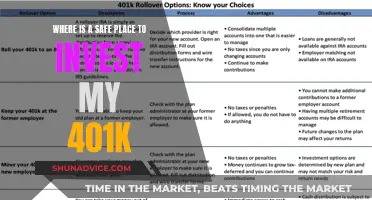

Building an investment portfolio can be a challenging task, but it is an important financial skill for active investing. A portfolio is a collection of financial investments like stocks, bonds, commodities, cash, and cash equivalents, including closed-end funds and exchange-traded funds (ETFs).

There are several steps to building an investment portfolio. Firstly, decide how much help you want and choose an account or advisor. Next, select investments that align with your preferences, goals, and risk tolerance. Then, determine the best asset allocation for you, and rebalance your portfolio as needed.

It is also important to regularly monitor your portfolio and adjust your investment strategy as life changes. This could include events such as getting married, becoming a parent, receiving an inheritance, or nearing retirement.

| Characteristics | Values |

|---|---|

| Investment portfolio definition | A collection of invested assets such as stocks, bonds, funds, real estate, and alternative investments. |

| Investment portfolios and risk tolerance | Consider your personal risk tolerance and time horizon when creating a portfolio. Your risk tolerance refers to your ability to accept investment losses in the hopes of higher returns. |

| How to build an investment portfolio | 1. Decide how much help you want. 2. Choose an account that aligns with your goals. 3. Choose your investments based on your risk tolerance. 4. Determine the best asset allocation for you. 5. Rebalance your investment portfolio as needed. |

| How to solve common portfolio problems | Focus on what you understand, set up a regular portfolio checkup schedule, do an honest risk assessment, think about risk-adjusted returns, include international investments, trim positions to get back to allocation targets, find the purpose for your positions, focus on investing rather than speculating, realise you need some risk, hold some cash and cash equivalents, start thinking about income, and seek a professional opinion. |

What You'll Learn

![]()

Choosing the right investment style

Active vs. Passive Management

The first dimension of investment style to consider is active or passive management. Active management involves hiring professional money managers to carefully select your investment holdings. Actively managed funds typically have a dedicated team of financial researchers and portfolio managers who strive for above-average returns. However, the expertise of these professionals comes at a cost, resulting in higher expenses for investors.

On the other hand, passive management, often in the form of index funds, takes a more hands-off approach. Passive funds aim to replicate the performance of a specific market index, such as the S&P 500, and generally have lower fees. Empirical research suggests that passive funds often outperform their active counterparts over the long term.

Growth vs. Value Investing

The next dimension to explore is growth versus value investing. Growth investing targets firms with high earnings growth rates, high return on equity, high profit margins, and low dividend yields. These companies are typically innovators in their field, experiencing rapid growth and reinvesting their earnings to fuel future expansion.

In contrast, value investing focuses on purchasing strong companies at attractive prices. Analysts look for low price-to-earnings ratios, low price-to-sales ratios, and higher dividend yields. Value investing is all about finding strong firms that may be undervalued by the market.

Small Cap vs. Large Cap Companies

The final dimension relates to the size of the companies you want to invest in. This decision often depends on your risk tolerance. Small-cap companies, or those with smaller market capitalizations, may offer greater growth potential and agility. However, they also carry more risk due to their limited resources, less diversified business lines, and more volatile share prices.

On the other hand, large-cap companies, such as well-established names like GE, Microsoft, and Exxon Mobil, provide more stability and dependability. While their massive size may hinder rapid growth, these companies are unlikely to go out of business unexpectedly.

Other Factors to Consider

In addition to these three primary dimensions, there are other factors to contemplate when choosing your investment style:

- Risk Tolerance: Understand your risk tolerance and ensure that your investment style aligns with it. If you have a low-risk tolerance, a conservative investment style focusing on fixed-income investments and high-quality bonds may be more suitable. Conversely, if you're comfortable with higher risk, an aggressive investment style tilted towards growth stocks or emerging markets might be appropriate.

- Investment Goals: Define your investment goals clearly. Are you investing for retirement, wealth accumulation, or income generation? Different investment styles will help you achieve different goals, so ensure your chosen style aligns with your objectives.

- Time Horizon: Consider your investment time horizon. If you're investing for the long term, you can generally take on more risk, as you have time to recover from market downturns. Conversely, if your investment horizon is short-term, a more conservative approach focusing on capital preservation may be preferable.

- Environmental, Social, and Governance (ESG) Factors: Increasingly, investors are incorporating ESG criteria into their investment decisions. If you want your investments to align with your values and have a positive impact on society and the environment, ESG investing offers a framework to evaluate companies' sustainability and ethical practices.

- Personal Understanding and Comfort: As Warren Buffett advises, invest within your circle of confidence. If you don't fully understand a particular industry or asset class, it's better to focus on what you know and find easier to comprehend.

By carefully considering these dimensions and factors, you can choose an investment style that suits your needs, preferences, and financial situation. This foundational step will help guide your investment decisions and contribute to the long-term success of your portfolio.

Creating a Diverse Investment Strategy: Portfolios to Consider

You may want to see also

![]()

Striking a balance between domestic and international

When it comes to striking a balance between domestic and international investments, it's important to recognise the benefits of diversification. While the US market has traditionally been seen as the centre of the equity world, international markets offer a range of attractive investment vehicles.

Benefits of International Investments

International investments can provide:

- Diversification: International markets can offer a range of investment opportunities that are not available in the US market. By investing in both US and international stocks, investors can reduce their risk and increase their potential returns.

- Exposure to different types of stocks: The US market tends to focus more on growth stocks, while many international markets have a stronger focus on value stocks. Therefore, an intentional tilt towards value may require more international exposure.

- Access to large multinational companies: International markets are home to some of the world's largest and most well-known companies, such as Coca-Cola, Volkswagen, and Nike. By investing internationally, investors can gain exposure to these companies and benefit from their global reach.

- Currency diversification: Investing in international markets can help investors diversify their currency exposure, as the performance of different currencies can vary over time.

Risks of International Investments

However, it's important to consider the risks associated with international investments:

- Currency risk: Changes in exchange rates can affect the value of international investments for US investors. A strengthening US dollar can lead to losses on foreign investments, while a weakening dollar can result in gains.

- Country risk: Events specific to a country, such as political instability or natural disasters, can impact the performance of investments in that country.

- Liquidity risk: Foreign stocks may have lower trading volumes, making them more difficult to buy or sell. This can also cause fluctuations in their prices.

- Higher investment costs: International investments may come with higher transaction costs and fees, impacting overall returns.

- Short-term underperformance: International markets may underperform domestic markets in the short term, requiring a longer investment horizon to realise potential gains.

Suggested Allocations

Determining the appropriate allocation between domestic and international investments is a complex decision that depends on various factors, including the investor's risk tolerance, investment goals, and time horizon. Historical data suggests that a combination of US and international stocks has generally led to higher returns and lower volatility. However, the optimal allocation can vary over time and may differ for each investor.

Choosing an Investment Portfolio: Strategies for Success

You may want to see also

![]()

Responding to fear and concerns surrounding the headlines

Communicate and Educate

When discussing market volatility with clients, advisors should maintain open and transparent communication. Educate clients about market fluctuations and emphasize the importance of staying focused on long-term financial goals. Reassess risk tolerance, review investment strategies, and highlight the benefits of a diversified portfolio to help clients navigate volatile markets.

Provide Unbiased Advice

As a financial advisor, you can leverage your emotional detachment from the performance of a given portfolio. This allows you to provide unbiased investment advice and guidance if certain assets underperform, ensuring that your client's decisions are based on research and evidence rather than emotion.

Long-Term Perspective

Encourage clients to take a long-term perspective on their investments. Remind them that short-term market fluctuations are normal and that their investment strategy is designed for long-term growth. Help them understand that reacting to every headline or news story can lead to impulsive decisions that may not align with their financial goals.

Risk Assessment and Tolerance

Assist clients in assessing their risk tolerance and adjusting their portfolios accordingly. Explain the potential impact of fixed-income investments, such as Treasury bonds, in providing ballast during volatile markets. Ensure that their portfolio aligns with their risk profile and financial objectives.

Regular Portfolio Reviews

Recommend regular portfolio check-ups to clients to stay on top of their investments. Suggest a quarterly review with additional emergency check-ins if significant market events occur. This proactive approach will help clients feel more in control and enable them to make informed decisions.

Seek Professional Guidance

Advisors should also encourage clients to seek professional guidance when needed. A financial advisor can provide personalized advice and tailored solutions based on the client's unique financial goals, circumstances, and risk tolerance. This can help alleviate fears and concerns by providing a comprehensive strategy.

Adjusting Your Investment Portfolio: Strategies for Success

You may want to see also

![]()

Building a portfolio to meet short- and long-term objectives

Building a portfolio that meets short- and long-term objectives requires a clear understanding of the investor's financial situation, goals, and risk tolerance. Here are some key considerations for constructing a portfolio to meet these objectives:

Determine Appropriate Asset Allocation:

The first step is to assess the investor's age, time horizon, capital available for investment, and future income needs. For example, a young college graduate starting their career will have different investment needs than someone nearing retirement. The investor's risk tolerance, or willingness to accept potential losses for higher returns, is also crucial. These factors will guide the allocation of assets among different classes, such as equities, bonds, and alternative investments.

Pick Individual Assets:

Once the asset allocation is determined, the next step is to select specific investments for the portfolio. This involves choosing stocks, bonds, mutual funds, exchange-traded funds (ETFs), or other securities that align with the desired asset allocation and the investor's risk profile. Stocks can be selected based on sector, market capitalisation, and company characteristics. Bonds should be evaluated based on coupon rate, maturity, type, and credit rating. Mutual funds and ETFs offer diversification and professional management but come with management fees.

Monitor and Reassess Weightings:

The portfolio's performance and weightings should be regularly monitored to ensure they remain aligned with the investor's goals and risk tolerance. Changes in price movements can cause the initial weightings to shift, requiring adjustments. Periodically reassessing the portfolio helps identify overweighted and underweighted positions and make necessary changes.

Rebalance Strategically:

When rebalancing the portfolio, consider the tax implications of selling certain assets. For example, selling appreciated assets may trigger capital gains taxes. Additionally, assess the outlook for overweighted securities; if they are expected to decline, it may be beneficial to sell despite the tax implications. Remember to maintain diversification across asset classes, sectors, and industry sectors.

Liquidity and Short-Term Goals:

While long-term objectives are important, it's also crucial to consider the investor's short-term needs and liquidity requirements. The portfolio should include a mix of long-term investments and more liquid assets that can be easily accessed for unexpected expenses or short-term goals. This ensures that the investor doesn't feel locked into long-term investments and can meet their immediate financial obligations.

Retirement Investments: Best Places for Your Savings

You may want to see also

![]()

Understanding risk tolerance

Understanding your risk tolerance is a critical aspect of building an investment portfolio. Risk tolerance refers to your ability to accept investment losses while also considering the potential for higher investment returns. It is influenced by your mental and emotional capacity to handle market fluctuations and is tied to your financial goals and time horizon.

When determining your risk tolerance, it's important to be honest with yourself. Consider how much loss you are truly comfortable with and assess your appetite for risk. Remember that your risk tolerance should significantly influence the content of your portfolio. If you have a low-risk tolerance, you may want to adopt a conservative strategy that focuses on lower-risk securities to protect your portfolio's value. On the other hand, if you have a high-risk tolerance, you may be willing to take on greater risks in search of greater returns.

It's also important to understand that your risk tolerance may change over time as your financial goals and circumstances evolve. For example, as you get closer to retirement, you may want to shift your portfolio towards more conservative assets to protect your savings. Conversely, if you are just starting your investment journey, you may be more comfortable taking on more risk, as you have more time to recover from potential losses.

Additionally, your risk tolerance should be considered in conjunction with other factors, such as your investment objectives, time horizon, and personality. All of these elements will help guide the construction of your investment portfolio and ensure it aligns with your financial goals and comfort level.

By assessing your risk tolerance, you can make more informed decisions about the types of investments that are suitable for your portfolio and strike a balance between risk and potential returns.

The Perfect Investment Portfolio: Strategies for Success

You may want to see also