In the realm of finance, understanding the nuances between different types of investments is crucial for making informed decisions. One such distinction is between current investments and short-term investments, which often raises questions among investors. While both terms are related to financial assets, they represent distinct approaches to managing money. Current investments typically refer to assets held for a relatively short period, often with a focus on liquidity and quick access to funds. On the other hand, short-term investments are a subset of current investments, emphasizing a more aggressive strategy to maximize returns within a limited timeframe. This introduction aims to explore the differences and similarities between these two investment strategies, shedding light on how they can be utilized effectively in various financial scenarios.

What You'll Learn

- Investment Timeframe: Understanding the difference in duration between current and short-term investments

- Risk Tolerance: How risk appetite influences investment choices

- Liquidity: The ease of converting investments into cash

- Tax Implications: Tax considerations for long-term vs. short-term gains

- Market Volatility: Impact of market fluctuations on investment strategies

![]()

Investment Timeframe: Understanding the difference in duration between current and short-term investments

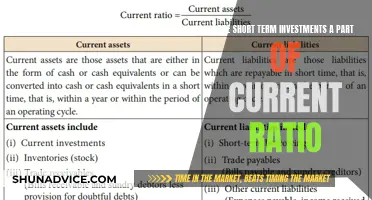

The terms "current investments" and "short-term investments" are often used in the financial world, but they represent different concepts and time horizons. Understanding the distinction between these two types of investments is crucial for investors to make informed decisions and manage their portfolios effectively.

Current Investments:

Current investments typically refer to assets or securities that are held for a relatively short period, often within a year or less. These investments are usually made with a focus on liquidity and the ability to quickly convert them into cash without incurring significant losses. Examples of current investments include money market funds, high-yield savings accounts, and short-term certificates of deposit (CDs). The primary goal of holding current investments is to preserve capital and provide a safe haven for funds that may be needed in the near future. For instance, an individual might use their emergency fund as a current investment to ensure they have quick access to funds in case of unexpected expenses.

Short-Term Investments:

Short-term investments, on the other hand, are designed for a more extended period, often ranging from a few months to several years. These investments aim to provide a balance between capital appreciation and income generation over a more extended duration. Short-term investments can include stocks, bonds, mutual funds, and exchange-traded funds (ETFs) with a focus on active trading and capital gains. For example, an investor might purchase shares of a growth stock with the intention of holding it for a year or two, taking advantage of potential price appreciation and dividend income.

The key difference lies in the time horizon and the level of risk associated with each type of investment. Current investments are more liquid and less risky, making them suitable for risk-averse investors or those who need immediate access to their funds. Short-term investments, however, offer the potential for higher returns but may come with increased volatility and risk. Investors should carefully consider their financial goals, risk tolerance, and the time they can commit to holding investments when deciding between the two.

In summary, while "current investments" emphasize liquidity and short-term needs, "short-term investments" focus on a longer-term strategy with potential for growth. Understanding this distinction is essential for investors to create a well-rounded portfolio that aligns with their financial objectives and risk preferences.

Long-Term Investment Strategies: Navigating the Market's Future

You may want to see also

![]()

Risk Tolerance: How risk appetite influences investment choices

Risk tolerance is a critical concept in investing, as it determines an individual's or institution's willingness to accept uncertainty and potential losses in pursuit of higher returns. It is a measure of how much risk an investor is willing to take on, and it significantly influences the types of investment choices made. Understanding one's risk tolerance is essential for building a well-rounded investment portfolio that aligns with financial goals and objectives.

The level of risk tolerance varies among investors and can be influenced by several factors. Age is a significant determinant; younger investors often have a higher risk tolerance since they have more time to recover from potential losses. As individuals age, their risk tolerance typically decreases due to a growing need for stable, long-term returns to support retirement goals. Additionally, an investor's financial situation plays a role; those with substantial savings and a lower reliance on immediate income may be more inclined to take on higher risks.

Risk tolerance also depends on an individual's investment knowledge and experience. More experienced investors might be more comfortable with riskier investments as they have a better understanding of market dynamics and potential pitfalls. Conversely, beginners may opt for more conservative strategies to avoid significant losses while learning the ropes of investing.

When assessing risk tolerance, investors should consider their investment goals, time horizon, and financial obligations. For short-term goals, such as saving for a vacation or a down payment on a house, investors might be more willing to take on riskier investments. However, for long-term goals like retirement, a more conservative approach is often recommended to ensure capital preservation.

In practice, investors can use various tools to gauge their risk tolerance. One common method is the Risk Number, which is a personalized risk threshold based on an individual's financial profile and goals. This tool helps investors understand the level of risk they can afford to take without compromising their financial well-being. Additionally, investors can assess their risk tolerance by evaluating their emotional response to market fluctuations and their ability to stick to a long-term investment strategy.

In summary, risk tolerance is a key factor in investment decision-making, as it dictates the types of assets an investor is willing to hold. By understanding and managing risk tolerance, investors can build portfolios that align with their financial aspirations while minimizing potential drawbacks. It is a dynamic concept that evolves over time, requiring regular review and adjustment to ensure investments remain suitable for an individual's changing circumstances.

Maximize Your Short-Term Cash: Top Investment Strategies

You may want to see also

![]()

Liquidity: The ease of converting investments into cash

Liquidity is a critical aspect of investment management, especially when distinguishing between current and short-term investments. It refers to the ease and speed with which an investment can be converted into cash without significant loss of value. This concept is crucial for investors as it directly impacts their ability to access their funds when needed.

In the context of current investments, liquidity is a key differentiator. Current investments are typically those that can be quickly and easily converted into cash with minimal impact on their value. These investments are highly liquid and are often used to meet short-term financial obligations or take advantage of immediate opportunities. Examples of current investments include money market funds, treasury bills, and high-quality corporate bonds with short-term maturity dates. These assets are considered low-risk and provide a safe haven for investors seeking quick access to their capital.

Short-term investments, on the other hand, also aim for liquidity but may carry slightly higher risks. These investments are designed to be held for a brief period, often up to one year, and are intended to provide a balance between capital preservation and potential growth. Short-term investments can include certificates of deposit (CDs), savings accounts, and certain money market funds. While these options offer relatively low risk, they might not provide the same level of liquidity as current investments, especially for those requiring immediate access to funds.

The concept of liquidity is essential for investors to manage their risk exposure and ensure they can meet their financial obligations. Highly liquid investments provide a safety net, allowing investors to quickly respond to market changes or unexpected expenses. For instance, having a portion of one's portfolio in current investments can be a prudent strategy, especially during times of economic uncertainty, as it enables investors to maintain flexibility and access to cash.

In summary, liquidity is a vital consideration when evaluating investments, particularly when distinguishing between current and short-term investments. Current investments are characterized by their high liquidity, enabling investors to access their funds swiftly without significant loss of value. Understanding and prioritizing liquidity can help investors make informed decisions, ensuring they have the necessary financial flexibility to navigate various market conditions and personal financial needs.

Maximizing Profits: A Beginner's Guide to Short-Term Rental Investing

You may want to see also

![]()

Tax Implications: Tax considerations for long-term vs. short-term gains

When it comes to investments, understanding the tax implications is crucial for making informed financial decisions. The tax treatment of long-term and short-term gains can significantly impact your overall investment strategy and returns. Here's an overview of the tax considerations for each:

Long-Term Capital Gains:

Long-term capital gains are taxes levied on the profit realized from selling an asset held for an extended period, typically more than one year. The tax rate for long-term gains is generally lower than the ordinary income tax rate, offering a significant advantage to investors. This lower tax rate is designed to encourage long-term investment strategies and provide an incentive for investors to hold assets for the long haul. For example, in many countries, long-term capital gains are taxed at a rate of 0%, 15%, or 20%, depending on the investor's income level. This favorable tax treatment allows investors to benefit from the potential growth of their investments without incurring a heavy tax burden.

Short-Term Capital Gains:

In contrast, short-term capital gains are taxed at the ordinary income tax rate. These gains arise from the sale of assets held for a shorter period, usually one year or less. The tax rate for short-term gains is typically higher than the long-term rate, making it less advantageous for investors. Short-term trading strategies may be subject to higher tax rates, which can reduce the net gains from such activities. It's important to note that the classification of an investment as long-term or short-term can depend on the specific tax laws of your jurisdiction, so consulting local tax regulations is essential.

Tax Strategies:

Investors often employ various tax strategies to optimize their investment returns. One common approach is to hold investments for the long term to benefit from the reduced tax rate on capital gains. This strategy can be particularly effective for long-term growth-oriented investments, such as stocks or real estate. Additionally, tax-efficient investment accounts, like retirement accounts, may offer tax advantages, allowing investments to grow tax-deferred or tax-free. Understanding the tax implications can help investors make strategic decisions to minimize their tax liability and maximize their investment returns.

In summary, the tax treatment of long-term and short-term capital gains differs significantly, with long-term gains often taxed at a more favorable rate. This distinction encourages investors to adopt long-term investment strategies. By considering these tax implications, investors can make informed choices to optimize their financial goals and minimize unnecessary tax burdens.

Understanding Short-Term Investments: Are They Current Assets?

You may want to see also

![]()

Market Volatility: Impact of market fluctuations on investment strategies

Market volatility refers to the rapid and significant fluctuations in asset prices, which can have a profound impact on investment strategies. This volatility is often associated with increased uncertainty and risk, making it a critical factor for investors to consider when formulating their plans. Understanding the effects of market volatility is essential for investors to navigate the ever-changing financial landscape effectively.

During periods of high market volatility, investment strategies may need to adapt quickly. Volatile markets can lead to rapid price swings, causing assets to become more or less valuable in a short time. This dynamic environment demands that investors remain agile and responsive to changing conditions. For instance, a strategy that focuses on long-term buy-and-hold investments might need adjustments when markets become highly volatile. Investors may consider implementing strategies like diversification, where they spread their investments across various asset classes, to mitigate the risks associated with market fluctuations.

One common approach to dealing with market volatility is to adopt a short-term investment perspective. Short-term investments aim to capitalize on quick market movements and can involve strategies such as day trading or swing trading. These strategies require investors to make frequent decisions based on market trends and technical analysis. While short-term investments can be profitable during volatile periods, they also carry higher risks due to the increased uncertainty and potential for rapid price changes.

On the other hand, some investors prefer a long-term investment strategy, which involves holding assets for an extended period, often years or even decades. This approach leverages the historical trend of markets eventually recovering and growing over time. Long-term investors believe that short-term market fluctuations are less significant compared to the overall market performance over an extended period. They focus on fundamental analysis, studying a company's financial health and growth prospects, rather than short-term price movements.

In summary, market volatility significantly influences investment strategies, prompting investors to adapt their approaches. While some investors may opt for short-term strategies to capitalize on market fluctuations, others may prefer long-term investments, riding out the volatility. Finding the right balance between these strategies and considering individual risk tolerance and financial goals is crucial for successful navigation through volatile markets.

Maximizing Returns: Smart Short-Term Investment Strategies

You may want to see also

Frequently asked questions

Current investments typically refer to assets that are held for a short period, often less than a year, and are considered highly liquid. These investments are primarily used to meet short-term financial goals, such as emergency funds or upcoming expenses. Examples include money market accounts, certificates of deposit (CDs), and short-term government bonds. Short-term investments are a subset of current investments, focusing on assets that can be quickly converted into cash with minimal impact on their value.

Current investments are designed for liquidity and quick access to funds, making them suitable for short-term financial needs. They offer relatively low risk and stable returns, often with minimal price fluctuations. On the other hand, long-term investments are held for an extended period, usually several years or more. These investments often include stocks, bonds, real estate, or mutual funds, which are intended to grow in value over time and provide higher returns but may be less liquid and carry more risk.

Yes, tax considerations can vary between current and long-term investments. For current investments, any gains or interest earned may be subject to short-term capital gains tax, which is typically lower than long-term rates. These investments are often used for liquidity and are not intended to be held for an extended period. In contrast, long-term investments may be taxed at different rates, and some assets, like real estate, can offer tax advantages if held for a certain period. It's essential to understand the tax implications of each investment type to make informed financial decisions.