Utility functions are a key concept in economics, measuring the welfare or satisfaction a consumer derives from a product or service. In finance, utility functions can be used to understand how much benefit an investor obtains from a portfolio's performance. This is particularly useful when assessing an investor's relationship with risk, as risk and return are trade-offs. Utility functions can be used to mathematically optimise investment decisions, helping investors make choices that align with their risk attitudes and strategies. While utility is challenging to quantify due to individual differences, it can be measured in dollars in certain cases. Understanding utility functions can also help companies make strategic decisions in sales, marketing, and product development.

| Characteristics | Values |

|---|---|

| Purpose | To measure the welfare or satisfaction of a consumer as a function of the consumption of real goods |

| Application | Used in rational choice theory to analyze human behavior |

| Use in Finance | Refers to how much benefit investors obtain from portfolio performance |

| Utility Function | U(X1, X2, X3, Xn) |

| Utility Curve Types | Risk-Averse, Risk-Neutral, Risk-Loving |

| Marginal Utility | The utility gained by consuming an additional unit of a service or good |

| Ordinal Utility | Ranks choices by preference |

| Cardinal Utility | Assigns a numeric value to the consumer's preference |

What You'll Learn

![]()

Understanding utility functions in economics

In economics, utility functions are used to measure the welfare or satisfaction of a consumer as a function of the consumption of goods and services. Utility functions are widely used in rational choice theory to analyse human behaviour. Utility functions assign a numerical value to the utility or satisfaction a consumer receives from a product or service, allowing economists to track and compare consumer choices.

Utility functions are often used by companies to guide their sales and marketing plans, advertising, and new product offerings. For example, a company may use utility functions to determine which products within their product line are preferred by consumers, and then use this information to enhance product development and gain a competitive advantage.

There are two main types of utility functions: ordinal utility and cardinal utility. Ordinal utility ranks choices by preference, without assigning a numerical value to the utility received. On the other hand, cardinal utility measures the utility received from a choice by assigning a numerical value to it.

When measuring utility, economists often refer to the concept of total utility and marginal utility. Total utility refers to the overall satisfaction or benefit a person receives from consuming a product or service. Marginal utility, on the other hand, measures the additional satisfaction or benefit a person gains from consuming one extra unit of a product or service.

It is important to note that utility functions are ordinal rather than cardinal. This means that utility functions only rank bundles of goods or services based on preferences, without indicating how much better one bundle is compared to another. For example, if bundle A provides 10 utils and bundle B provides 20 utils, it does not mean that bundle B is twice as good, but only that it is preferred over bundle A.

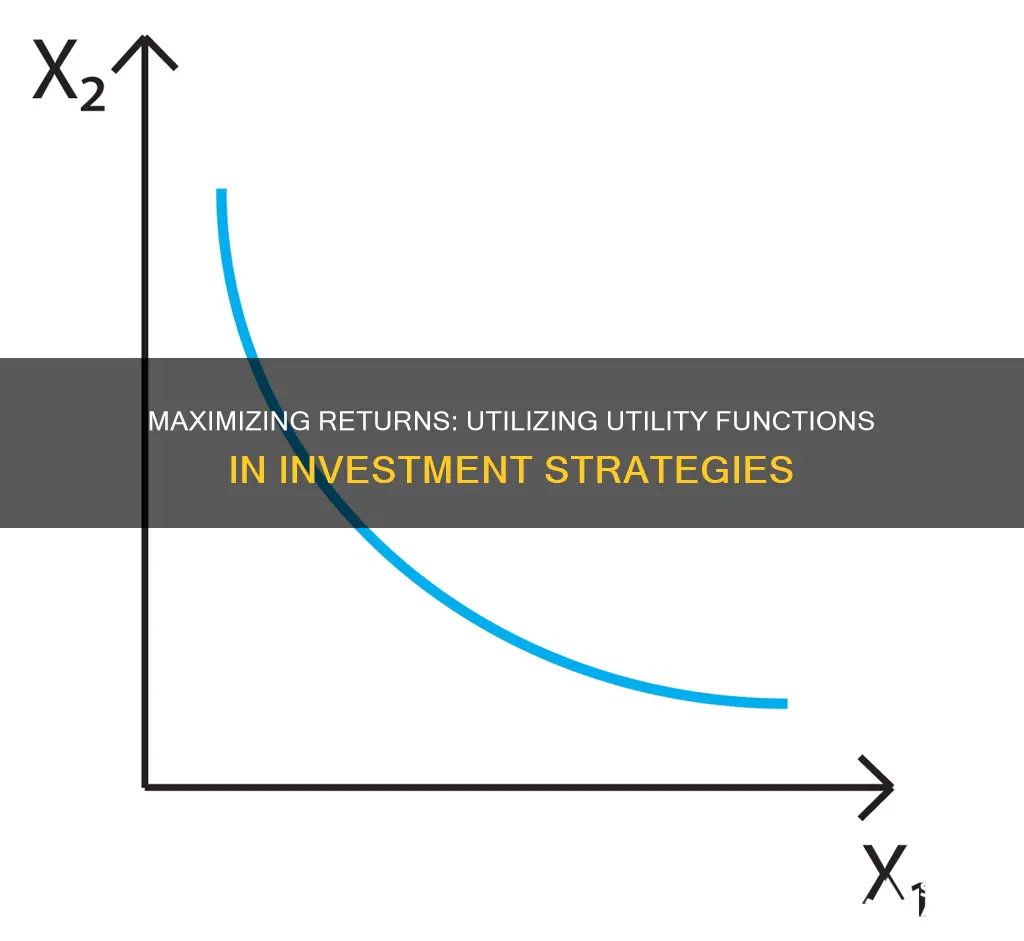

Utility functions can also be represented graphically using indifference curves, which show combinations of commodities that provide the same level of satisfaction to an individual. These curves can be used to derive individual demand curves by combining them with budget constraints.

In summary, utility functions are a powerful tool used in economics to understand and predict consumer behaviour by quantifying the satisfaction or welfare gained from consuming different goods and services.

Fidelity Investments: Are They Fiduciaries?

You may want to see also

![]()

How utility functions can be used to inform investment strategies

Utility functions can be used to inform investment strategies in several ways.

Firstly, utility functions can help investors understand their risk attitudes and make investment decisions that align with their risk tolerance. By quantifying the utility or satisfaction derived from different investments, investors can assess the trade-off between risk and return. For example, an investor with a utility function that values a $2,000 increase in portfolio value at 1 util may prefer a lower-risk investment with consistent returns over a high-risk investment with the potential for higher returns but also a greater chance of loss.

Secondly, utility functions can be used to determine the optimal portfolio allocation for an investor. By plotting the utility function, known as an indifference curve, alongside the capital allocation line (CAL), which connects a risk-free asset with a portfolio of risky assets, the optimal portfolio can be found at the tangent point between the two. The CAL reflects the expected return on an investor's portfolio based on the level of risk measured by the standard deviation.

Additionally, utility functions can provide insights into an investor's attitude towards risk. There are three types of utility curves that describe an investor's relationship with risk: risk-averse, risk-neutral, and risk-loving. A risk-averse investor's utility curve will flatten as they become less willing to take on additional risk, while a risk-loving investor will experience increasing marginal utility, and their curve will slope upward.

Furthermore, utility functions can be applied to financial planning decisions, such as asset allocation and retirement spending. By quantifying an individual's preferences and trade-offs, financial advisors can provide recommendations that are mathematically optimized for their clients' preferences and risk tolerance.

However, it is important to note that defining an individual's utility function can be challenging, as it is an abstract concept that varies across individuals and can change over time as they gain experience or face new situations.

Understanding Cash Investing Activities: A Beginner's Guide

You may want to see also

![]()

The benefits of using utility functions for financial planning

Utility functions are an essential tool in finance, providing a mathematical representation of investor preferences and risk tolerance. They are used to quantify the satisfaction or utility an individual derives from different levels of wealth or investment outcomes. Understanding utility functions is crucial for making informed financial decisions, optimizing portfolios, and modelling investor behaviour.

Key Concepts of Utility Functions in Finance

The principle of risk aversion is central to utility functions in finance. Risk-averse investors favour a certain outcome over a riskier option with a potentially higher return. Utility functions capture this behaviour mathematically, assigning a numerical value to different levels of wealth that reflects the investor's satisfaction.

The concept of diminishing marginal utility is another key aspect. As wealth increases, the additional satisfaction from an extra unit of wealth decreases. This explains why investors may opt for a diversified portfolio instead of investing all their resources in a single high-risk, high-reward venture. The diminishing marginal utility makes riskier investments less appealing as the incremental benefit of additional wealth is lower.

Benefits of Using Utility Functions for Financial Planning

Informed Decision-Making:

Utility functions enable individuals to make more informed financial decisions by mathematically quantifying their preferences and the trade-offs involved. This helps individuals navigate the complexities of financial planning, especially when dealing with uncertain future events.

Optimized Portfolios:

By incorporating utility functions, investors can construct portfolios that align with their risk preferences and financial goals. Utility functions allow for a personalized approach to portfolio management, maximizing expected utility rather than solely focusing on expected returns. This comprehensive assessment considers both returns and associated risks.

Dynamic Portfolio Management:

Utility functions facilitate the use of advanced techniques such as stochastic programming and dynamic optimization. These methods account for the uncertainty and variability of future returns, enabling more robust portfolio construction. By modelling the investor's utility function, these techniques can adapt asset allocations to changing market conditions and evolving investor preferences, enhancing long-term financial stability.

Customized Investment Strategies:

Financial advisors can leverage utility functions to tailor investment recommendations to individual clients. By understanding a client's unique risk profile and financial objectives, advisors can propose portfolios that reflect their preferences. This personalized approach improves client satisfaction and fosters a deeper understanding of the client's financial needs.

Behavioural Finance Insights:

Utility functions in behavioural finance explore the psychological aspects of investor behaviour, offering insights into how real-world decisions deviate from traditional economic models. By adapting utility functions to capture these complexities, analysts can gain a more accurate representation of investor preferences, including the impact of cognitive biases, emotions, and social factors.

In conclusion, utility functions offer a powerful framework for financial planning, enabling individuals and advisors to make more informed decisions, optimize portfolios, and tailor investment strategies. By mathematically representing investor preferences and risk tolerance, utility functions provide valuable insights for navigating the complexities of financial planning and investment decision-making.

Retirement Investing: Strategies for Your Golden Years

You may want to see also

![]()

The challenges of defining an individual's utility function

Utility functions are a key criterion in decision-making processes, especially in the evaluation of project criteria. They are used to assess the value or usefulness of a set of criteria, and in economics, they are used to measure the satisfaction or welfare of a consumer as a function of the consumption of real goods.

However, defining an individual's utility function is challenging due to its abstract nature. Here are some of the challenges:

- Subjectivity of Preferences: Utility functions are based on an individual's preferences, which can vary widely. An ice cream lover might assign a higher utility value to ice cream than cookies, but another person might prefer cookies over ice cream. These preferences are subjective and unique to each individual.

- Dynamic Preferences: People's preferences can change over time. For example, a person's utility function for choosing a home might prioritize proximity to downtown today, but in a few years, their preferences might shift towards a quieter neighbourhood.

- Complexity of Trade-offs: Utility functions are often used to evaluate trade-offs, such as the decision between higher risk and higher potential returns in investing. However, people may struggle to accurately assess these trade-offs, especially when they involve distant or abstract future consequences.

- Income and Wealth Effects: It is challenging to define the point at which further income or wealth increases experience a significant decline in marginal utility, especially for individuals who have never experienced high levels of wealth.

- Loss Aversion: Utility functions typically reflect the concept of loss aversion, where losses are weighted more heavily than comparable gains. However, this can be difficult to quantify, as individuals may experience varying degrees of loss aversion.

- Risk Tolerance: Risk tolerance is another factor that influences utility functions. Some individuals are risk-averse, while others are risk-neutral or even risk-loving. This variation in risk tolerance can impact the shape and slope of the utility function.

- Indifference: In some cases, individuals may be indifferent between two alternatives, assigning them the same utility value. This indifference can make it challenging to define a clear preference order and construct an accurate utility function.

- Measurement Challenges: Utility functions attempt to quantify satisfaction or welfare, but these concepts can be abstract and difficult to measure directly. While economists use "utils" as a unit of measurement, it is challenging to assign true numerical values to an individual's level of satisfaction.

Understanding Dividend Investing: Yield on Cash

You may want to see also

![]()

How utility functions can be applied to portfolio selection

Utility functions are a key component of modern portfolio theory, which was introduced in Harry Markowitz's 1952 doctoral thesis. This theory assumes that investors aim to maximise their portfolio's expected return while maintaining a prescribed amount of risk. Portfolios that meet this criterion are known as "efficient portfolios".

Utility functions can be applied to portfolio selection by using a specific utility function that reflects an investor's risk preferences and expected utility. This utility function can be based on various factors, such as the expected return, standard deviation, and risk aversion of a portfolio.

For example, the utility function for an investment can be represented as:

> U = E(r) - 1/2 * A * σ^2

Where:

- U = utility of an investment

- E(r) = expected return

- A = risk aversion coefficient

- Σ^2 = variance of the investment

By plotting this utility function as an indifference curve, investors can determine the combination of risk and returns that would provide them with a given level of utility.

Additionally, the capital allocation line (CAL) is a visual representation of an investor's portfolio, connecting a risk-free asset with the portfolio of risky assets. The CAL reflects the expected return of an investor's portfolio based on the level of risk, measured by the standard deviation.

By finding the tangent point between the CAL and the indifference curve, investors can identify their optimal portfolio. This optimal portfolio will provide the highest level of utility for a given level of risk.

Overall, utility functions are a valuable tool for investors to make informed decisions about their portfolios by considering their risk preferences and expected utility.

Invest Your Weekly Cash Wisely: A Guide to Getting Started

You may want to see also

Frequently asked questions

A utility function is a mathematical way to quantify how a person evaluates decisions and trade-offs by assigning values to outcomes to reflect their relative weighting.

Utility theory takes into account an investor's subjective perception of risk. The utility function assigns a particular utility value – or level of satisfaction – to a given monetary value. An investor's utility function for a particular investment can be described in terms of risk and return.

Utility is difficult to quantify as it varies between individuals and is an abstract concept. However, dollars can sometimes be used as a quantitative measure. Marginal utility refers to the incremental benefit an individual derives from obtaining one additional unit of a good or service.

Utility functions can be used to help craft recommendations for clients by mathematically optimising the "best" portfolio or retirement solution over a time horizon. This gives proper weight to both near-term outcomes and the consequences of future uncertain events.