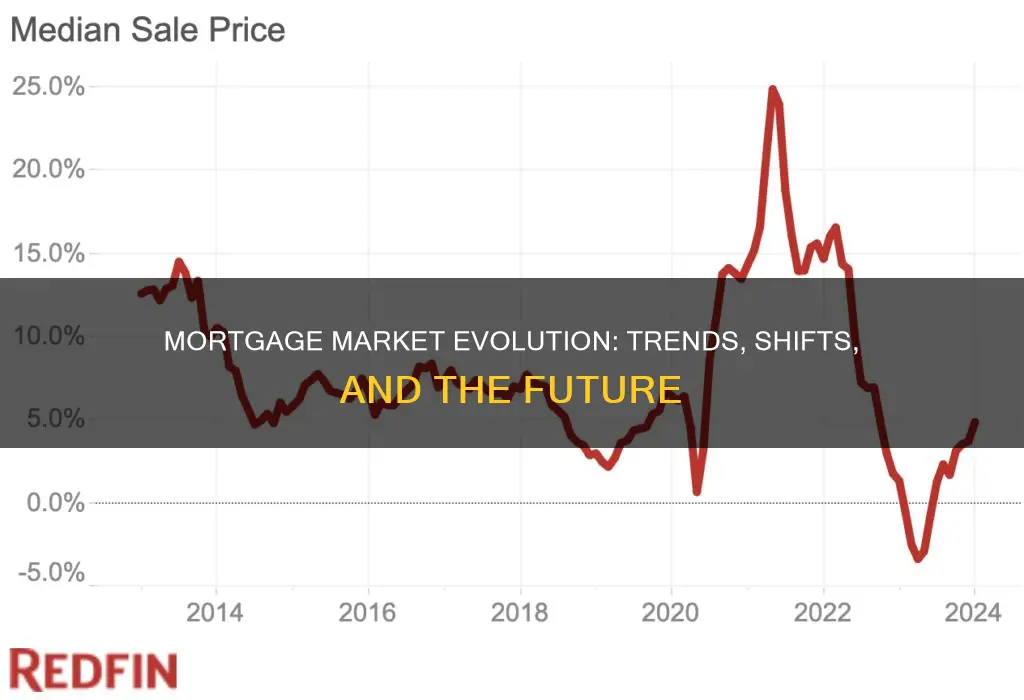

During the Great Depression in the 1930s, the housing market experienced one of the first examples of a housing bubble burst. This led to a period of low-interest rates and government interventions to encourage lending and homeownership. Fast forward to the 2008 housing bubble collapse, and we see another critical juncture for interest rates. The subprime mortgage crisis resulted in a need for a government bailout, and the subsequent years saw fluctuations in interest rates as the market recovered.

More recently, the COVID-19 pandemic brought record-low mortgage rates, providing an opportunity for many buyers to lock in favourable rates. This surge in mortgage debt, driven by low-interest rates, continued into 2021, with super-prime borrowers taking advantage of the low rates. However, as economic headwinds picked up, including inflation and labour market challenges, interest rates began to climb again.

As of 2025, the housing market is facing challenges due to elevated mortgage rates, which have dampened housing market activity. The combination of rising home prices and high-interest rates has made housing affordability a significant concern. While there are signs of improvement, with more homes hitting the market and a rebound in existing home sales, the impact of high-interest rates continues to be felt.

Looking ahead, there is uncertainty about how policies and economic factors will influence interest rates. While some analysts predict that interest rates will remain relatively stable, others suggest that market volatility could lead to fluctuations in mortgage rates. As a result, homebuyers and lenders remain cautious, hoping for a more favourable interest rate environment to boost housing market activity.

Mortgage CRM and LOS Integration: A Powerful Combination

You may want to see also

![]()

Increased demand and decreased supply

The demand for housing has increased, while the supply has decreased. This can be attributed to several factors, including the impact of the COVID-19 pandemic, which caused a frenzy in the housing market due to record-low mortgage rates. This led to a massive increase in outstanding mortgage debt, with more people taking out active mortgages and larger mortgages being taken out.

The demand for housing has also been influenced by the return to office mandates, with some people moving closer to cities now that they are required to be in the office several days a week. Additionally, there is a growing presence of first-time homebuyers in the market, which may be due to repeat buyers being less active because of the mortgage lock-in effect.

On the supply side, there is a general sluggishness in the housing market due to steep mortgage rates and high home prices. This is impacted by various economic factors, such as inflation and a weakening labour market. There is also uncertainty in the market due to new policies, such as potential immigration crackdowns and tariff policies, which could affect building supply costs and the availability of labour.

The combination of rising demand and limited supply has resulted in a challenging housing market, with high home prices and elevated mortgage rates. This has made housing affordability a significant problem, and it remains to be seen whether the market will stabilise in the coming months.

Nationwide Title's Mortgage Note: Recreating the Details

You may want to see also

![]()

The rise of first-time homebuyers

The mortgage market has undergone significant changes over the years, and one of the most notable trends has been the rise of first-time homebuyers. This demographic has become a crucial driving force in the market, with their demand serving as a buffer against rising mortgage rates.

One of the primary reasons behind the increase in first-time homebuyers is demographics. The large cohort of millennials who entered the job market in the mid-2000s is now in their early to mid-30s, which is typically the age range when individuals consider buying their first home. Additionally, the number of higher-income young renters has nearly doubled in the past decade, indicating a substantial untapped market of potential first-time homebuyers.

In 2020, 2.4 million first-time homebuyers obtained mortgages, a 26% increase from 2016 when 1.9 million first-time homebuyers entered the market. This surge in demand from first-time homebuyers has been a significant contributor to the overall rise in home sales. However, it's important to note that existing homes are generally more affordable, selling for about 25% less than new homes. As a result, many first-time homebuyers are competing for a limited inventory of existing homes, further driving up demand.

First-time homebuyers face several challenges, including rising mortgage rates, which impact housing affordability. Additionally, there is a shortage of affordable entry-level homes, with existing home inventory increasingly occupied by higher-income households. This mismatch between supply and demand has resulted in an insufficient number of affordable options for first-time buyers. Nevertheless, the demand from this cohort remains strong, and they continue to play a crucial role in driving the market forward.

Avoiding Foreclosure: Understanding Mortgage Arrears and Your Options

You may want to see also

Frequently asked questions

The demand for mortgages has increased, with more people taking out active mortgages and larger mortgages being taken out. This has been influenced by record-low mortgage rates during the COVID-19 pandemic, allowing buyers to increase their purchase prices.

The mortgage market has become more regulated over time. In the 1930s and 40s, Congress passed laws to promote homeownership and protect homebuyers and mortgage lenders, leading to the Federal Housing Administration (FHA). More recently, the GSEs have been placed under conservatorship, and the chief regulator for Fannie Mae and Freddie Mac is now also the board chair of both companies.

The behaviour of buyers has changed due to the lock-in effect, where homeowners with low-interest rates are reluctant to move. This has resulted in a frozen market and less inventory. However, there are signs of a shift, with more homes on the market and buyers taking advantage of increased inventory and leverage.