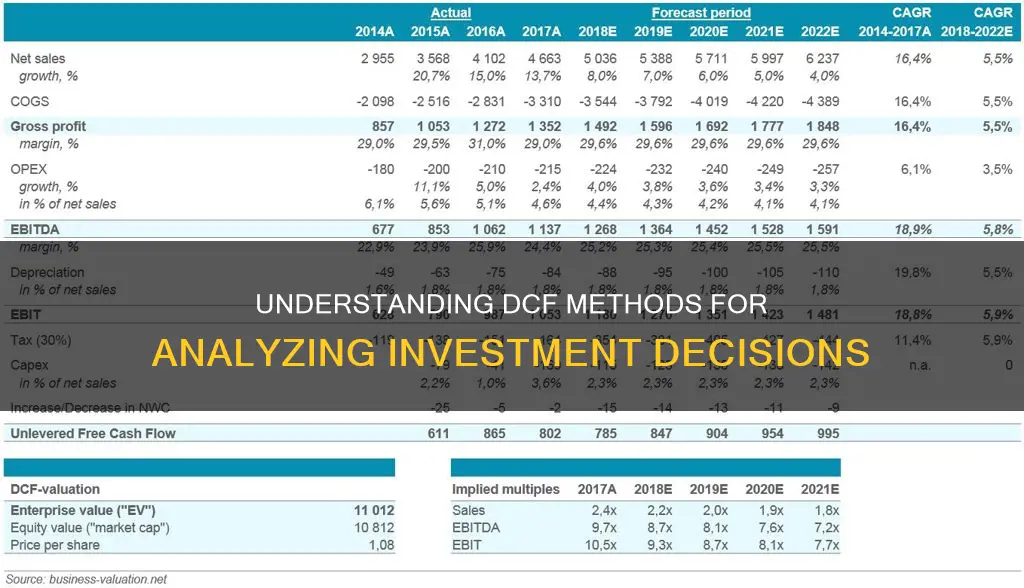

Discounted cash flow (DCF) is a valuation method that estimates the value of an investment using its expected future cash flows. Analysts use DCF to determine whether an investment is worthwhile by comparing its current cost to the potential future value of the investment. This is done by calculating the present value of expected future cash flows using a projected discount rate. If the DCF is higher than the current cost of the investment, the opportunity is likely to result in positive returns and may be worth pursuing.

| Characteristics | Values |

|---|---|

| Purpose | To determine whether an investment is worthwhile |

| Application | Used in investment banking, real estate, private equity, and corporate finance |

| Type of Model | Financial |

| Basis | The value of a company is determined by its ability to generate cash flows for investors in the future |

| Formula | DCF = CF1 / (1 + r) ^ 1 + CF2 / (1 + r) ^ 2 + ... CFn / (1 + r) ^ n |

| Components | Cash Flow, Discount Rate, Number of Periods |

| Discount Rate | Typically the company's Weighted Average Cost of Capital (WACC) |

| Time Period | Usually 10 years, but can vary |

| Use Cases | To value a business, project, investment, shares, or an income-producing property |

What You'll Learn

- DCF analysis can be used to determine whether to acquire a company or buy securities

- DCF analysis can help business owners and managers make capital budgeting decisions

- DCF analysis can be used to estimate the money an investor might receive from an investment

- DCF analysis can be used to determine the value of an investment based on its future cash flows

- DCF analysis can be used to determine whether an investment is worthwhile in the long run

![]()

DCF analysis can be used to determine whether to acquire a company or buy securities

Discounted cash flow (DCF) analysis can be used to determine whether to acquire a company or buy securities. DCF is a valuation method that estimates the value of an investment based on its expected future cash flows. It can be applied to value a stock, company, project, or other assets.

DCF analysis can help investors decide whether to acquire a company or buy securities by providing a reasonable projection of whether a proposed investment is worthwhile. It involves estimating the future cash flows of an investment and discounting them to their present value using a discount rate. The discount rate is typically the weighted average cost of capital (WACC), which accounts for the rate of return expected by shareholders.

If the DCF is higher than the current cost of the investment, the opportunity could result in positive returns and may be worthwhile. For example, if an investment has a DCF of $13,306,727 and an initial investment of $11 million, the net present value (NPV) is $2,306,727, indicating a potential positive return on investment.

DCF analysis can also be used to value privately held companies and as an additional test for publicly traded stocks. It is considered a more theoretical approach that relies on the fundamental expectations of the business rather than public market factors or historical precedents.

How Cashing Investments Affect Debt Service Coverage

You may want to see also

![]()

DCF analysis can help business owners and managers make capital budgeting decisions

Discounted cash flow (DCF) analysis is a valuable tool for business owners and managers when making capital budgeting decisions. DCF analysis is a method used to value investments by estimating future cash flows and discounting them to present value. This analysis helps determine whether an investment is worthwhile by assessing if the future cash flows generated will be greater than the initial investment.

For business owners and managers, DCF analysis provides a framework to evaluate potential investments, projects, or capital expenditures. By forecasting future cash inflows and outflows and applying a discount rate, businesses can identify projects that will create value and improve their capital allocation decisions. This analysis is particularly useful for long-term investments, such as new equipment purchases or expansion initiatives, as it considers the time value of money.

DCF analysis can also assist in budgeting decisions by evaluating the impact of different initiatives on cash flow. For example, a business owner could use DCF analysis to assess the benefits of a cost-saving program or entering a new market. By quantifying the expected cash flows and discounting them to the present value, business owners can make more informed decisions about resource allocation and strategic initiatives.

Additionally, DCF analysis can help business owners determine the projected value of their company. This information can be valuable when seeking external investment, applying for loans, or making strategic decisions about the company's future direction.

It is important to note that DCF analysis relies on estimates and assumptions about future cash flows, discount rates, and terminal values. As a result, it is essential to use conservative estimates and perform sensitivity analysis to account for potential variations in these factors.

Overall, DCF analysis is a powerful tool for business owners and managers, providing a quantitative framework to evaluate investments, projects, and strategic initiatives, ultimately improving capital budgeting decisions and driving long-term success.

Understanding the Relationship Between Cash and Investments

You may want to see also

![]()

DCF analysis can be used to estimate the money an investor might receive from an investment

Discounted cash flow (DCF) analysis is a method used to estimate the value of an investment based on its expected future cash flows. It is a useful tool for investors to determine whether an investment is likely to be profitable.

DCF analysis involves projecting the future cash flows of an investment and then discounting those cash flows to arrive at an estimated current value, known as the net present value (NPV). The discount rate used in this calculation is typically the weighted average cost of capital (WACC), which takes into account the cost of debt and equity used to finance the investment.

By comparing the DCF to the initial investment cost, investors can determine if the investment is likely to generate positive returns. If the DCF is higher than the current cost of the investment, the opportunity is likely to be profitable and worthwhile. On the other hand, if the DCF is lower than the present cost, investors may be better off holding onto their cash.

DCF analysis can be applied to a wide range of investments, including stocks, companies, projects, and other assets. It is particularly useful for investments with expected future cash flows that can be reasonably estimated. However, it is important to note that DCF analysis relies on estimates and assumptions, which may not always be accurate. As such, it should not be the sole method used for investment decisions.

Overall, DCF analysis is a valuable tool for investors to estimate the potential returns of an investment and make more informed decisions. By considering the expected future cash flows and discounting them to their present value, investors can assess whether an investment aligns with their financial goals and risk tolerance.

Investing in Cash Balance Plans: Understanding Your Options

You may want to see also

![]()

DCF analysis can be used to determine the value of an investment based on its future cash flows

Discounted cash flow (DCF) analysis is a method used to determine the value of an investment by projecting its future cash flows and discounting them to their present value. This analysis is based on the principle that the value of an investment is tied to its ability to generate cash flows for investors in the future.

DCF analysis involves forecasting the expected cash flows from an investment and then discounting them using an appropriate discount rate, which is typically the weighted average cost of capital (WACC). The WACC reflects the average rate of return expected by shareholders. By discounting future cash flows, DCF analysis accounts for the time value of money, which assumes that money in the future is worth less than money today due to factors such as uncertainty, inflation, and the potential to invest and earn interest.

The DCF formula is as follows:

DCF = CF1 / (1 + r)1 + CF2 / (1 + r)2 + ... + CFn / (1 + r)n

Where:

- CF1, CF2, ..., CFn = Cash flow for each period

- R = Discount rate

- N = Number of periods

By applying this formula, investors can determine the present value of the expected future cash flows. If the DCF is higher than the current cost of the investment, it indicates a potentially profitable opportunity with positive returns.

DCF analysis can be applied to value stocks, companies, projects, and other assets or activities. It is widely used in investment banking, corporate finance management, real estate, and private equity. It helps investors analyse potential mergers or acquisitions, and it assists business owners in making capital budgeting and operating expenditure decisions.

Cash App Investing: Dividends and Your Money

You may want to see also

![]()

DCF analysis can be used to determine whether an investment is worthwhile in the long run

Discounted Cash Flow (DCF) analysis is a valuable tool for investors and companies to determine whether an investment is worthwhile in the long run. It is a forward-looking analysis method that values an investment by estimating its future cash flows and discounting them to their present value. The DCF analysis is based on the principle that the value of an investment is tied to its ability to generate cash flows for investors in the future.

DCF analysis involves forecasting the expected cash flows from an investment and then discounting those cash flows to their present value using a discount rate. The discount rate reflects the cost of financing the investment or the opportunity cost of alternative investments. The higher the discount rate, the lower the present value of the future cash flows.

By comparing the DCF to the initial investment cost, investors can determine if the investment is profitable. If the DCF is greater than the present cost, the investment is likely to generate a positive return and is worth considering. On the other hand, if the DCF is lower than the present cost, it may be better to hold onto the cash.

DCF analysis can be applied to a wide range of investments, including stocks, companies, projects, real estate, and private equity. It is a valuable tool for financial analysts in investment banking, who use it to assess potential mergers and acquisitions. Outside of corporate finance, DCF valuations can assist business owners in making budget decisions and projecting the value of their companies.

However, it is important to note that DCF analysis relies on estimates and assumptions about future cash flows, discount rates, and terminal values. These estimates may not always be accurate, and small variations in early estimates can be magnified in future projections. As such, it is crucial to use DCF analysis in conjunction with other valuation approaches, such as comparable company analysis and price-to-earnings ratios.

Cash is Not King: Exploring Investment Alternatives

You may want to see also

Frequently asked questions

DCF analysis is based on the concept of "time value of money", which states that money in the future is worth less than money today. This is because of uncertainty, inflation, and the potential to invest and earn interest.

DCF analysis uses the formula: DCF = CF1 / (1 + r)1 + CF2 / (1 + r)2 + ... CFn / (1 + r)n, where CF is the cash flow for each year and r is the discount rate. This calculates the present value of expected future cash flows.

The discount rate is typically the company's Weighted Average Cost of Capital (WACC), which takes into account the company's interest rate, loan payments, and dividend payments to shareholders.

An investment is considered profitable when the DCF is higher than the initial cost. This indicates that the future cash flows of the investment are greater than the value of the initial investment.

DCF analysis relies on estimates of future cash flows, which may not be accurate. It is also sensitive to the estimation of the discount rate and terminal value. DCF may not be suitable for banks and financial institutions, as they reinvest positive cash flows into creating products.