A DSCR loan, or Debt Service Coverage Ratio loan, is a type of non-QM loan that allows investors to streamline the typical qualifying mortgage process and benefit from more flexible underwriting requirements. DSCR loans are used to help investors secure home financing without having to apply for traditional Texas home loans. These loans are specifically designed for borrowers investing in real estate and are based on the rental income of a property rather than personal finances.

| Characteristics | Values |

|---|---|

| Purpose | Help investors secure home financing without having to apply for traditional Texas home loans |

| Type of Loan | Non-QM loan |

| Qualification | Based on the property's DSCR and other financial metrics such as credit score and down payment amount |

| Repayment | Through the rental income the property earns |

| Applicability | Cannot be used to purchase owner-occupied property |

| Lender | Griffin Funding, Visio Lending, LBC Mortgage, District Lending, and TxPremierMortgage |

| Interest-Only Payment Options | Available |

| Terms | 30-year terms with no balloons |

| Interest Rate and Terms | Influenced by factors such as the property type, loan-to-value ratio, borrower's credit score, and the DSCR itself |

| Property Types | Single-family homes, multi-family units, commercial real estate, and mixed-use buildings |

| Income Verification | Not required |

| Employment History Verification | Not required |

| Credit Score | Required |

| Down Payment | Required (20% to 30% of the property's purchase price) |

What You'll Learn

![]()

DSCR loans are a type of non-QM loan

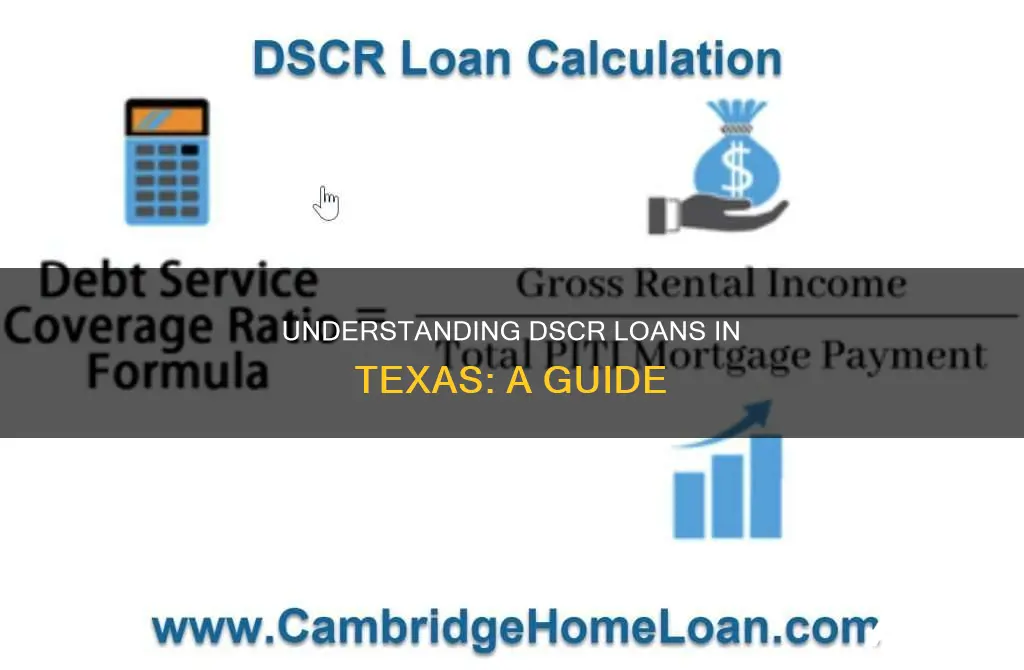

The main advantage of a DSCR loan is that it allows borrowers to qualify for financing based on the projected or actual rental income of a property rather than their personal income or financial history. This means that investors do not need to provide proof of income or employment history verification, making it a popular choice for those who may struggle to secure other types of loans. The debt service coverage ratio (DSCR) is calculated by dividing the property's annual rental income by its annual debt obligations, including principal, interest, taxes, insurance, and HOA fees if applicable. A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow. Most lenders look for a DSCR of 1.2 or higher, but some may accept a lower ratio depending on the property type and risk involved.

DSCR loans also offer flexible lending criteria and faster approval processes than traditional loans. Investors can benefit from interest-only loans, rate buy-downs, prepayment penalty buy-downs, and rate structure choices. Additionally, DSCR loans can help investors expand their portfolios by allowing them to leverage the funds from the loan to invest in multiple properties, diversifying their investments and enhancing their potential for long-term profitability.

However, there are some drawbacks to consider. DSCR loans are aimed specifically at investors, which may exclude other types of borrowers. Additionally, the eligibility for these loans assumes that the property has a good DSCR ratio, which may not be the case for all properties. Vacancies in the rental property can also hinder cash flow and impact the ability to repay mortgage debt obligations.

Becoming a Loan Signing Notary: A Step-by-Step Guide

You may want to see also

![]()

They are used to secure financing for investment properties

DSCR loans are a popular choice for investors in Texas as they are more flexible than other loans. They are specifically designed for borrowers investing in real estate and can be used for both residential and commercial properties if the property generates income.

DSCR loans are a type of non-QM loan that allows investors to streamline the typical qualifying mortgage process and benefit from more flexible underwriting requirements. They are used to secure financing for investment properties by enabling real estate investors to qualify for financing based on the rental income of a property rather than their personal finances. This means that investors can qualify for a loan without providing proof of income or employment history verification.

The debt service coverage ratio (DSCR) is a number that measures a property's current rental income compared to its debt obligations. A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow. Lenders use the DSCR to determine how much of a loan can be supported by the income coming from the property.

DSCR loans can be used to purchase investment properties, including long-term rentals like multi-family housing and short-term rentals like vacation properties. They can also be used for cash-out refinances, where investors replace their mortgage loan with a new loan for a higher loan amount and use the difference to buy more properties.

Overall, DSCR loans provide investors with a flexible financing option for investment properties in Texas, allowing them to secure funding based on the income potential of the property rather than their personal finances.

Exclusive Access: Members-Only Group Benefits

You may want to see also

![]()

Lenders are looking for a DSCR of 1.25

Lenders are typically looking for a Debt Service Coverage Ratio (DSCR) of 1.25 when considering loan applications. This is because a DSCR of 1.25 indicates that the rental income of a property is high enough to cover loan payments when they are due, including in the event of unforeseen circumstances such as unexpected vacancies or repairs.

The DSCR is a financial ratio that compares a company's operating income to its debt payments. In the context of real estate investment, the DSCR measures a property's rental income against its debt obligations. A DSCR of 1.25 indicates that a property's income is 25% higher than what is necessary to repay the loan. This is considered a strong ratio, demonstrating financial stability and a positive cash flow.

Lenders use the DSCR to assess the financial health of a company or investment property and to determine whether there is sufficient income to meet principal and interest obligations. A higher DSCR can lead to more favourable loan terms, such as lower interest rates and less stringent requirements.

DSCR loans in Texas are a popular choice for investors as they offer more flexible lending criteria and faster closing times. These loans are specifically designed for borrowers investing in real estate and are based on the rental income of a property rather than personal finances.

Unitranche Loans: Understanding This Unique Debt Financing Option

You may want to see also

![]()

DSCR loans offer more flexible lending criteria

DSCR loans are a type of non-QM loan that allows investors to streamline the typical qualifying mortgage process and benefit from more flexible underwriting requirements. They are designed for real estate investors and can only be used to purchase income-generating properties.

The debt service coverage ratio (DSCR) is a number that measures a property's current rental income compared to its debt obligations. A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow. A DSCR loan enables real estate investors to qualify for financing based on the rental income of a property rather than personal finances.

DSCR loans also offer flexibility in terms of property types. Investors can use these loans to finance single-family homes, multi-family units, commercial properties, and even mixed-use buildings. They can also be used for short-term rentals and long-term rentals.

Additionally, DSCR loans often feature higher loan limits and flexible terms, enabling investors to acquire larger properties or multiple units, enhancing portfolio growth opportunities. They can also be tailored to meet the investor's needs, with options such as interest-only loans, rate buy-downs, and prepayment penalty buy-downs.

Becoming a Loan Signing Agent: Florida's Requirements

You may want to see also

![]()

DSCR loans can be used for short-term rentals

DSCR loans are a great option for investors looking to finance short-term rental properties. Unlike conventional loans, DSCR loans allow investors to qualify for financing based on the projected rental income of a property rather than their personal income or financial information. This makes it easier for those with non-traditional incomes to get approved for an investment property loan.

DSCR, or Debt Service Coverage Ratio, is a number that measures a property's current rental income against its debt obligations. A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow. Lenders use this metric to determine whether the property can "pay for itself" without relying on the borrower's personal income.

DSCR loans are particularly useful for short-term rental properties because they often offer faster closing times and more flexible requirements. For example, investors can qualify for DSCR loans without providing proof of income or employment history verification. This makes it a good option for those who have had trouble securing other types of loans. Additionally, DSCR loans can be used to finance multiple properties, which is ideal for investors looking to build a large real estate portfolio.

When considering a DSCR loan for a short-term rental property, it's important to keep in mind that these loans typically require a relatively large down payment and proof of cash reserves. However, with the growing demand for short-term rentals and the popularity of platforms like Airbnb, DSCR loans can be a valuable tool for investors looking to expand their investment property portfolios.

The True Cost of Capital: Which Financing Option Costs Most?

You may want to see also

Frequently asked questions

DSCR stands for Debt Service Coverage Ratio. It is a financial tool used by real estate investors to finance property acquisitions.

DSCR loans are based on the rental income of a property rather than the borrower's personal income. Lenders use the DSCR to determine how much of a loan can be supported by the income coming from the property.

DSCR loans offer more flexibility in terms of property types and income verification. They also have faster approval processes and higher loan limits, enabling investors to acquire larger properties or multiple units.

DSCR loans are designed for real estate investors and can only be used to purchase income-generating properties. Borrowers must meet minimum credit score requirements and provide a down payment of at least 20%.

The Debt Service Coverage Ratio is calculated by dividing the property's annual Net Operating Income (NOI) by its annual debt service, which includes principal, interest, taxes, insurance, and HOA fees if applicable.