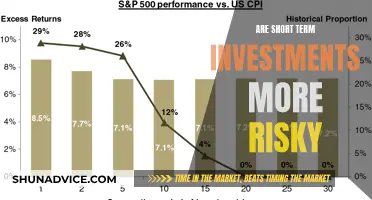

In the realm of long-term investing, understanding the impact of Risk Management and Development (RMD) strategies is crucial. RMDs play a pivotal role in shaping investment outcomes by influencing risk exposure, asset allocation, and overall portfolio performance. This paragraph delves into the intricate relationship between RMDs and long-term investing, exploring how these strategies can either enhance or hinder investment goals over extended periods. By examining various RMD approaches, investors can gain valuable insights into optimizing their portfolios and navigating the complexities of the financial markets with a long-term perspective.

What You'll Learn

- Market Volatility: RMDs can impact long-term investment strategies by causing market volatility

- Tax Implications: RMDs may have tax consequences, affecting long-term investment returns

- Asset Allocation: RMDs can influence asset allocation decisions in long-term investment portfolios

- Retirement Planning: RMDs can impact retirement planning and long-term financial goals

- Investment Timing: RMDs may require strategic investment timing to manage long-term wealth

![]()

Market Volatility: RMDs can impact long-term investment strategies by causing market volatility

Market volatility is an inherent risk in the financial markets, and it can significantly impact long-term investment strategies, especially when Regular Mandatory Distributions (RMDs) are involved. RMDs are required withdrawals from retirement accounts, typically set at a fixed percentage of the account balance, and they must be taken by the account owner or beneficiary each year, starting at age 72. While RMDs are designed to provide a steady income stream for retirees, they can inadvertently contribute to market volatility, particularly in long-term investments.

When RMDs are withdrawn from investment accounts, they often need to be liquidated to meet the cash requirement. This process can lead to selling assets, including stocks, bonds, or mutual funds, which may result in short-term capital gains or losses. These transactions can introduce volatility into the market, especially if the investments are sold at inopportune times, such as during market downturns. As a result, RMDs can create a feedback loop where market volatility triggers RMDs, which in turn exacerbate the volatility.

The impact of RMDs on market volatility is particularly relevant for long-term investors who aim to grow their wealth over an extended period. Long-term investors often focus on asset allocation and diversification to minimize risk. However, RMDs can disrupt this strategy by forcing liquidations that may not align with the investor's overall plan. For instance, selling assets to meet RMD requirements might lead to selling at a low point in the market, potentially locking in losses or missing out on future gains.

To mitigate the effects of market volatility caused by RMDs, investors can consider several strategies. One approach is to carefully time RMDs to coincide with periods of market stability or growth. This timing can help avoid selling during market downturns. Additionally, investors might explore alternative methods of generating income, such as annuitization or taking withdrawals from non-retirement accounts, to reduce the reliance on RMDs from long-term investment portfolios. Another strategy is to consult a financial advisor who can provide personalized guidance on managing RMDs and minimizing their impact on long-term investment goals.

In summary, RMDs can introduce market volatility, which is a critical consideration for long-term investors. By understanding the potential consequences and implementing appropriate strategies, investors can navigate the challenges posed by RMDs and maintain their long-term investment objectives. It is essential to stay informed about market trends and seek professional advice to ensure that RMDs do not derail a carefully constructed investment plan.

Unlocking the Long-Term Potential: Savings vs. Investments

You may want to see also

![]()

Tax Implications: RMDs may have tax consequences, affecting long-term investment returns

When it comes to long-term investing, understanding the impact of Required Minimum Distributions (RMDs) is crucial, especially regarding the tax implications. RMDs are a set of rules that dictate how much money an individual must withdraw from certain tax-deferred retirement accounts, such as traditional IRAs, each year after reaching a certain age. While RMDs ensure that retirement accounts are taxed, they can have significant effects on long-term investment strategies.

One of the primary tax implications of RMDs is the potential increase in taxable income. As RMDs are mandatory withdrawals, they can push an individual's income into higher tax brackets, especially for those with substantial retirement savings. This can result in a higher tax liability, which may reduce the net returns on long-term investments. For example, if an investor has a large IRA and takes the required RMD, the distribution could push their income over a certain threshold, leading to a higher tax rate on other sources of income. This effect can be particularly relevant for retirees who rely on their investment returns to sustain their lifestyle.

Additionally, RMDs can impact investment strategies, especially for those aiming to minimize taxes. Investors might need to adjust their portfolios to accommodate the mandatory withdrawals. This could involve selling assets to generate the required cash or rebalancing the portfolio to ensure sufficient liquidity. These actions can have tax consequences, such as capital gains taxes on asset sales, which may further reduce the overall investment returns. Proper planning and consideration of RMDs are essential to mitigate these potential tax implications.

To navigate these tax challenges, investors should consider various strategies. One approach is to take RMDs in a tax-efficient manner, such as by withdrawing assets with lower tax implications, like mutual funds or stocks, rather than cash. Another strategy is to utilize tax-loss harvesting, where investors sell investments at a loss to offset capital gains and reduce overall tax liability. Additionally, contributing to a Roth IRA can be beneficial, as withdrawals from Roth accounts are tax-free, providing a potential way to avoid RMD-related tax issues.

In summary, RMDs can significantly influence long-term investment outcomes, particularly through their tax implications. Understanding these effects is vital for investors to make informed decisions and develop strategies that align with their financial goals. By being proactive and implementing appropriate tax-saving techniques, individuals can better manage the impact of RMDs on their long-term investment returns.

Afs Investments: Long-Term Strategy or Short-Term Gamble?

You may want to see also

![]()

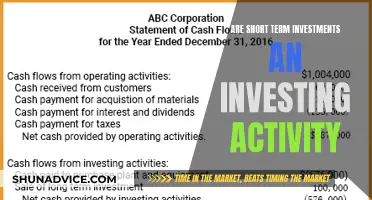

Asset Allocation: RMDs can influence asset allocation decisions in long-term investment portfolios

RMDs, or Required Minimum Distributions, are a significant consideration for long-term investors, particularly those approaching or in retirement. These distributions are mandated by the IRS and can have a substantial impact on an investor's asset allocation strategy. When an individual reaches a certain age, typically 72 or older, they are required to take out a minimum amount from their tax-deferred retirement accounts, such as IRAs or 401(k)s. This mandatory withdrawal can significantly alter the composition of an investor's portfolio, especially if they are in the accumulation phase of investing.

One of the primary effects of RMDs on asset allocation is the need to balance short-term liquidity with long-term growth potential. As investors are required to take out a fixed percentage of their account balance each year, they must carefully consider how to allocate these distributions to maintain their desired investment strategy. This often involves a shift in asset allocation, potentially moving more towards liquid assets like cash or fixed-income securities to ensure the ability to meet the RMD requirements.

For long-term investors, this can be a strategic opportunity to rebalance their portfolios. By taking advantage of the RMD requirement, investors can strategically sell assets that have appreciated in value and are now generating capital gains. This can be particularly useful for those looking to reallocate funds into more tax-efficient or growth-oriented investments. For example, an investor might use the proceeds from selling appreciated stocks to purchase index funds or exchange-traded funds (ETFs) that offer diversification and potentially lower tax implications.

Additionally, RMDs can encourage investors to review and adjust their asset allocation strategies. As the required distributions are based on the value of the account at the end of the previous year, any significant market fluctuations can impact the amount owed. This may prompt investors to reassess their asset allocation, ensuring that it aligns with their risk tolerance and financial goals. For instance, if a significant portion of the portfolio is in growth stocks and the market has experienced a downturn, an investor might consider reallocating some funds to more stable assets to meet the RMD requirement while also managing risk.

In summary, RMDs play a crucial role in shaping asset allocation decisions for long-term investors. By understanding the impact of these mandatory distributions, investors can strategically manage their portfolios, potentially optimizing tax efficiency and aligning asset allocation with their overall investment objectives. It is essential for investors to stay informed about their RMD obligations and regularly review their asset allocation strategies to navigate the complexities of long-term investing successfully.

Markatale Securities: Unraveling the Short-Term Investment Mystery

You may want to see also

![]()

Retirement Planning: RMDs can impact retirement planning and long-term financial goals

Retirement planning is a critical aspect of financial management, especially for those approaching their golden years. One of the key considerations for retirees and those planning for retirement is understanding the impact of Required Minimum Distributions (RMDs) on their long-term financial goals. RMDs are a mandatory withdrawal requirement for individuals with retirement accounts, such as traditional IRAs and 401(k)s, once they reach a certain age, typically 72. While RMDs ensure a steady income stream for retirees, they can significantly impact retirement planning and long-term financial strategies.

For retirees, RMDs can have both advantages and challenges. On the positive side, RMDs provide a guaranteed income stream, which is essential for covering living expenses during retirement. This regular distribution can help retirees maintain a consistent cash flow, ensuring they have the financial means to cover their daily needs. However, the mandatory nature of RMDs can also lead to several potential drawbacks. Firstly, RMDs may result in higher tax liabilities, as the withdrawals are often taxed as ordinary income. This can be particularly challenging for retirees on a fixed income, as they may need to allocate a larger portion of their RMD funds to cover taxes, leaving less for other expenses.

Additionally, RMDs can impact the growth and preservation of retirement savings. Retirees must carefully consider the timing and amount of withdrawals to ensure their long-term financial goals are not compromised. If not managed properly, RMDs can lead to excessive withdrawals, depleting retirement savings faster than expected. This is especially crucial for those aiming to maintain a specific lifestyle or achieve long-term financial milestones. To mitigate these risks, retirees should consider consulting a financial advisor who can help develop a personalized retirement plan, taking into account RMD requirements and tax strategies.

Furthermore, the impact of RMDs extends beyond individual retirees. For those who are still working and contributing to retirement accounts, RMDs can influence their investment strategies. As individuals approach the age of RMDs, they may need to adjust their investment approach to balance the need for income generation and the preservation of capital. This could involve rebalancing portfolios, considering tax-efficient investment options, or exploring alternative retirement income sources.

In summary, RMDs play a significant role in retirement planning and can either support or challenge an individual's long-term financial goals. Retirees must carefully navigate the mandatory withdrawal requirements, considering tax implications and the potential impact on their overall financial strategy. By understanding the effects of RMDs, retirees can make informed decisions to ensure a secure and comfortable retirement, aligning with their desired financial objectives.

Understanding Short-Term Investments: A Brainly Guide

You may want to see also

![]()

Investment Timing: RMDs may require strategic investment timing to manage long-term wealth

RMDs, or Required Minimum Distributions, are a critical aspect of retirement planning that can significantly impact long-term investment strategies. These distributions mandate that individuals with certain retirement accounts, such as traditional IRAs or 401(k)s, take a minimum amount of money out of their accounts each year, typically starting at age 72. While RMDs are designed to provide a steady income stream for retirees, they can also present challenges and opportunities for investors looking to preserve and grow their wealth over the long term.

One of the key considerations when dealing with RMDs is the potential impact on investment portfolios. RMDs often require retirees to liquidate a portion of their investments, which can be a strategic decision point for investors. By carefully planning the timing of RMDs, individuals can optimize their investment strategies. For example, investors might choose to take larger RMDs in years when their investment portfolio has performed well, allowing them to potentially sell assets at higher values. This approach can help minimize the tax impact of RMDs and potentially preserve more of the portfolio's gains.

Strategic investment timing becomes crucial when managing RMDs to ensure that retirees can maintain their desired lifestyle without depleting their savings prematurely. Here are some tactics to consider:

- Diversify and Rebalance: Investors should aim to diversify their portfolios across various asset classes, including stocks, bonds, and real estate. Regular rebalancing of the portfolio can help manage risk and ensure that investments align with long-term goals. By diversifying, retirees can better withstand market fluctuations and potentially avoid selling assets at inopportune times due to RMD requirements.

- Consider Tax-Efficient Strategies: RMDs are subject to income tax, so minimizing the tax impact is essential. Investors can explore tax-efficient investment strategies, such as tax-loss harvesting, where they sell investments that have decreased in value to offset capital gains. Additionally, contributing to tax-advantaged accounts, like Roth IRAs, can provide long-term tax benefits.

- Review and Adjust Annuity Options: Annuities can be a valuable tool for managing RMDs. Some annuities offer guaranteed income streams, allowing retirees to convert a portion of their portfolio into a steady cash flow. This can help individuals meet their immediate financial needs while preserving the remaining assets for future generations.

- Plan for RMDs in Advance: Proactive planning is essential. Investors should review their retirement accounts and investment portfolios regularly to anticipate future RMD requirements. By doing so, they can make informed decisions about asset allocation and potentially adjust their strategies to optimize tax efficiency and wealth preservation.

In summary, RMDs present a unique challenge for long-term investors, but with strategic timing and planning, retirees can effectively manage their distributions while preserving and growing their wealth. By understanding the impact of RMDs and implementing thoughtful investment strategies, individuals can navigate the complexities of retirement planning and ensure a more secure financial future.

Understanding NAV: The Key to Investment Clarity

You may want to see also

Frequently asked questions

RMDs are mandatory withdrawals from traditional IRAs (Individual Retirement Accounts) that individuals must take after reaching a certain age, typically 72. While RMDs can affect long-term investing by forcing liquidity, they also provide an opportunity to review and potentially optimize investment portfolios. By taking RMDs, investors can assess their financial situation, rebalance their portfolios, and make strategic adjustments to align with their long-term goals.

Yes, there are strategies to minimize the impact of RMDs on long-term capital preservation. One approach is to convert a portion of a traditional IRA to a Roth IRA, which allows for tax-free withdrawals in the future. By converting, you can avoid RMDs on the traditional IRA while potentially growing tax-free savings in the Roth IRA. Additionally, consulting a financial advisor can help develop a personalized plan to manage RMDs and ensure they align with your long-term investment objectives.

RMDs are subject to income tax, which can impact the after-tax returns of long-term investments. When RMDs are taken, the distributions are taxed as ordinary income, which may push investors into higher tax brackets. This can result in a higher tax burden, especially for those with significant retirement savings. It is essential to consider the tax implications and potentially adjust investment strategies to minimize the tax impact of RMDs on long-term growth.