If you're 55 and wondering how to invest for retirement, don't panic. While it's important to start retirement planning early, you can still achieve your goals. Here are some tips to help you boost your retirement savings:

- Fund your 401(k) to the max: If your workplace offers a 401(k) plan, now is the time to increase your contributions. Not only is it an easy and automatic way to invest, but you can also defer paying taxes on that income until you withdraw it in retirement.

- Rethink your 401(k) allocations: Consider adjusting your investment portfolio to be more conservative as you get older. While it's important to remain diversified, you may want to shift your allocation towards more stable, low-risk investments like bonds.

- Consider adding an IRA: If you don't have access to a 401(k) or you've maxed out your contributions, consider opening an Individual Retirement Account (IRA). This will allow you to continue building your retirement savings with tax advantages.

- Know all your sources of income: Evaluate your expected income streams during retirement, including traditional pensions, Social Security benefits, and any other investments or savings. This will help you understand how much more you need to save.

- Take advantage of catch-up contributions: Individuals aged 50 and above are often eligible for catch-up contributions to their retirement accounts. For example, in 2024, Americans aged 50 and up can contribute up to $30,500 to their 401(k) and up to $8,000 to an IRA.

- Create a health savings account: Prepare for unexpected medical costs by opening a health savings account. This will reduce your taxable income, and you can make tax-free withdrawals after the age of 65.

- Make the most of Social Security: Consider delaying retirement to increase your monthly Social Security benefit checks. By waiting until you're 70 instead of claiming benefits at 62, your monthly benefit amount can significantly increase.

| Characteristics | Values |

|---|---|

| Recommended retirement savings at age 50 | Six times your yearly salary |

| 401(k) contribution limit in 2024 | $23,000 |

| 401(k) contribution limit in 2024 for those aged 50 or older | $30,500 |

| IRA contribution limit in 2024 | $7,000 |

| IRA contribution limit in 2024 for those aged 50 or older | $8,000 |

| Recommended investment allocation at age 50 | 70% to 75% bonds, 15% to 20% stocks, and 5% to 15% in cash or cash equivalents |

| Recommended investment allocation for a moderately conservative portfolio | 55% to 60% bonds and 35% to 40% stocks |

| Recommended investment allocation for those in their 20s | 80% stocks and 20% bonds |

| Recommended savings rate | 10% to 15% of income |

| Recommended savings rate for those in their 40s | 15% of income |

What You'll Learn

![]()

Fund your 401(k) to the max

If you're 55 or older, you can make an additional "catch-up contribution" of $7,500 on top of the standard maximum contribution of $23,000 for a total of $30,500. This is a great option if you want to boost your retirement savings and you're in a financial position to do so.

If your workplace offers a 401(k) plan, now is a good time to increase your contributions, especially if you aren't already funding yours to the maximum amount. 401(k) plans are an easy and automatic way to invest, and you'll be able to defer paying taxes on that income until you withdraw it in retirement.

Since your 50s and early 60s are likely to be your peak earning years, you may be in a higher marginal tax bracket now than you will be during retirement. This means you'll face a smaller tax bill when the time comes to withdraw your savings.

The maximum amount you can contribute to your plan is adjusted each year to reflect inflation. In 2024, the standard maximum amount is $23,000 for anyone under the age of 50.

If you're able to max out your 401(k) contributions, that's fantastic! But if you're not quite there yet, don't worry. Contributing anything above the standard maximum is still beneficial and will help you build a comfortable retirement fund.

- Start contributing as early as you can. The longer your money is invested, the more time it has to benefit from compound interest.

- Take full advantage of any 401(k) match offered by your employer. This is essentially "free money" that you don't want to leave on the table.

- Work towards saving at least 15% of your income for retirement, including any employer contributions. This may seem like a lot, but remember that it includes any percentage that your employer matches, and you can start small and gradually increase your contributions over time.

- Keep track of your 401(k)s, especially if you've changed jobs multiple times. It's not uncommon for people to forget about 401(k) plans from previous employers. Make sure to audit your résumé and keep track of all your retirement accounts to maximise your savings.

Invest Now: Where to Put Your Money

You may want to see also

![]()

Consider adding an IRA

If you're approaching retirement age, it's important to ensure you have a sound financial plan in place. One option to consider is adding an individual retirement account (IRA). IRAs come in two varieties: traditional and Roth. With a traditional IRA, contributions are made with pre-tax dollars, meaning they're tax-deductible in that year. With a Roth IRA, you get your tax break at the other end, as withdrawals are tax-free.

The maximum you can contribute to an IRA in 2024 is $7,000, plus another $1,000 if you're aged 50 or older. It's important to note that you can only contribute earned income to an IRA, such as wages, salaries, tips, and commissions. Certain forms of compensation, such as pension payments, annuity payments, and Social Security benefits, do not count as earned income for IRA contributions. Additionally, you cannot contribute more than your annual earnings, and you must adhere to the annual contribution limits set by the IRS. For 2024, the limit is $7,000 for individuals under 50, and $8,000 for those aged 50 and over.

There are several benefits to contributing to an IRA during retirement. Firstly, you'll be padding your nest egg, allowing you to save up a nice sum of money. Secondly, if you fund a traditional IRA, you can lower your tax liability and put yourself in a lower tax bracket. And if you fund a Roth IRA, you can allow your savings to grow tax-free.

However, there are also some potential drawbacks to consider. Contributing to an IRA during retirement may not be financially feasible for everyone, especially if you're on a fixed income. Additionally, putting money into an IRA may mean locking it in for a certain amount of time, reducing your financial flexibility.

It's important to carefully consider your financial situation and goals when deciding whether to add an IRA to your retirement plan. Consulting with a financial advisor can help you make an informed decision that aligns with your needs and objectives.

Investing: Why the Fear?

You may want to see also

![]()

Take advantage of catch-up contributions

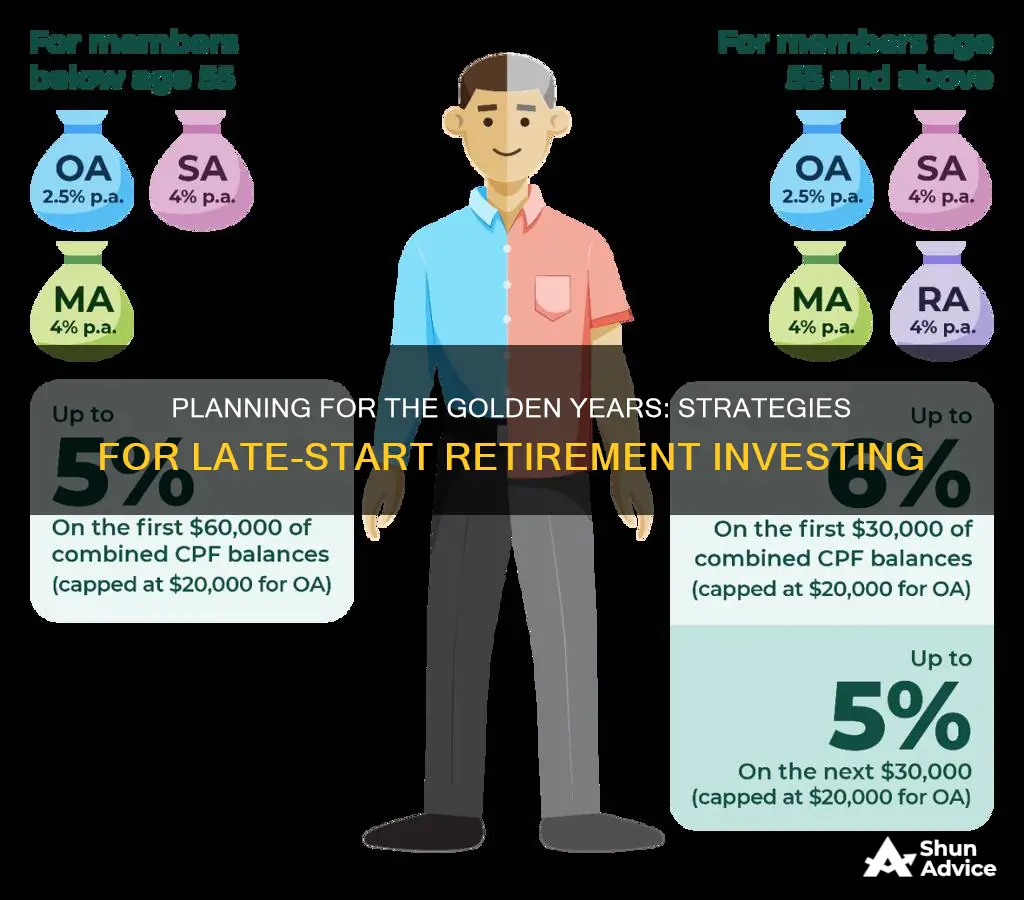

If you're 55, you're eligible to make catch-up contributions to your retirement savings. Catch-up contributions are extra amounts that individuals aged 50 or over can contribute to their tax-sheltered retirement accounts. Catch-up contributions can be made to 401(k) plans, IRAs, and HSAs.

In 2024, the maximum amount that individuals under 50 can contribute to their 401(k) is $23,000. However, those aged 50 and over can contribute up to $30,500 to their 401(k) as a catch-up contribution. This means that individuals over 50 can contribute an additional $7,500 on top of the regular contribution limit.

For IRAs, the maximum contribution limit in 2024 is $7,000 for those under 50. Those aged 50 or over can contribute up to $8,000, including a catch-up contribution of up to $1,000.

Catch-up contributions can provide significant benefits for those who are behind on their retirement savings or want to boost their retirement income. By taking advantage of catch-up contributions, you can increase your tax-advantaged savings and potentially reduce your current tax bill. Additionally, investing in a tax-advantaged account can provide long-term benefits, such as tax-deferred compounding or tax-free withdrawals.

It's important to note that catch-up contributions must be made before the end of the plan year, and there may be specific requirements or limits based on the type of retirement plan you have. Therefore, it's recommended to review the rules and regulations of your retirement plan to maximize your savings effectively.

Silver: Inflation Hedge

You may want to see also

![]()

Make the most of Social Security

If you're 55, it's a good idea to start thinking about your plan for collecting Social Security benefits. Here are some tips to make the most of your Social Security:

- Delay taking your benefits until you reach full retirement age or even until you're 70. The longer you wait, the higher your monthly benefit will be. For every year you delay past your full retirement age, your benefit will increase by 8% until you reach 70. However, there is no incentive to wait past 70, as your benefits won't increase any further.

- Work for at least 35 years. Your Social Security benefit is calculated based on your 35 highest-earning years. If you work for fewer years, those zeros will be factored into the calculation, reducing your payout.

- If you're married, consider claiming spousal benefits. You may be eligible for up to 50% of your spouse's benefit, depending on their retirement age and your own age when you start claiming. Even divorcees can claim spousal benefits based on their ex-spouse's earnings, as long as the marriage lasted at least 10 years.

- If you have dependent children under the age of 19, you may be able to secure additional Social Security payments for them, worth up to 50% of your full retirement benefit.

- Keep track of your earnings if you continue to work after receiving Social Security payments. There are limits on how much you can earn without reducing your benefits. For 2024, the limit is $22,320 for those below full retirement age and $59,520 for those who reach full retirement age during the year.

- Watch out for tax-bracket creep. Your earnings plus Social Security benefits could push you into a higher tax bracket.

- Apply for survivor benefits if your deceased spouse was eligible for higher Social Security payments than you. You may be able to claim their higher benefit amount.

- Check your Social Security statement for mistakes. A miscalculation, even for a single year, could impact your benefit for life.

Reliance Industries: Invest Now?

You may want to see also

![]()

Diversify your portfolio

Diversifying your portfolio is a crucial aspect of retirement planning, helping to balance risk and return. Here are some detailed strategies to diversify your portfolio for retirement at age 55:

Maintain a Mix of Stocks, Bonds, and Cash Investments:

Diversification is about spreading your investments across different asset classes. At age 55, you may want to adjust your portfolio to include a mix of stocks, bonds, and cash investments. Stocks provide growth potential, bonds offer more stability, and cash investments provide liquidity. The exact allocation will depend on your risk tolerance and financial goals.

Shift Towards Conservative Investments Gradually:

As you approach retirement, it's common to reduce the proportion of stocks in your portfolio and increase conservative investments like bonds and cash equivalents. However, completely abandoning stocks is not advisable, as they can help your portfolio keep up with inflation and provide growth potential. A conservative portfolio might consist of 70-75% bonds, 15-20% stocks, and 5-15% cash or cash equivalents.

Take Advantage of Catch-up Contributions:

At age 50 and above, you are allowed to make additional "catch-up" contributions to your retirement accounts. For 2024, Americans aged 50 and up can contribute up to $30,500 to their 401(k) and up to $8,000 to an Individual Retirement Account (IRA). These extra contributions can help boost your retirement savings and provide more flexibility in your portfolio diversification.

Consider Different Types of Stocks and Bonds:

Within the stock and bond categories, there are various options to choose from. For stocks, you can diversify across large-cap, mid-cap, and small-cap stocks, as well as growth stocks. For bonds, consider corporate bonds, preferred stock offerings, and moderate-risk instruments that offer competitive returns with lower risk than pure equities.

Explore Alternative Investments:

Alternative investments, such as precious metals, derivatives, oil and gas leases, and other non-correlated assets, can help reduce the overall volatility of your portfolio. They can also provide returns during periods when traditional asset classes underperform or are idle.

Avoid Over-Concentration in Any Single Investment:

An important aspect of diversification is ensuring your portfolio is not overly concentrated in any single investment or asset class. This includes company stock. A significant drop in the value of a single investment could have a substantial impact on your retirement plans if it constitutes a large portion of your savings.

Remember, diversification is a dynamic process, and your portfolio should be regularly reviewed and adjusted as you age to ensure it aligns with your changing risk tolerance, time horizon, and financial goals.

Investments: Where is the Money Going?

You may want to see also

Frequently asked questions

There is no hard-and-fast rule about how much you should have saved by 55, but most experts recommend around five to six times your yearly salary. T. Rowe Price suggests that by age 50, you should have saved around six times your salary.

You can invest in a 401(k), a 403(b), a traditional or Roth IRA, or a similar plan. If you're over 50, you can also take advantage of catch-up contributions, which allow you to contribute more to your retirement accounts.

It's important not to abandon stocks completely from your investment portfolio, even as you get closer to retirement. Stocks typically have higher growth potential than fixed-income investments and can help your portfolio outpace inflation.

Think about when you would like to retire and what you want your life to look like. Would you like to continue working part-time? Do you want to travel or move? Answering these questions will help you figure out how much you need to save. You can also use an online retirement calculator to get an estimate.