When it comes to planning for your retirement, one of the most important decisions you can make is whether to invest in your employer's 401(k) plan or to manage your investments independently. Both options have their advantages and disadvantages, and understanding these can help you make an informed choice. In this paragraph, we'll explore the key factors to consider, such as the benefits of employer matching contributions, the potential for tax advantages, and the flexibility of self-directed investments, to help you decide which path is right for your financial goals and risk tolerance.

What You'll Learn

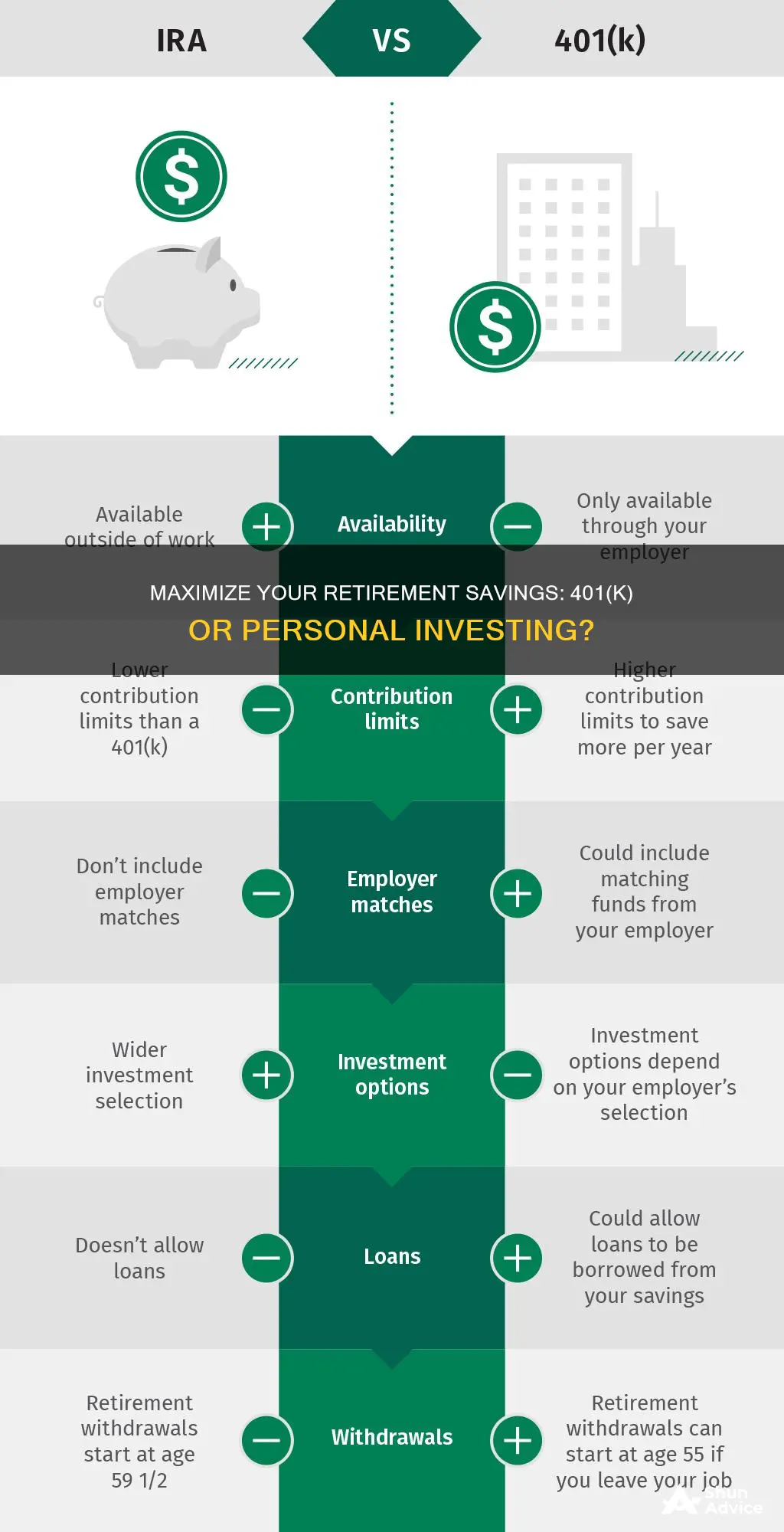

- Tax Benefits: 401(k)s offer tax advantages, allowing contributions to be made pre-tax, reducing taxable income

- Employer Matching: Many employers match contributions, providing free money and boosting savings

- Diversification: 401(k)s offer access to a wide range of investment options for diversified portfolios

- Fee Structure: Compare fees of 401(k)s and personal investments to ensure cost-effectiveness

- Liquidity and Flexibility: 401(k)s offer flexibility in withdrawals, unlike some personal investment accounts

![]()

Tax Benefits: 401(k)s offer tax advantages, allowing contributions to be made pre-tax, reducing taxable income

When considering whether to utilize your employer's 401(k) plan or invest independently, it's essential to understand the tax benefits associated with each option. One of the most significant advantages of a 401(k) is the tax-deferred status it provides. By contributing to a 401(k), you can make pre-tax contributions, which means your money is invested before taxes are taken out. This results in a reduction of your taxable income for the year, potentially lowering your overall tax liability. For example, if you contribute $1,000 to your 401(k) before taxes, you will have $1,000 less in taxable income, which can be beneficial, especially if you are in a higher tax bracket.

The tax benefits of a 401(k) extend beyond the contribution itself. As your investments grow tax-free within the account, you won't owe taxes on the earnings until you start making withdrawals in retirement. This allows your savings to compound over time, potentially growing significantly. Additionally, many 401(k) plans offer a variety of investment options, allowing you to diversify your portfolio and potentially earn higher returns compared to investing on your own.

In contrast, investing independently may not provide the same tax advantages. While you can still benefit from tax-efficient strategies like tax-loss harvesting and tax-efficient mutual funds, you won't have the same level of tax-deferred growth as you would in a 401(k). Traditional brokerage accounts are typically subject to taxes on capital gains and dividends, which can eat into your investment returns.

Furthermore, the power of compound interest is maximized within a 401(k) due to its tax-deferred nature. As your investments grow, the earnings are reinvested, and the process repeats, potentially leading to substantial growth over the long term. This is particularly advantageous for retirement savings, as it allows your money to work harder for you.

In summary, the tax benefits of a 401(k) are a compelling reason to consider using it. The ability to make pre-tax contributions reduces your taxable income and provides tax-deferred growth on your investments. While investing independently has its advantages, the tax advantages of a 401(k) can be a significant factor in your decision-making process, especially when planning for retirement.

Unveiling the Secrets: Decisive Questions to Ask Your Broker Before Buying an Investment Property

You may want to see also

![]()

Employer Matching: Many employers match contributions, providing free money and boosting savings

Employer matching is a significant advantage of using a 401(k) plan at work. When you contribute to your 401(k), many employers will match a portion of your contribution, essentially providing you with free money. This employer match can significantly boost your savings and is a valuable opportunity that should not be overlooked. The amount of the match varies depending on the employer and can range from a small percentage of your contribution to a full match, sometimes even exceeding your contributions. For example, if your employer offers a 50% match, for every dollar you contribute, they will add another 50 cents, effectively doubling your savings. This is a powerful incentive to save more and can make a substantial difference in your retirement savings over time.

This employer-provided benefit is a form of immediate financial gain, as it increases your savings without requiring any additional effort or cost from your side. It's like getting a free bonus on top of your regular contributions. By taking advantage of this match, you are essentially working with a financial partner who is invested in your long-term financial success. This can be a more substantial incentive than the potential tax benefits of contributing to a 401(k), as the employer match provides an immediate and tangible return on your investment.

The key to maximizing this benefit is to contribute enough to qualify for the full match. Employers often have specific contribution limits or percentages that they will match. It's essential to understand these rules to ensure you are getting the most out of this opportunity. For instance, if your employer matches up to 6% of your pay, aim to contribute at least that amount to your 401(k) to get the full benefit. This strategy ensures that your savings grow faster and that you are not leaving free money on the table.

Additionally, employer matching can be a powerful motivator to save regularly and consistently. Knowing that your employer is contributing to your retirement savings can encourage you to make regular contributions, even if it's just a small amount. This habit of consistent saving can lead to significant financial gains over your working years. It's a win-win situation, as you benefit from the match, and your future self will thank you for the head start on retirement savings.

In summary, employer matching is a compelling reason to use a 401(k) plan at work. It provides free money, boosts your savings, and encourages consistent saving habits. Understanding your employer's matching policy and contributing enough to qualify for the full match is essential to making the most of this valuable benefit. By taking advantage of employer matching, you can set yourself up for a more secure financial future and potentially retire with more substantial savings.

First-Time Homebuyers: Unlocking the Secrets to Successful Property Investment

You may want to see also

![]()

Diversification: 401(k)s offer access to a wide range of investment options for diversified portfolios

When considering your retirement savings strategy, one of the key benefits of utilizing a 401(k) plan offered by your employer is the opportunity for diversification. Diversification is a crucial investment principle that involves spreading your assets across various types of securities to reduce risk. In the context of a 401(k), this means having access to a broad array of investment options, which can be a powerful tool for building a well-rounded retirement portfolio.

A typical 401(k) plan provides participants with a selection of investment funds, often including a mix of stocks, bonds, and sometimes alternative investments. This variety allows investors to construct a diversified portfolio right from the start. For instance, you might choose to invest a portion of your 401(k) in large-cap stocks, which are generally considered less volatile, and another portion in small-cap or international stocks, which can offer higher growth potential but may be more risky. By doing so, you're not only managing risk but also potentially maximizing returns over the long term.

The beauty of diversification within a 401(k) is that it often requires less effort from the investor. When you have a wide range of investment options available, you can easily allocate your contributions across these different asset classes. This approach simplifies the investment process, as you don't need to research and select individual stocks or bonds. Instead, you can rely on the expertise of the plan's investment managers who have already made these selections.

Moreover, diversification in a 401(k) can be particularly advantageous for those who are just starting to build their retirement savings. It provides a solid foundation for long-term growth, allowing investors to benefit from the power of compounding returns over time. As your investments mature, you can further adjust your portfolio to align with your risk tolerance and retirement goals.

In summary, the availability of diverse investment options within a 401(k) plan is a significant advantage for investors. It enables you to create a well-diversified portfolio, manage risk effectively, and potentially achieve your retirement objectives. This aspect of 401(k) plans often makes them an attractive and efficient way to save for the future, especially when combined with the potential tax advantages and employer contributions that many of these plans offer.

Saving and Investing: Finding the Right Balance

You may want to see also

![]()

Fee Structure: Compare fees of 401(k)s and personal investments to ensure cost-effectiveness

When considering whether to invest in a 401(k) plan offered by your employer or to manage your investments independently, understanding the fee structure is crucial for making an informed decision. The fees associated with both options can significantly impact your long-term financial growth. Here's a breakdown of how to compare and evaluate the costs:

K) Fees:

- Management Fees: These are charged by the 401(k) plan's investment manager or the mutual funds/exchange-traded funds (ETFs) within the plan. Management fees can vary widely, typically ranging from 0.1% to 1% of the assets under management. Lower-cost index funds or ETFs often have more competitive fees.

- Recordkeeping and Administrative Fees: These fees cover the administrative tasks associated with maintaining your 401(k) account, such as processing contributions, distributing statements, and ensuring compliance with tax laws. These fees are usually a small percentage of your account balance.

- Plan Management Fees: If your 401(k) plan is provided by a third-party administrator, there may be additional fees for setting up and managing the plan, which can vary based on the complexity of the plan.

Personal Investment Fees:

- Brokerage Fees: If you choose to invest outside of your 401(k), you'll need to consider the fees charged by your brokerage firm. These can include account maintenance fees, trading commissions, and sometimes a per-transaction fee. Online brokerages often offer lower fees compared to traditional full-service brokers.

- Mutual Fund or ETF Fees: If you invest in mutual funds or ETFs, you'll pay management fees, which are typically lower than those of actively managed funds. These fees are usually a percentage of the fund's assets and are paid to the fund's manager.

- Taxes: Personal investments may be subject to capital gains taxes when you sell them, which can impact your overall returns.

Comparing Cost-Effectiveness:

- Calculate the total fees for both options over a year and then compare them to your overall investment returns. Lower fees generally result in higher net returns for your investments.

- Consider the potential for tax advantages, such as tax-deferred growth in a 401(k) or tax-efficient strategies when investing personally.

- Evaluate the level of diversification and investment options available in each plan. A well-diversified 401(k) might offer more choices, but personal investments can provide more control over your portfolio.

- Review the plan's performance and track record, especially if you're considering a 401(k) with a specific investment strategy.

By carefully examining the fee structures, you can make a more informed decision about whether to utilize your employer's 401(k) or take control of your investments personally, ensuring that your retirement savings grow efficiently.

Valic Retirement Investment Options: A Comprehensive Review

You may want to see also

![]()

Liquidity and Flexibility: 401(k)s offer flexibility in withdrawals, unlike some personal investment accounts

When considering your retirement savings options, the concept of liquidity and flexibility is an important aspect to evaluate. This is especially relevant when comparing a 401(k) plan, offered by your employer, to personal investment accounts. Understanding the differences in liquidity and flexibility between these two options can significantly impact your financial decisions.

A 401(k) plan provides a level of liquidity that many personal investment accounts cannot match. With a 401(k), you have the freedom to withdraw funds from your account, subject to certain rules and penalties. This flexibility allows you to access your money when needed, whether for a major purchase, an emergency, or any other financial requirement. For instance, if you encounter a significant financial setback or need to cover unexpected expenses, you can typically withdraw funds from your 401(k) without incurring the same level of restrictions as you might face with a personal investment account.

In contrast, personal investment accounts often come with more stringent withdrawal rules. These accounts may have penalties for early withdrawals, and the process of accessing your funds can be more complex and time-consuming. For example, if you decide to sell investments in a personal account before a specified holding period, you might face penalties or taxes, making it less flexible for short-term financial needs.

The flexibility of a 401(k) is particularly beneficial for those who may require access to their savings for various reasons. It provides a safety net, ensuring that you can address financial obligations or take advantage of opportunities without the same level of restriction as personal investment accounts. This aspect of liquidity and flexibility is a significant advantage, especially for individuals who value the ability to control and access their funds according to their unique circumstances.

Additionally, the 401(k) plan's flexibility can be advantageous for those who may need to make significant financial decisions or adjustments. It allows for more immediate access to funds, which can be crucial in certain situations. This level of liquidity is a unique feature of 401(k)s and can be a compelling reason to consider this option as part of your retirement savings strategy.

Black Americans: Investors or Not?

You may want to see also

Frequently asked questions

It's a common dilemma! While employer-sponsored 401(k) plans offer convenience and potential tax advantages, self-directed investing gives you more control. Consider your risk tolerance, time commitment, and financial goals. Research and understand the fees and investment options in your 401(k) before making a decision.

Traditional 401(k)s offer tax-deductible contributions and tax-deferred growth, while Roth 401(k)s provide tax-free growth and withdrawals in retirement. Roth 401(k)s are ideal if you expect to be in a higher tax bracket during retirement. Traditional 401(k)s are better if you want to reduce your taxable income in the contribution year.

Employer-matched contributions are essentially free money! Many employers offer matching contributions, which can significantly boost your savings. Additionally, 401(k) plans often provide a range of investment options, low fees, and the ability to borrow from your account in emergencies.

Withdrawing funds from a 401(k) before age 59½ typically incurs a 10% early withdrawal penalty, plus income tax on the distribution. However, there are exceptions. You can withdraw your contributions (not earnings) tax-free and penalty-free at any time. Some plans also allow hardship withdrawals for specific reasons, but these are subject to penalties and taxes.

Even without an employer match, contributing the maximum allowed to your 401(k) can still be beneficial. You can contribute up to $19,500 in 2023, plus an additional $6,500 if you're age 50 or older. Consider adjusting your budget to allocate more funds to your retirement savings. Self-employed individuals can also contribute to a Solo 401(k) or a SEP IRA to maximize tax benefits.