When it comes to investing, your portfolio mix is an important consideration. The right mix of investments can help you manage the ups and downs of the market while working towards your financial goals. One of the main factors that influence your asset allocation is your age. As you get older, your financial situation, goals, and risk tolerance may change, and your investment portfolio should reflect that. Here's how to invest and create a portfolio mix based on your age.

| Characteristics | Values |

|---|---|

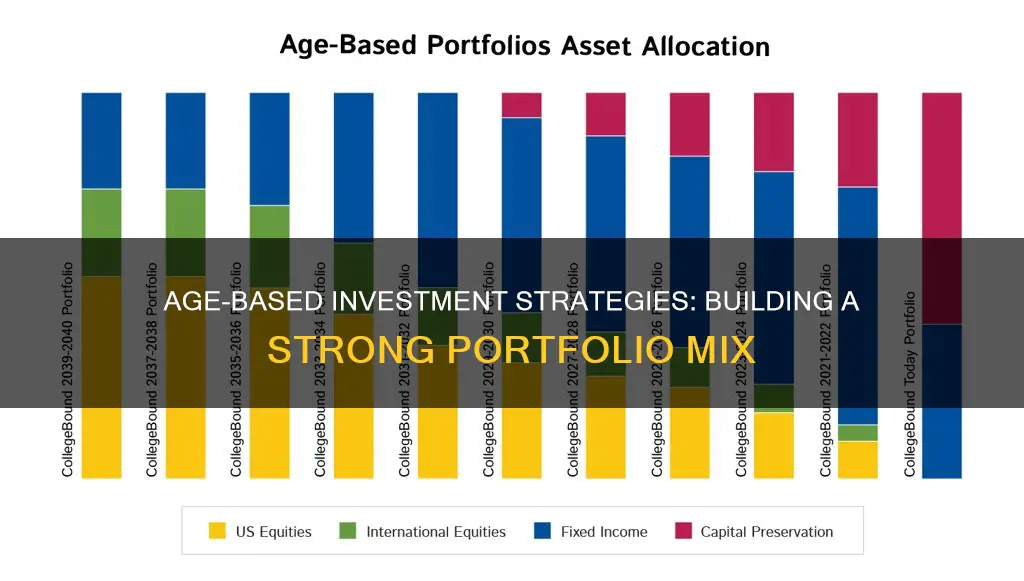

| Investors in their 20s | Place a higher percentage of their assets in cash than any other age group except retirees in their 70s |

| Investors in their 20s, 30s, and 40s | Have about a 42% allocation of US stocks and 8% allocation of international stocks in their financial portfolios |

| Investors in their 20s, 30s, and 40s | Have a bond allocation of less than 5% |

| Investors in their 50s | Keep 39.7% in US stocks and 8.4% in international stocks |

| Investors in their 60s | Keep 36.4% in US stocks and 7.8% in international stocks |

| Older investors in their 70s and over | Keep between 30% and 33% of their portfolio assets in US stocks and between 5% and 7% in international stocks |

| Younger investors | Hold a much lower percentage of their portfolio assets in bonds than middle-aged and older investors |

| Investors in their 50s | Have a total bond allocation of 8.9% |

| Investors in their 60s | Have a total bond allocation of 13.1% |

| Investors in their 20s and 30s | May want to hold most of their portfolio in stocks to help save for long-term financial goals like retirement |

| Investors in their 40s and 50s | May want to keep a hefty portion of their portfolio allocated to stocks |

| Investors in their 60s | Their allocation will likely shift toward fixed-income assets like bonds, and maybe even cash |

| Retired investors | May want to hold a mix of assets that includes stocks that might provide some growth |

![]()

Stocks allocation

Stocks are an important part of a retirement portfolio regardless of age. However, the percentage of stocks in your portfolio should decrease as you get older. Younger investors can typically afford to take more risks and allocate a higher percentage of their portfolio to stocks. As investors approach retirement, they may shift towards a more conservative asset allocation, with a higher percentage allocated to bonds and cash.

- In your 20s and 30s: Young investors in their 20s, 30s, and 40s maintain about a 42% allocation of US stocks and an 8% allocation of international stocks in their financial portfolios. They can consider an 80/20 split between stock and bond funds, taking advantage of compound interest.

- In your 40s: As you enter your peak earning years, you may still have competing financial goals, such as mortgage payments or saving for your children's education. You may want to keep a hefty portion of your portfolio allocated to stocks, especially if you haven't saved much for retirement yet.

- In your 50s: As you approach retirement, you may want to start allocating 60% of your portfolio to stocks and 40% to bonds. Adjust these numbers according to your risk tolerance.

- In your 60s: Once you hit your 60s, your allocation will likely shift towards fixed-income assets like bonds and maybe even cash. This can help prepare for the possibility of a market downturn when you retire.

- In retirement: Even after retiring, it's important to maintain a mix of assets, including stocks, to avoid outliving your savings and preserve your spending power. A conservative allocation of 50% stocks and 50% bonds is often recommended for retirees.

It's important to note that these are general guidelines, and each person's financial situation is unique. Other factors to consider when determining your stock allocation include your risk tolerance, time horizon, and investment goals.

Investment Savings: Average Amounts in the United States

You may want to see also

![]()

Bonds allocation

Bonds are an important part of any investment portfolio, and the allocation of bonds in a portfolio should be based on several factors, including age, risk tolerance, and financial goals.

Bonds are considered a less risky investment compared to stocks, as they offer steadier returns. Bond prices typically move in the opposite direction of stocks, providing a hedge against stock market volatility. This negative correlation between stocks and bonds is essential for diversifying an investment portfolio and managing risk.

When it comes to bond allocation, the general rule of thumb is that younger investors can afford to allocate a smaller percentage of their portfolio to bonds since they have a longer time horizon and can tolerate more risk. As investors approach retirement age, they may shift towards a more conservative asset allocation, increasing the percentage of bonds in their portfolio.

For example, according to the "100 minus your age" rule, a 60-year-old investor would allocate 40% of their portfolio to equities, with the remaining 60% comprising bonds, government debt, and other safe assets. However, with increasing life expectancies, some experts suggest modifying this rule to "110 minus your age" or even "120 minus your age" to account for longer lifespans and lower yields on fixed-income investments.

The "Survival Asset Allocation Model" recommends a 60/40 stock/bond portfolio for traditional retirees over 60, while the "New Life Asset Allocation Model" suggests subtracting your age from 120 to determine the percentage of stocks to hold, resulting in a higher allocation of stocks to account for longer lifespans.

It is important to note that there is no one-size-fits-all approach to bond allocation, as it depends on individual circumstances and risk tolerance. Other factors to consider when determining bond allocation include investment goals, timeline, and overall portfolio size.

Additionally, it is crucial to regularly review and rebalance your portfolio to ensure it aligns with your changing financial circumstances and goals. This may involve selling some stocks and using the proceeds to purchase bonds or other asset classes to maintain your desired asset allocation.

In conclusion, bond allocation in an investment portfolio should be tailored to the individual's age, risk tolerance, and financial goals. Younger investors typically allocate a smaller percentage to bonds, while older investors approaching retirement may increase their bond allocation to reduce risk and protect their capital.

Ally Invest: Portfolio Margin Trading Options Explored

You may want to see also

![]()

Cash allocation

Cash and cash equivalents are considered one of the least volatile types of assets, but they also offer very low returns. As a result, younger investors tend to allocate a smaller percentage of their portfolio to cash, focusing instead on stocks and bonds. However, it is important to have some cash reserves for emergencies, and financial advisors often recommend keeping at least three to six months' worth of living expenses in a savings account, money market account, or liquid CD.

According to Empower data, younger investors in their 20s place a higher percentage of their assets in cash (30.8%) than any other age group, except retirees in their 70s and older. This may be due to their relative inexperience and potential risk aversion. However, by keeping a large proportion of their financial assets in low-yielding cash instruments, young investors may be missing out on opportunities for long-term compounding to help grow their portfolios.

As you approach retirement age, you may want to increase your cash allocation to ensure you have sufficient liquid assets to cover your living expenses. Additionally, having a larger cash reserve can provide a cushion against market downturns, allowing you to avoid selling stocks during a downturn and locking in losses.

Once you have retired, your portfolio allocation is still important, and you may want to hold a mix of assets, including stocks, bonds, and cash, to help preserve your spending power. While cash and cash equivalents may not provide the same growth potential as stocks, they can offer stability and liquidity, especially if you are relying primarily on a fixed income.

In summary, while the specific percentage of cash allocation in your portfolio may vary depending on your age, financial goals, and risk tolerance, it is generally recommended to have at least a small portion of your assets in cash or cash equivalents to provide liquidity and stability to your investment portfolio.

ESG Investing: Portfolio Value and Long-Term Impact

You may want to see also

![]()

Risk tolerance

Younger investors are generally considered to have a higher risk tolerance. They can afford to take more risks as they have a longer time horizon to recover from any potential losses. As such, younger investors may allocate a higher percentage of their portfolio to stocks, which typically offer higher returns but come with greater risk.

As investors approach retirement age, their risk tolerance tends to decrease. They have less time to recover from losses, so they may shift towards a more conservative asset allocation, with a higher percentage allocated to bonds and cash, which are considered less risky investments.

However, it is important to note that age is not the only factor influencing risk tolerance. An individual's innate risk tolerance can also play a significant role. Some older investors may have a higher risk tolerance and continue to invest heavily in stocks, while younger investors may prefer a more conservative approach and opt for a more balanced portfolio.

Additionally, life circumstances can impact risk tolerance. For example, those with stable jobs and higher incomes may be more comfortable taking on risk, while those with financial dependents or caring for aging parents may have a lower risk tolerance.

Monitoring Your Investment Portfolio: How Frequently Should You Check?

You may want to see also

![]()

Retirement goals

Retirement planning is a long-term process that requires careful management of your investment portfolio. Here are some essential considerations for your retirement goals:

Start Early and Save Consistently

The power of compounding is your greatest asset when planning for retirement. The earlier you start saving and investing, the more time your money has to grow. Aim to save a portion of your income consistently and increase the amount over time as your salary increases or you pay off significant expenses.

Take Advantage of Various Accounts

Utilize a variety of accounts to maximize your retirement savings. This includes employer-sponsored plans like 401(k)s, Individual Retirement Accounts (IRAs), taxable brokerage accounts, and robo-advisor accounts. Each of these accounts offers different tax advantages and features that can benefit your overall retirement plan.

Focus on Growth Investments in Your Early Years

When you're younger, prioritize growth investments such as stocks and real estate. These investments have the potential for higher returns over time, and you have the advantage of time to ride out any market volatility.

Adjust Your Asset Allocation Over Time

As you get closer to retirement, gradually adjust your asset allocation to reduce risk. Consider moving some of your holdings into more conservative sectors, such as corporate bonds, preferred stocks, and moderate-risk instruments. This shift will help preserve your capital and provide a more stable income stream as you approach retirement.

Diversify Your Portfolio

Diversification is crucial to managing risk and stabilizing your investment returns. Diversify across different asset classes, such as stocks, bonds, cash, and alternative investments. Additionally, diversify within these asset classes by investing in individual stocks from different sectors, bond funds, and varying maturities of bonds.

Monitor Your Risk Tolerance and Time Horizon

Your risk tolerance and time horizon will change as you age. As you approach retirement, you may need to focus more on capital preservation and income generation rather than aggressive growth. Review your portfolio regularly and make adjustments as necessary to align with your changing risk tolerance and time horizon.

Seek Professional Advice

Consult financial advisors or planners to help you navigate the complexities of retirement planning. They can provide personalized advice based on your circumstances, risk tolerance, and retirement goals.

Remember, the key to successful retirement planning is to start early, save consistently, and make adjustments to your portfolio as you age to ensure your financial needs are met during your retirement years.

Rebalancing Your Investment Portfolio: How Often is Necessary?

You may want to see also

Frequently asked questions

Cash is king for investors in their 20s. They hold more assets in cash than any other age group, except retirees aged 70 or older. Investors in their 20s, 30s, and 40s have about a 42% allocation of US stocks and an 8% allocation of international stocks. Their bond allocation is less than 5%.

In your 50s, you may want to consider adding a meaningful allocation to bonds. Investors in their 50s keep 39.7% in US stocks and 8.4% in international stocks. Their total bond allocation is 8.9%.

Retirees commonly shift their focus from growth to income and stocks that provide dividend income or fixed-income bonds. Older investors in their 70s and over keep between 30% and 33% of their portfolio assets in US stocks and between 5% and 7% in international stocks.