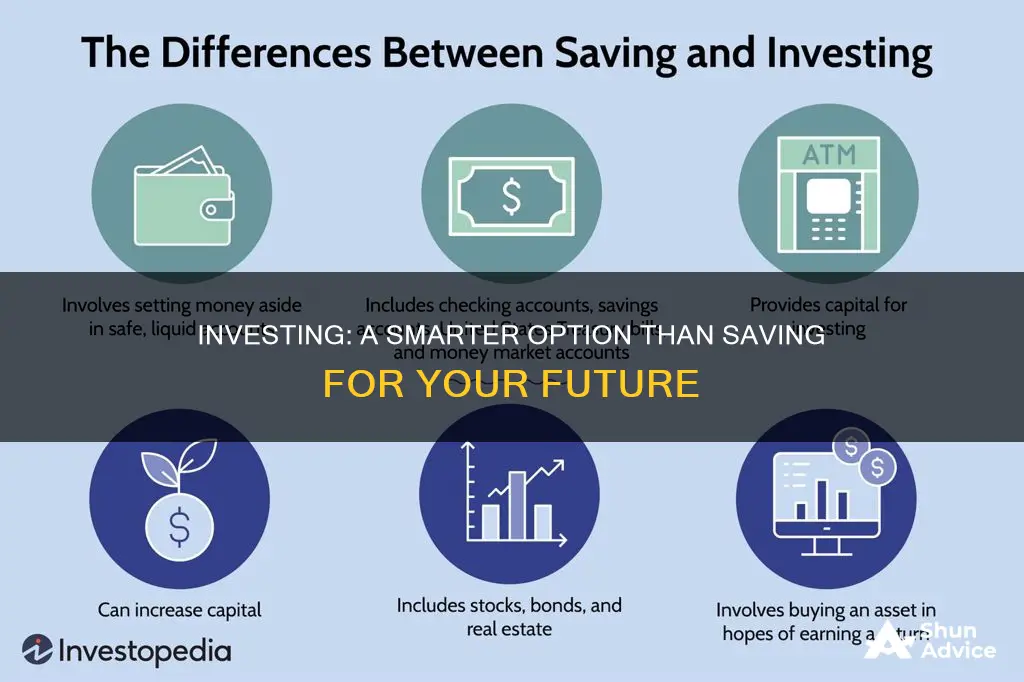

Saving and investing are both important for building a sound financial future, but they serve different purposes. Saving is generally better for short-term financial goals, such as building an emergency fund or saving for a vacation, as it provides a safe and low-risk way to accumulate money. On the other hand, investing is typically better for long-term goals, such as retirement or children's education, as it offers the potential for higher returns over time. While investing carries the risk of losing money, it can also lead to significant growth in wealth. Therefore, it is essential to understand the differences between saving and investing to make informed financial decisions.

| Characteristics | Values |

|---|---|

| Risk | Saving is low-risk, investing is higher-risk |

| Returns | Saving offers lower, more predictable returns; investing offers higher, fluctuating returns |

| Liquidity | Saving offers immediate access to funds; investing has barriers to access |

| Time horizon | Saving is better for short-term goals; investing is better for long-term goals |

| Inflation | Saving is susceptible to inflation; investing can help protect against inflation |

| Emergency funds | Saving is essential for emergency funds; investing is not recommended until emergency funds are in place |

| Financial goals | Saving is suitable for immediate or near-term expenses; investing is suitable for long-term goals such as retirement |

| Income | Saving is suitable for those with minimal cash savings; investing is suitable for those with excess cash |

What You'll Learn

![]()

Investing can help you beat inflation

Inflation is the increase in the price of goods and services over time, which erodes the purchasing power of your money. In other words, with inflation, you won't be able to buy as much in the future with the same amount of money. This is why it's important to find ways to make your money grow, and investing is one of the best ways to do that.

When you invest, you put your money into something with the expectation that it will grow in value over time. This can help you maintain or even increase your "buying power" as inflation drives up the prices of everyday items.

Historical Performance of the Stock Market

Historically, money invested in the stock market has grown significantly more over the long term than money kept in a savings account. Stocks offer the most upside potential in the long term, and some broad market indexes like the S&P 500 have generated average annual returns of around 11% over the past decade.

Beating Inflation with Specific Assets

Some assets have traditionally outperformed the rate of inflation and can be good choices for your investment portfolio. These include:

- Gold: Gold is often considered a hedge against inflation and has seen an average annual gain of 9.48% over a 20-year period. It is a physical asset that tends to hold its value, especially in countries where the native currency is losing value.

- Real Estate: Property prices and rental income tend to rise with inflation, making real estate a good hedge against inflation. This includes both direct property ownership and real estate investment trusts (REITs).

- Treasury Inflation-Protected Securities (TIPS): TIPS are designed to protect your investment from rising prices. The U.S. Treasury adjusts the par value of TIPS each year to keep up with inflation, boosting your interest payments.

- Diversified Index Funds: Experts recommend investing in diversified index funds based on broad market indexes like the S&P 500. This approach allows you to diversify your portfolio, grow your investments, and lower your risk of loss due to inflation.

Compounding Returns

Compounding returns, or reinvesting your returns to earn even more, can significantly boost your investment growth over time. The sooner you start investing and the longer you stay invested, the better, regardless of short-term market fluctuations.

Beating Inflation with Growth Stocks

In general, businesses that benefit from inflation are those that require little capital. Technology and communication services companies are good examples of this, as they are capital-light businesses. Therefore, investing in growth stocks or growth-stock mutual funds can be a good strategy to beat inflation.

While investing can be a powerful tool to beat inflation, it's important to remember that it comes with risks. The value of stocks and other investments can go up and down, and there is always the possibility of losing some or all of your investment. Diversification and long-term investing are key to reducing these risks.

Additionally, before investing, make sure you have enough savings in an emergency fund and enough money in your savings account to cover short-term needs and expenses.

Savings Strategies: Maximizing Output from Your Investments

You may want to see also

![]()

Investing is a good option for long-term goals

- Beating Inflation: One of the biggest drawbacks of saving is that it often fails to beat inflation. With inflation, the purchasing power of your money decreases over time. In contrast, investing in stocks, bonds, mutual funds, or real estate can offer returns that outpace inflation, helping you preserve and grow your wealth in real terms.

- Potential for Higher Returns: Investments typically offer the potential for higher returns compared to traditional savings accounts. By taking on a higher level of risk, you increase the opportunity for greater gains. Over the long term, the average annual growth of the stock market, for example, has historically been around 7% after inflation.

- Compounding Effects: Investing allows you to benefit from compounding returns. Compounding happens when your earnings start generating their own earnings, leading to exponential growth in your wealth over time. This effect is particularly pronounced when reinvesting dividends or interest income.

- Long-Term Goals: Investing is especially suitable for long-term goals such as retirement planning, saving for your children's education, or building generational wealth. The longer your investment horizon, the more time your investments have to ride out short-term market fluctuations and benefit from the power of compounding.

- Tax Benefits: Certain investment vehicles, such as retirement accounts (e.g., 401(k)s, IRAs), offer tax advantages. These accounts allow you to contribute pre-tax income, defer taxes on investment earnings, or benefit from tax-free growth, enhancing your overall returns.

- Income Generation: Investing can be a source of passive income through dividend-paying stocks, interest payments from bonds, or rental income from real estate investments. This additional income stream can supplement your regular earnings and further boost your savings.

- Diversification: Investing allows you to diversify your portfolio across various asset classes, industries, and companies, reducing overall risk. Diversification helps protect your portfolio from significant losses during market downturns and can provide a more stable foundation for long-term growth.

Saving and Investing: Your Path to Financial Freedom

You may want to see also

![]()

You can invest in a variety of assets

Investing is a way to grow your money by purchasing an asset that will hopefully appreciate in value or provide a regular income in the future. There are several types of assets that you can invest in, and the right choice depends on your financial goals, timeline, and risk tolerance. Here is a detailed overview of some of the most common investment assets:

Stocks

Stocks are the basic building blocks of investing. When you buy stocks, you own shares of a public company, and you can benefit from its growth and profits. Stocks can be classified into growth stocks, value stocks, dividend stocks, and blue-chip stocks. Growth stocks are companies with rapidly increasing revenues and earnings, while value stocks are shares of healthy companies that are currently undervalued. Dividend stocks are companies that provide steady dividend income, and blue-chip stocks are established companies with a strong track record, such as Apple or Microsoft. Stocks tend to have higher yields than bonds but also come with greater risks.

Bonds

Bonds are fixed-income securities issued by corporations or governments to raise money for projects. When you buy a bond, you lend money to the issuer, and they pay you interest. Once the bond reaches maturity, the issuer returns your original investment. Bonds are less risky than stocks but usually offer lower returns.

Cash Equivalents

When financial professionals refer to cash as an investment, they mean short-term, highly liquid investments like money market funds, treasury bills, and certificates of deposit (CDs). These investments provide stability to your portfolio and are suitable for short-term financial goals or retired investors who can't take on much risk.

Mutual Funds

Mutual funds are investment vehicles where multiple investors pool their money to purchase a diverse group of stocks, bonds, and other securities. Mutual funds are managed by professional money managers and are typically designed to track a market index like the S&P 500. There are also actively managed mutual funds that aim to outperform the market but often come with higher costs. Mutual funds provide diversification and lower risk compared to individual stocks.

Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds but trade throughout the day on stock exchanges. They can track market indices or focus on specific sectors, such as technology or energy. ETFs tend to have lower investment minimums than mutual funds, making them more accessible to new investors.

Annuities

Annuities are contracts between an individual and an insurance company. You pay the insurance company in installments or a lump sum, and they agree to make periodic payments to you for a set period, often used for a steady income stream in retirement. There are fixed, variable, and index annuities, each with different interest rate structures.

Derivatives

Derivatives are financial instruments whose value is based on an underlying asset. Common types of derivatives include futures contracts, options contracts, and swaps. Derivatives can be used for speculation or hedging against losses but are generally complex and risky, so they may not be suitable for all investors.

Cryptocurrency

Cryptocurrency, like Bitcoin or Ethereum, is a risky but buzz-worthy investment option. Cryptocurrencies are highly volatile and unregulated, so investing in them comes with significant risk. However, some people choose to invest in them due to their potential for high returns.

Real Estate

Real estate investing can be done by directly purchasing commercial or residential properties, or indirectly through real estate investment trusts (REITs), which trade like stocks. Real estate can be a good hedge against inflation and can benefit from a strong economy and low unemployment.

Hedge Funds and Private Equity Funds

Hedge funds and private equity funds are alternative investments typically only available to accredited investors with high net worth. These funds aim to deliver market-beating returns but can be volatile and may underperform the market. They often require substantial initial investments and have limited liquidity.

Commodities

Commodities are tangible investments, such as gold, silver, crude oil, or agricultural products. You can invest in commodities through commodity pools, managed futures funds, or specialized ETFs. Commodities can be a good hedge against inflation, as their value tends to rise during inflationary periods.

In conclusion, there are numerous investment assets to choose from, each with its own characteristics, risks, and potential returns. Diversifying your portfolio across a variety of these assets can help balance your risk and increase your potential for long-term wealth accumulation.

Life Cycle Theory: Savings and Investment Strategies Explored

You may want to see also

![]()

Investing can help you build wealth for your future

While saving is a great way to put money aside for short-term goals and emergencies, investing is a powerful tool to build wealth over time and achieve long-term financial goals. Here's how investing can help you build wealth for the future:

Higher Returns:

Investing offers the potential for higher returns compared to traditional savings accounts. Over time, investments in stocks, bonds, mutual funds, and other assets can provide much higher returns than the interest earned on savings accounts. This helps your wealth grow faster and enables you to achieve larger financial goals.

Beating Inflation:

Saving cash often results in negative returns after adjusting for inflation. Inflation erodes the purchasing power of your money over time. By investing, you have the opportunity to generate returns that outpace inflation, helping you maintain and grow your wealth in real terms.

Long-Term Goals:

Investing is ideal for long-term financial goals, such as retirement planning, saving for your children's education, or building generational wealth. The power of compounding returns over time can help your investments grow exponentially, turning smaller contributions into a substantial nest egg for the future.

Income Generation:

Investing in dividend-paying stocks, bonds, or real estate can provide a recurring income stream. This allows you to generate cash flow from your investments while also growing your principal investment over time.

Diversification:

Investing allows you to diversify your portfolio and reduce risk. By investing in a variety of assets, industries, and companies, you can lower the impact of market volatility and improve your overall returns.

Tax Benefits:

Certain investment accounts, such as retirement accounts (e.g., 401(k) or IRA) and 529 college savings plans, offer tax advantages. These accounts allow you to invest pre-tax dollars, defer taxes on investment earnings, or receive tax breaks, enhancing your overall returns.

Outpacing Debt:

Investing can be a more effective strategy than saving when it comes to managing high-interest debt. For example, if you have credit card debt with a 20% interest rate, investing your money at a potential return of 7% would result in a net loss. Paying off the high-interest debt first ensures you don't incur further interest expenses.

Building a Secure Future:

Investing allows you to build a secure financial future for yourself and your loved ones. It provides the opportunity to grow your wealth over time, ensuring you have sufficient funds for retirement, unexpected expenses, and major life goals.

Remember, investing does come with risks, and there is always the potential for losing money. It's important to carefully consider your financial situation, goals, and risk tolerance before investing. Additionally, maintaining a healthy balance between saving and investing is crucial, ensuring you have emergency funds readily available while also building wealth for the future.

Planning Savings and Investments: Strategies for Financial Freedom

You may want to see also

![]()

Investing can help you achieve financial security

- Inflation Protection: One of the biggest drawbacks of saving is that your money loses purchasing power over time due to inflation. In contrast, investing offers the potential for higher returns that can outpace inflation, helping you maintain the buying power of your money.

- Long-Term Goals: Investing is particularly well-suited for long-term financial goals, such as retirement planning, saving for a child's education, or building generational wealth. The power of compounding, where your earnings generate more earnings, can significantly boost your wealth over time.

- Diversification: Investing allows you to diversify your portfolio and reduce risk. By investing in a variety of assets, such as stocks, bonds, real estate, or mutual funds, you decrease the impact of any single investment loss.

- Higher Returns: On average, the stock market has historically provided annual growth of around 7% after inflation. This means that, over time, your investments can double in value roughly every 10 years. This is a much higher return than you would typically get from a savings account.

- Tax Benefits: Certain investment accounts, such as retirement accounts (e.g., 401(k) or IRA) and 529 college savings plans, offer tax advantages. These accounts allow you to either defer taxes on investment earnings or exempt them from certain taxes, enhancing your overall returns.

- Income Generation: Investing can provide a recurring income stream through dividend-paying stocks, bonds, or real estate investments. This can be particularly beneficial during retirement or if you're looking for passive income sources.

- Beating Savings Account Returns: The interest rates offered by savings accounts are often very low and may not even keep up with inflation. By investing, you have the potential to earn much higher returns than what you would get by keeping your money in a savings account.

While investing offers these advantages, it's important to remember that it also comes with risks. You could lose money, and there are no guarantees of positive returns. Therefore, it's crucial to assess your financial situation, goals, and risk tolerance before deciding whether to save or invest.

How Interest Rates Affect Savings and Investments

You may want to see also

Frequently asked questions

Saving is for low-risk, short-term financial goals, while investing is for long-term goals and comes with the risk of loss but also the potential for higher returns.

When you invest, you could lose money, break even, or earn a return—there are no guarantees. The value of your investments can fluctuate due to factors outside your control.

Saving provides a financial safety net for unexpected events and short-term goals. It is also a good option if you need immediate or near-term access to your money.

Investing has the potential for higher returns than savings and can help you achieve long-term financial goals. It is a good option if you are looking to grow your wealth over time.

Saving should be prioritized if you don't have an emergency fund or if you need the cash within the next few years. Investing is a better option if you have long-term financial goals and can keep your money invested for at least five years.