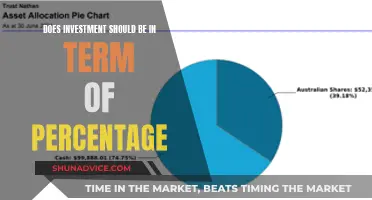

The fintech industry has seen tremendous growth and innovation in recent years, attracting significant investments from various sources. Among the many sub-domains within fintech, the payments and digital banking sector has emerged as the largest in terms of investments. This domain encompasses a wide range of services, including online and mobile payments, digital wallets, peer-to-peer lending, and virtual banking. The rapid adoption of digital payment methods and the increasing demand for convenient and secure financial services have fueled the growth of this sector, making it a highly attractive investment opportunity for venture capitalists, investors, and financial institutions alike.

What You'll Learn

- Payment Processing: Handling money transfers, from mobile wallets to online banking

- Lending & Credit: Platforms for borrowing and lending money, including peer-to-peer lending

- Blockchain & Cryptocurrency: Decentralized finance, digital currencies, and smart contracts

- RegTech: Regulatory technology for compliance and risk management in fintech

- Neobanks & Digital Banking: New digital-only banks disrupting traditional banking models

![]()

Payment Processing: Handling money transfers, from mobile wallets to online banking

The payment processing sector within fintech is a critical component of the global financial infrastructure, facilitating the seamless transfer of funds across various platforms. This domain has witnessed significant growth and investment in recent years, driven by the increasing demand for digital payment solutions and the rapid expansion of e-commerce. As consumers and businesses alike embrace digital transactions, the need for efficient, secure, and scalable payment processing systems has become paramount.

Payment processing involves a complex network of technologies and intermediaries, ensuring that money moves smoothly from one party to another. This process encompasses various touchpoints, including point-of-sale (POS) terminals, online payment gateways, mobile wallets, and traditional banking systems. The evolution of payment processing has been marked by a shift towards digital channels, with mobile and online payments gaining prominence.

Mobile wallets, such as Apple Pay, Google Pay, and Samsung Pay, have revolutionized the way consumers make payments. These digital wallets enable users to store payment information securely on their devices, allowing for contactless and convenient transactions. The integration of mobile wallets with online banking systems further enhances the user experience, providing a seamless and integrated payment solution. For instance, users can initiate a payment from their online banking platform and then use their mobile wallet to complete the transaction, ensuring a smooth and efficient process.

Online banking platforms have also played a pivotal role in the growth of payment processing. These platforms offer a range of services, including money transfers, bill payments, and peer-to-peer transactions. With the rise of digital banking, customers increasingly prefer managing their finances online, driving the need for robust and secure payment processing systems. Online banking providers invest heavily in security measures to protect customer data and ensure the integrity of transactions, which is crucial for maintaining trust in the digital economy.

The payment processing industry is characterized by its high-volume, low-margin nature, requiring efficient operational strategies. Companies in this domain focus on optimizing transaction speeds, minimizing costs, and ensuring compliance with regulatory standards. The use of advanced technologies, such as machine learning and artificial intelligence, is becoming prevalent to detect and prevent fraudulent activities, enhance security, and personalize user experiences. As the fintech industry continues to evolve, payment processing will remain a critical area of investment, driving innovation and shaping the future of global financial transactions.

Understanding Term Sheets: A Guide to Investment Agreements

You may want to see also

![]()

Lending & Credit: Platforms for borrowing and lending money, including peer-to-peer lending

The lending and credit sector is a significant and rapidly growing area within the fintech industry, attracting substantial investments globally. This domain encompasses various platforms and services that facilitate borrowing and lending money, offering an alternative to traditional financial institutions. One of the most prominent sub-sectors within this category is peer-to-peer (P2P) lending, which has gained immense popularity and investment in recent years.

P2P lending platforms act as intermediaries, connecting individual borrowers and lenders directly. These platforms disrupt the traditional banking system by enabling borrowers to access loans without the need for a bank, and lenders to earn interest by funding these loans. The process typically involves a thorough credit assessment of the borrower, often using advanced data analytics and machine learning algorithms, to determine the risk and interest rate. This approach has proven to be highly effective, especially for those who might not have access to traditional credit or have been deemed high-risk by banks.

The rise of P2P lending can be attributed to several factors. Firstly, the global financial crisis of 2008 highlighted the limitations of the traditional banking system, prompting many to seek alternative financial solutions. Secondly, the advent of digital technology and the internet has made it easier for these platforms to operate, allowing for faster and more efficient transactions. As a result, P2P lending has become a preferred choice for both borrowers and lenders, especially in regions with underdeveloped banking systems or those seeking more competitive interest rates.

Several well-known companies have emerged in this space, such as Lending Club, Prosper, and ZestMoney, each offering unique features and services. These platforms often provide quick access to credit, competitive interest rates, and flexible repayment options, making them attractive to a wide range of borrowers. For lenders, the opportunity to earn higher returns compared to traditional savings accounts is a significant draw.

The lending and credit sector, particularly P2P lending, has not only disrupted the traditional financial industry but has also created a new, vibrant market. This domain continues to attract significant investments, with venture capitalists and financial institutions recognizing the potential for growth and innovation. As the sector evolves, it is likely to further challenge and transform the way money is lent and borrowed, offering more accessible and efficient financial services to a global audience.

Maximizing SIP Returns: Top Investment Strategies for Long-Term Growth

You may want to see also

![]()

Blockchain & Cryptocurrency: Decentralized finance, digital currencies, and smart contracts

Blockchain and cryptocurrency have emerged as significant disruptors in the financial technology (fintech) industry, attracting substantial investments and reshaping traditional financial systems. This domain has captured the attention of investors, entrepreneurs, and institutions worldwide due to its potential to revolutionize various aspects of finance.

Decentralized finance (DeFi) is a key area within blockchain and cryptocurrency that has gained immense popularity. DeFi aims to recreate traditional financial services, such as lending, borrowing, and trading, on a decentralized network, eliminating the need for intermediaries like banks. By utilizing smart contracts, DeFi platforms enable peer-to-peer transactions, ensuring security, transparency, and accessibility. This has led to the creation of various decentralized applications (DApps) that offer services like stablecoin issuance, decentralized exchanges, and automated market-making protocols. The rapid growth of DeFi has been fueled by the increasing demand for financial inclusion and the desire for more efficient and cost-effective financial services.

Cryptocurrencies, the digital or virtual currencies secured by cryptography, have played a pivotal role in this domain. Bitcoin, the first and most well-known cryptocurrency, introduced the concept of decentralized ledger technology, known as blockchain. Blockchain, a distributed database, ensures secure and transparent transactions by recording them in a chain of blocks. This technology has not only underpinned the success of cryptocurrencies but has also found applications in various other sectors. Smart contracts, self-executing contracts with the terms of the agreement directly written into code, further enhance the capabilities of blockchain. They enable automated and secure transactions, reducing the need for intermediaries and minimizing potential fraud.

The investments in blockchain and cryptocurrency have been substantial, with venture capital firms, institutional investors, and government bodies showing interest. The total investment in blockchain startups reached an estimated $4.1 billion in 2020, with a significant portion allocated to DeFi projects. Cryptocurrency markets have also experienced tremendous growth, with the total market capitalization surpassing $2 trillion in 2021. This growth has attracted investors seeking high returns and has led to the development of numerous blockchain-based projects, including decentralized exchanges, NFT platforms, and blockchain-based identity solutions.

In summary, the blockchain and cryptocurrency domain has become a significant focus for investors due to its potential to transform traditional finance. Decentralized finance, with its ability to provide accessible and efficient financial services, has been a major driver of investment. Cryptocurrencies and blockchain technology, coupled with smart contracts, offer a secure and transparent alternative to conventional financial systems. As the industry continues to evolve, further innovations and investments are expected, shaping the future of finance and potentially attracting even more attention from the global investment community.

Unraveling the World of Short-Term Investments: Strategies and Benefits

You may want to see also

![]()

RegTech: Regulatory technology for compliance and risk management in fintech

The financial technology, or fintech, industry has seen tremendous growth and investment in recent years, with various sectors attracting significant attention. Among these, RegTech, or regulatory technology, has emerged as a crucial and rapidly expanding domain. RegTech focuses on leveraging technology to streamline and automate compliance and risk management processes within the fintech space, ensuring that financial institutions adhere to ever-evolving regulations.

In the context of fintech, RegTech plays a pivotal role in addressing the complex and often stringent regulatory requirements that fintech companies must navigate. These requirements are particularly challenging due to the dynamic nature of the industry and the rapid pace of technological advancements. As fintech innovations continue to disrupt traditional financial services, regulatory bodies worldwide are implementing new rules to ensure consumer protection, market stability, and fair competition.

RegTech solutions are designed to help fintech firms efficiently manage these regulatory obligations. These technologies automate various compliance tasks, such as reporting, monitoring, and data management. For instance, RegTech platforms can automatically extract and analyze large volumes of data, ensuring that financial institutions meet reporting deadlines and identify potential risks or non-compliance issues promptly. This automation not only reduces the likelihood of human error but also allows compliance teams to focus on more strategic tasks, enhancing overall operational efficiency.

One of the key advantages of RegTech is its ability to provide real-time insights and analytics. By utilizing advanced analytics and machine learning algorithms, RegTech systems can identify patterns, trends, and anomalies in financial data, helping companies detect and mitigate risks more effectively. This is particularly crucial in the fintech sector, where the potential for fraud, money laundering, and other financial crimes is ever-present. RegTech solutions can enhance fraud detection systems, improve customer due diligence processes, and facilitate more efficient and accurate risk assessments.

Moreover, RegTech enables fintech companies to stay agile and adaptable in a rapidly changing regulatory environment. As regulations evolve, RegTech platforms can be updated and customized to incorporate new requirements, ensuring that compliance remains a dynamic and responsive process. This adaptability is essential for fintech firms to maintain their competitive edge while adhering to the necessary legal and ethical standards. In summary, RegTech is a vital component of the fintech ecosystem, offering innovative solutions to manage compliance and risk, thereby fostering a more robust and secure financial industry.

The Long-Term Viability of Land as an Investment: Exploring Opportunities and Risks

You may want to see also

![]()

Neobanks & Digital Banking: New digital-only banks disrupting traditional banking models

The rise of neobanks and digital-only banking models has been a significant trend in the fintech industry, attracting substantial investments and disrupting the traditional banking landscape. These innovative financial institutions, often referred to as 'neobanks' or 'challenger banks,' offer a fresh approach to banking by leveraging technology and digital platforms to provide convenient, accessible, and often more affordable financial services. This shift towards digital-only banking has been fueled by the increasing demand for personalized, user-friendly banking experiences, especially among younger generations who are comfortable with technology.

Neobanks typically operate without a physical branch network, relying entirely on online and mobile banking platforms. They focus on delivering a seamless digital experience, allowing customers to open accounts, manage their finances, and access a range of financial products and services from their smartphones or computers. This model has been made possible by advancements in fintech, enabling secure online transactions, real-time payments, and integrated financial management tools. By cutting out the overhead costs associated with traditional brick-and-mortar banks, neobanks can offer lower fees and more competitive interest rates, attracting customers seeking better value.

One of the key advantages of neobanks is their ability to quickly adapt to market trends and customer preferences. They can launch new products and services at a rapid pace, often responding to customer feedback and market demands within days or weeks. This agility allows them to stay ahead of the competition and continuously improve their offerings. For instance, many neobanks have introduced features like instant account opening, automated financial advice, and peer-to-peer payments, all designed to enhance customer convenience and engagement.

The success of neobanks has attracted significant investments from various sources, including venture capital firms, large financial institutions, and even tech giants. These investments have fueled the growth of the industry, enabling neobanks to expand their customer bases, improve their technology infrastructure, and offer more comprehensive services. As a result, the neobank market has become increasingly competitive, driving innovation and forcing traditional banks to reevaluate their strategies to stay relevant.

In conclusion, the neobank and digital banking sector represents a substantial and rapidly growing segment of the fintech industry. Its success lies in its ability to provide a more personalized, efficient, and customer-centric banking experience. With continued investments and technological advancements, these digital-only banks are set to further disrupt the traditional banking models, forcing established institutions to adapt and evolve to meet the changing demands of the market and their customers. This evolution in the banking industry highlights the power of fintech to drive innovation and create new opportunities in the financial services sector.

Maturity Transformation: Unlocking Long-Term Investment Potential

You may want to see also