Investing for retirement is a long-term strategy that requires careful planning and consideration. The best investments for retirement offer a balance between growth and safety, allowing individuals to build their wealth while managing risk. Here are some options to consider:

- High-yield savings accounts: These accounts provide easy access to funds and are suitable for those who need their money in the near future or prefer a risk-averse approach. While they are considered safe, there is a risk of losing purchasing power over time due to inflation if the interest rates are too low.

- Long-term certificates of deposit (CDs): CDs are issued by banks and typically offer higher interest rates than savings accounts. They are a good choice for retirees who don't need immediate income and can lock up their funds for a fixed period. CDs carry reinvestment risk, but they can provide a higher return during the term.

- Long-term corporate bond funds: These funds invest in bonds issued by corporations and offer higher returns than government or municipal bond funds. They are suitable for investors seeking cash flow or those looking to reduce portfolio risk while earning a return.

- Dividend stock funds: Dividend stocks provide consistent income in the form of cash or additional stock payouts. While not all stocks pay dividends, dividend stock funds offer a diversified collection of dividend-paying stocks, reducing the risk associated with individual stocks.

- Value stock funds: These funds invest in stocks that are bargain-priced compared to the market, making them attractive options during periods of high stock valuations. Value stock funds tend to be safer than other stock funds but are still subject to market fluctuations.

- Small-cap stock funds: Small-cap funds invest in stocks of smaller companies with strong growth prospects. They offer the potential for significant returns but carry higher risk due to the less established nature of the underlying companies.

- Real estate investment trusts (REITs): REITs provide diversified exposure to real estate and offer substantial dividend payouts. They are suitable for income-focused investors and can provide both capital appreciation and dividend income.

- S&P 500 index funds: These funds are based on a diverse range of large American companies, offering broad exposure to the stock market. They are suitable for beginners and those seeking a well-diversified investment with potential for higher returns than traditional banking products or bonds.

- Nasdaq-100 index funds: Nasdaq-100 index funds provide exposure to some of the biggest tech companies. They offer growth potential but come with significant volatility due to the high valuation of the underlying stocks.

- Rental housing: Investing in rental properties can generate regular cash flow but requires active management and the ability to deal with tenants and maintenance issues.

| Characteristics | Values | |

|---|---|---|

| Investment type | High-yield savings accounts, long-term certificates of deposit, long-term corporate bond funds, dividend stock funds, value stock funds, small-cap stock funds, real estate investment trusts, S&P 500 index funds, Nasdaq-100 index funds, rental housing, annuities, bonds, stocks, cash-value life insurance plans, nonqualified deferred compensation plans, defined contribution plans, traditional pensions, guaranteed income annuities, cash-balance plans, IRAs, robo-advisors, target date funds, rental property, QLACs | |

| Risk level | Low: high-yield savings accounts, long-term certificates of deposit, long-term corporate bond funds, dividend stock funds, robo-advisors, target date funds, annuities, bonds, defined contribution plans, IRAs | |

| Medium: value stock funds, small-cap stock funds, real estate investment trusts, S&P 500 index funds, Nasdaq-100 index funds, rental housing, stocks, cash-value life insurance plans, nonqualified deferred compensation plans, traditional pensions, guaranteed income annuities, cash-balance plans | ||

| High: value stock funds, small-cap stock funds, stocks | ||

| Time horizon | Long-term: long-term certificates of deposit, long-term corporate bond funds, dividend stock funds, value stock funds, small-cap stock funds, real estate investment trusts, S&P 500 index funds, Nasdaq-100 index funds, rental housing, stocks, nonqualified deferred compensation plans, traditional pensions, guaranteed income annuities, cash-balance plans, IRAs | |

| Short-term: high-yield savings accounts |

What You'll Learn

![]()

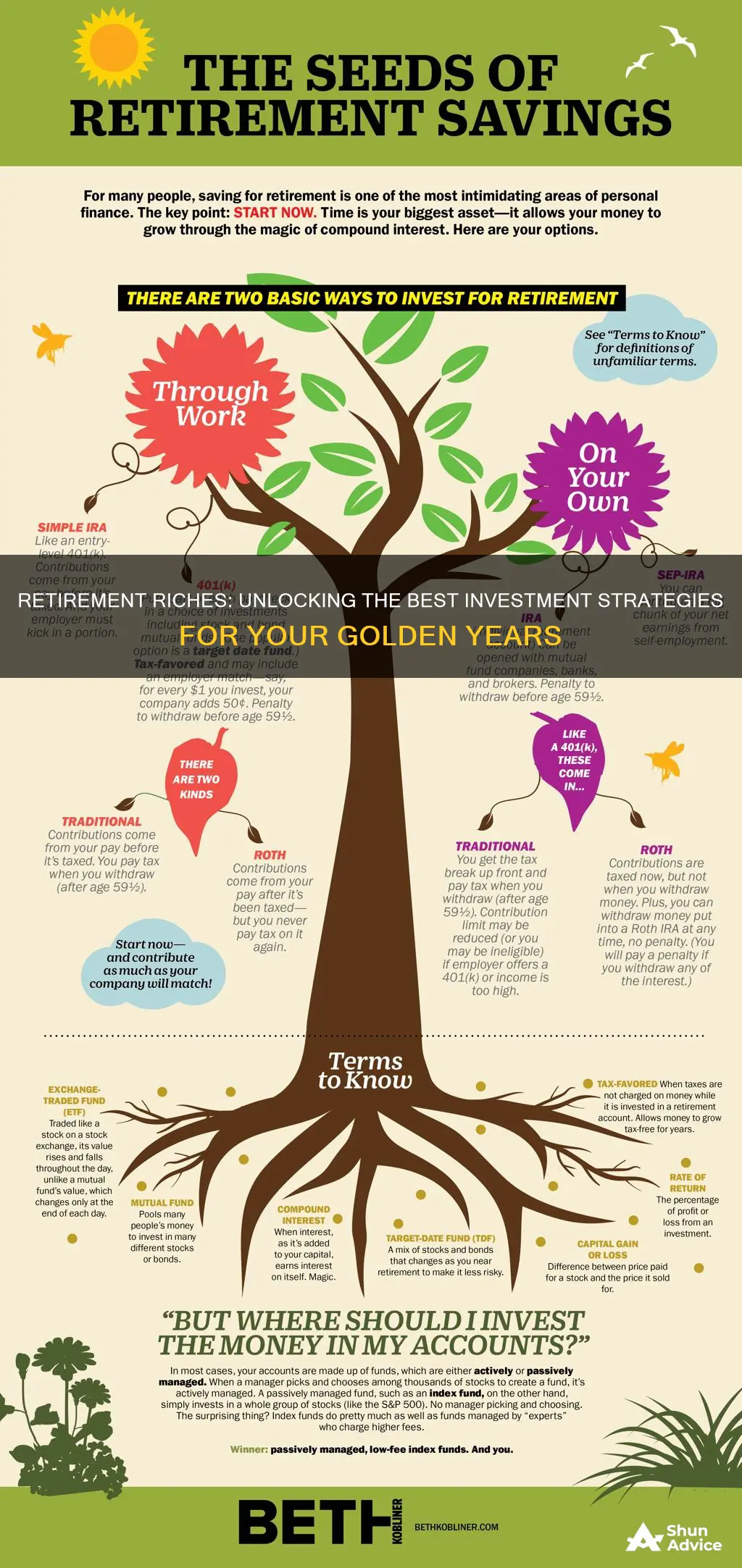

Tax-advantaged accounts

Tax-Deferred Accounts

Tax-deferred accounts allow you to reduce your taxable income now and postpone paying taxes on your earnings until later. Examples of tax-deferred accounts include:

- Traditional 401(k) plans: These are the most common type of tax-advantaged account. You contribute to them with pre-tax money, and your contributions and investment gains are taxed when you withdraw them in retirement. Many employers offer matching contributions, which can boost your savings.

- Traditional Individual Retirement Accounts (IRAs): These are tax-deferred accounts that individuals can use to save for retirement. Contributions may be tax-deductible, and earnings are untaxed until withdrawal.

- SEP IRAs: These are similar to traditional IRAs but are designed for self-employed individuals and small business owners. They have higher contribution limits and allow for profit-sharing.

- SIMPLE IRAs: These are designed for small businesses and offer higher contribution limits than traditional IRAs. They may include employer matching contributions.

Tax-Exempt Accounts

Tax-exempt accounts allow you to contribute after-tax dollars, and your earnings and withdrawals are tax-free. Examples of tax-exempt accounts include:

- Roth 401(k) plans: These are similar to traditional 401(k) plans but are funded with after-tax dollars. Withdrawals are not taxed as long as certain rules are followed.

- Roth IRAs: These are the tax-exempt counterpart to traditional IRAs. Contributions are made with after-tax money, and withdrawals can be made tax-free. Roth IRAs offer flexibility, as you can withdraw your contributions without penalty. However, there are income limits for contributing to these accounts.

- 529 college savings plans: These are tax-exempt accounts that can be used to save for college or other qualifying educational expenses. Earnings and withdrawals are tax-free at the state and federal levels.

- Health Savings Accounts (HSAs): These accounts offer a triple tax advantage: contributions are made pre-tax, earnings grow tax-free, and withdrawals are tax-free when used for qualified health care expenses. HSAs can also be used as a supplemental retirement account, as funds can be withdrawn penalty-free for any purpose after age 65.

Investments After Loss: A New Chapter

You may want to see also

![]()

Asset allocation

Stocks

Stocks are a common feature of retirement portfolios because of their potential for growth. They can help investors keep pace with inflation and taxes, which is particularly important for retirees who are living on a fixed income. However, stocks are more volatile than other investments, so they may not be suitable for risk-averse retirees.

Bonds

Bonds are a good way to reduce risk and diversify your portfolio. They provide regular income through periodic payments and are generally less volatile than stocks. Bond funds are another good income option, offering robust yields and stability.

Cash

Having cash on hand means retirees won't have to worry as much about the markets or their monthly paycheck. It's recommended to set aside one year's worth of cash in a safe, liquid account, such as an interest-bearing bank account or money market fund. This cash reserve can be used to cover living expenses and replenish investment portfolios.

Other Investments

In addition to stocks, bonds, and cash, retirees may also consider the following investments:

- High-dividend blue-chip stocks: These offer stability, regular income, and the potential for stock appreciation.

- Bank certificates of deposit (CDs): CDs offer higher interest rates than other deposit accounts and allow you to lock in a fixed rate for a specific period.

- Money market funds: These are low-risk and stable, offering high credit quality, short maturities, and high liquidity.

- Income-producing equities: Some equities provide income in the form of dividends, offering a regular stream of income and the opportunity for capital appreciation.

- Annuities: Annuities can provide a guaranteed income stream for a certain period or for life. They offer tax-deferred growth, flexibility, and the potential for payments to continue for beneficiaries after death. However, annuities may have limited liquidity and are subject to the claims-paying abilities of the insurance company.

- High-yield savings accounts: In the current interest rate environment, these accounts can earn meaningful interest with limited risk.

The right asset allocation for retirement will depend on your individual circumstances and goals. It's important to consider your time horizon, risk tolerance, current and future income sources, and investment objectives when determining the appropriate mix of investments for your portfolio.

Telephone Bill Conundrum: Expense or Investment?

You may want to see also

![]()

Robo-advisors or target-date funds

Robo-advisors and target-date funds (TDFs) are both popular investment options for people who want a hands-off approach to building and managing a portfolio. However, they are designed for different situations and achieve that goal in different ways. Here is a detailed comparison between the two to help you decide which one might be more suitable for your retirement planning:

Robo-Advisors

Robo-advisors are digital services that use algorithms and investor surveys to build and manage personalised client portfolios. They offer a good middle ground for those who want a hands-off approach but do not want to work with a human advisor. Here are some key features of robo-advisors:

- Personalised Portfolios: Robo-advisors survey each investor about their financial situation, risk tolerance, time horizon, and goals to formulate a tailored mix of assets designed to meet their individual needs. This level of personalisation is generally not available with target-date funds.

- Flexibility: Robo-advisors can be used for various investment goals, including retirement, saving for a home, or other expenses. They can also use more advanced investment strategies, such as tax-loss harvesting, to potentially increase returns.

- Management and Advisory Fees: Robo-advisors typically charge a management fee, which is a percentage of your invested assets. For example, Betterment charges $4 per month for accounts under $20,000, while Wealthfront and Betterment charge 0.25% for accounts over $20,000. These fees are in addition to the expense ratios charged by the mutual funds or exchange-traded funds (ETFs) used in the portfolio.

- Account Maintenance: Robo-advisors automate routine account maintenance tasks such as rebalancing and tax-loss harvesting, which can help reduce taxes on capital gains.

- Minimum Investment Requirements: Robo-advisors usually have low or no minimum investment requirements, making them accessible to a wide range of investors. For example, Betterment has no minimum balance requirement, while Wealthfront requires a $500 minimum balance.

Target-Date Funds (TDFs)

Target-date funds, on the other hand, are mutual funds designed for retirement savings and are often the default investment option in employer-sponsored retirement programs, such as 401(k) plans. Here are some key characteristics of TDFs:

- Retirement Focus: TDFs are specifically designed to help individuals save for retirement by choosing a target year, usually decades in the future. The fund's asset allocation becomes more conservative as the target date approaches, reducing volatility and risk.

- Simplicity: TDFs offer a simple, one-stop-shop solution for investors. You choose the fund with a target date closest to your retirement year, and the fund automatically adjusts its holdings over time. This makes TDFs a good option for those who want a completely hands-off approach.

- Fees: TDFs typically only charge an expense ratio, which can be lower than the combined fees of a robo-advisor's management fee and the expense ratios of the underlying funds. For example, Vanguard's target-date funds have low expense ratios of around 0.17%. However, some TDFs may have expense ratios exceeding 1%.

- Glide Path: The glide path refers to the gradual reduction of equity allocation as the target date nears. This path can vary between fund providers, with some levelling off before retirement ("to" retirement) and others continuing to adjust after retirement ("through" retirement).

- Limited Personalisation: TDFs do not offer the same level of personalisation as robo-advisors. Investors choose the fund closest to their retirement year, and the underlying investments are predetermined by the fund manager.

- Availability: TDFs are widely available in taxable accounts and are commonly

In summary, robo-advisors offer more personalisation, flexibility, and advanced investment strategies but tend to be more expensive due to the management fees. On the other hand, target-date funds are specifically designed for retirement savings, offering a simple, hands-off approach with lower fees. When deciding between the two, consider your investment goals, desired level of involvement, and fee structure to determine which option aligns best with your retirement planning needs.

Retirement Plans and Investment Portfolios: What's the Difference?

You may want to see also

![]()

Dividend-paying stocks

When considering dividend-paying stocks, it's important to look for companies with a reliable history of consistent or steadily increasing dividend payouts. Some stocks tend to pay higher dividends than others, and it's crucial to review a company's dividend-paying history before investing. Additionally, dividend-paying stocks may become less attractive as interest rates rise, so it's important to consider the current economic climate when making investment decisions.

- AT&T (T): This telecom company has managed to score a key breakout above price resistance, offering investors both price gains and a consistent dividend stream with a yield of about 5.7%.

- British American Tobacco PLC (BTI): This tobacco company has experienced significant price gains in 2024 and offers a dividend yield of over 8%.

- Eversource Energy (ES): As a defensive sector stock, Eversource Energy operates in the utilities sector, which has seen an improvement in July 2024. The stock has a dividend yield of around 4.5%.

- Altria Group Inc. (MO): Altria is a tobacco company that manufactures and sells cigarettes, smokeless tobacco, and alcoholic beverages. It offers a rich dividend of 8.52%.

- BXP Inc. (BXP): Formerly known as Boston Properties, BXP operates as a real estate investment trust, developing and managing Class A properties. It pays a sizable dividend of 6.46%.

- Chevron Corp. (CVX): This American multinational energy corporation specializes in oil and gas and offers a rich dividend of 4.17%.

- Pfizer Inc. (PFE): As a top pharmaceutical stock, Pfizer offers a hefty dividend of 5.95%, which has risen annually for the past 14 years.

- United Parcel Service Inc. (UPS): This well-known stock offers a forward dividend yield of 4.4%.

- CubeSmart (CUBE): CubeSmart is another option with a higher dividend yield of 4.8%.

- Colgate-Palmolive (CL): This company has a top share in the U.S. and abroad and has managed raw materials price swings well, offering a steady dividend payout.

- Johnson & Johnson (JNJ): Johnson & Johnson has raised its dividend for over 50 years and owns well-known brands such as Aveeno, BAND-AID, Motrin, Neutrogena, Johnson's Baby, and Tylenol.

- PepsiCo: PepsiCo offers a diversified business model with a snack food division and a beverage unit, providing a stable income stream.

- S&P Global (SPGI): S&P Global provides independent ratings, benchmarks, analytics, and data to capital and commodity markets worldwide. The company has paid a dividend every year since 1937 and has excellent margins and an enviable track record.

- Stanley Black & Decker (SWK): This company is well-known for its brands, including Dewalt, Black+Decker, Craftsman, Stanley, and Troy-Bilt. The stock is off its pre-pandemic levels, offering a nice entry point and a 3.6% yield.

- Walmart: Walmart has a solid dividend track record and is expected to continue growing its dividend payouts.

These examples demonstrate the range of dividend-paying stocks available to investors. It's important to conduct thorough research and consult with a financial professional before making any investment decisions.

GME: Invest Now or Never?

You may want to see also

![]()

Annuities

There are four basic types of annuities:

- Fixed vs. Variable Annuities: Fixed annuities offer a predetermined, guaranteed rate of return, whereas variable annuities base returns on the performance of a basket of stocks and bonds, providing more growth potential but also higher risk.

- Immediate vs. Deferred Annuities: With immediate annuities, individuals pay a lump sum and immediately begin receiving regular payments. Deferred annuities are a long-term tool, where payments are collected at a specified future date, allowing time for interest accrual or market gains.

The benefits of annuities include:

- Income for Life: Annuities provide income that generally lasts for life, ensuring retirees have a steady stream of income to supplement Social Security.

- Deferred Distributions: Annuities offer tax-deferred status, meaning individuals only pay taxes when they withdraw funds, providing control over tax payments.

- Guaranteed Rates: Fixed annuities offer predetermined, guaranteed rates of return, providing a predictable income stream.

However, there are also drawbacks to annuities:

- Hefty Fees: Annuities often come with high upfront costs and annual expenses, which can be comparable to the cost of a managed portfolio.

- Lack of Liquidity: Many annuities have surrender fees for early withdrawals, making it difficult and expensive to back out of the contract.

- Higher Tax Rates: Withdrawals from annuities are taxed as ordinary income, which can be higher than capital gains tax rates.

- Complexity: Annuities are complex financial products, with numerous exotic variations, making it challenging for investors to fully understand what they are purchasing.

When considering annuities for retirement, it is essential to weigh the pros and cons. Annuities offer a guaranteed income stream but come with complex contracts and high fees. They may be suitable for those seeking peace of mind and a secure income stream, but individuals with sufficient retirement savings may want to maximise their 401(k) or IRA before investing in annuities.

Young Investors: Emulate Warren Buffett's Strategy

You may want to see also

Frequently asked questions

Safe investments for retirees include high-yield savings accounts, long-term certificates of deposit, and annuities.

Medium-risk investments for retirees include corporate bonds, dividend-paying stocks, and real estate investment trusts (REITs).

High-risk, high-reward investments for retirees include growth stocks, such as small-cap stocks, and stock index funds, such as the S&P 500 or Nasdaq-100.

Retirees can generate income by finding part-time work, investing in rental properties, or purchasing an annuity.

When choosing retirement investments, it's important to consider your risk tolerance, time horizon, knowledge of investing, financial situation, and how much you can invest. Diversifying your investments across different asset classes and geographic regions can also help reduce risk.