Understanding the difference between short-term and long-term investments is crucial for anyone looking to grow their wealth. Short-term investments are typically those that you plan to hold for a relatively short period, often less than a year. These can include money market funds, certificates of deposit (CDs), and short-term bonds. They are generally considered low-risk and are used to preserve capital and provide easy access to funds. On the other hand, long-term investments are designed to be held for an extended period, often several years or more. These may include stocks, real estate, mutual funds, and retirement accounts like a 401(k) or IRA. Long-term investments are generally more volatile but offer the potential for higher returns over time, making them suitable for those who can afford to take on more risk in pursuit of greater gains.

What You'll Learn

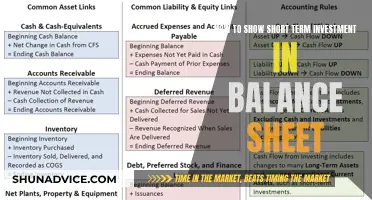

- Definition: Short-term investments are assets held for a year or less, while long-term investments are for more than a year

- Risk: Short-term investments often carry lower risk, while long-term investments may involve higher risk but potentially greater rewards

- Liquidity: Short-term investments are easily convertible to cash, whereas long-term investments may be less liquid

- Tax Implications: Short-term capital gains are taxed at a higher rate than long-term gains, impacting investment strategies

- Strategy: Investors use short-term investments for quick access to funds, while long-term investments are for wealth accumulation

![]()

Definition: Short-term investments are assets held for a year or less, while long-term investments are for more than a year

When discussing investments, it's essential to understand the distinction between short-term and long-term investments, as this classification significantly impacts financial strategies and risk management. Short-term investments are financial assets that are typically held for a relatively brief period, often a year or less. These investments are characterized by their liquidity and the ability to quickly convert them into cash without incurring significant losses. Examples of short-term investments include money market accounts, certificates of deposit (CDs) with maturities under a year, and highly liquid stocks or mutual funds that can be sold promptly. The primary goal of short-term investments is to provide a safe and accessible store of value while also offering a modest return on investment.

In contrast, long-term investments are those that are intended to be held for an extended period, typically more than a year. These investments are often chosen for their potential to generate substantial returns over time, as they may be subject to market fluctuations in the short term. Long-term investments include stocks, bonds, real estate, and certain types of mutual funds or exchange-traded funds (ETFs) that are designed for long-term growth. The strategy behind long-term investments is to weather short-term market volatility and benefit from the power of compounding, where returns are reinvested to earn additional returns over an extended period.

The key difference lies in the time horizon and the associated risks. Short-term investments are more conservative, offering lower potential returns but with reduced risk due to their liquidity and shorter exposure to market volatility. On the other hand, long-term investments are more aggressive, aiming for higher returns over an extended period, which may involve higher risks, especially in volatile markets. Investors often use a combination of both strategies to balance risk and return, ensuring their portfolios are well-diversified and aligned with their financial goals.

Understanding this distinction is crucial for investors to make informed decisions about their portfolios. It allows individuals to tailor their investment strategies to their risk tolerance, financial objectives, and time constraints. For instance, a young investor saving for retirement might opt for a higher proportion of long-term investments to maximize growth, while a more conservative investor approaching retirement might prefer a mix of short-term and long-term investments to ensure a steady income and principal preservation.

In summary, short-term investments are those held for a year or less, focusing on liquidity and modest returns, while long-term investments are for more than a year, aiming for substantial growth over time. This classification is fundamental in financial planning, helping investors navigate the complexities of the investment landscape and make choices that align with their unique circumstances and goals.

Understanding the Nature of Long-Term Investments: Operating Assets or Not?

You may want to see also

![]()

Risk: Short-term investments often carry lower risk, while long-term investments may involve higher risk but potentially greater rewards

When considering the risk associated with short-term and long-term investments, it's important to understand the inherent nature of each type of investment strategy. Short-term investments are typically characterized by their relatively low-risk profile. These investments are designed to be liquid and easily convertible into cash within a short period, usually a few days to a few months. Examples of short-term investments include money market funds, high-yield savings accounts, and short-term certificates of deposit (CDs). The primary appeal of short-term investments is their safety and accessibility, making them suitable for individuals seeking a safe haven for their funds while still allowing for quick access to their money when needed.

In contrast, long-term investments often come with a higher degree of risk but also carry the potential for greater rewards. These investments are typically held for an extended period, ranging from several years to decades. Stocks, bonds, real estate, and certain mutual funds are common examples of long-term investments. The risk associated with long-term investments is primarily due to market volatility and the uncertainty of future economic conditions. Over the long term, markets have historically trended upwards, but individual stocks and sectors can experience significant fluctuations, leading to potential losses.

The key difference in risk lies in the time horizon and the nature of the investment. Short-term investments are designed to provide liquidity and capital preservation, making them less susceptible to market downturns in the short term. On the other hand, long-term investments are more exposed to market cycles and economic shifts, which can result in substantial gains or losses over an extended period. Diversification is a critical strategy to manage risk in long-term investments, as it helps spread the potential impact of any single investment's performance.

For risk-averse investors, short-term investments offer a more conservative approach, ensuring that capital is protected while still providing a reasonable return. Long-term investors, however, are willing to take on more risk in exchange for the potential to build substantial wealth over time. It's essential for investors to assess their risk tolerance, financial goals, and investment time horizon to determine the most suitable investment strategy for their needs.

In summary, short-term investments are generally less risky due to their liquidity and focus on capital preservation, while long-term investments carry higher risk but offer the potential for significant returns. Understanding the risk associated with each investment type is crucial for making informed financial decisions and building a well-diversified investment portfolio.

Understanding Short-Term Investments: A Comprehensive Guide to H-10 Strategies

You may want to see also

![]()

Liquidity: Short-term investments are easily convertible to cash, whereas long-term investments may be less liquid

Liquidity is a crucial concept when understanding the difference between short-term and long-term investments. It refers to the ease with which an investment can be converted into cash without significant loss of value. In the context of investments, liquidity is a measure of how quickly and efficiently an asset can be bought or sold in the market without affecting its price.

Short-term investments are designed to be highly liquid, allowing investors to access their funds quickly and efficiently. These investments typically have a maturity period of less than one year and are easily convertible into cash. For example, money market funds, certificates of deposit (CDs), and treasury bills are considered short-term investments because they can be redeemed or sold relatively quickly, providing investors with immediate access to their capital. This liquidity is essential for investors who need to maintain a certain level of cash flow or who may require their funds for short-term financial needs.

On the other hand, long-term investments often exhibit lower liquidity. These investments are typically held for extended periods, sometimes even decades, and may take longer to sell or convert into cash. Real estate, for instance, is a long-term investment as it can take time to find a buyer willing to purchase the property at a fair price. Similarly, certain stocks or bonds with longer maturity dates may be less liquid, as they require a longer time horizon to find a suitable buyer. This reduced liquidity can be a trade-off for investors seeking higher potential returns over an extended period.

The concept of liquidity is essential for investors to consider when making financial decisions. It allows investors to assess the accessibility and flexibility of their investments. Short-term investments provide liquidity, ensuring investors can quickly access their funds when needed, while long-term investments may offer higher returns but with the trade-off of reduced liquidity. Understanding liquidity helps investors manage their risk and make informed choices based on their financial goals and time horizons.

In summary, liquidity is a key factor in distinguishing between short-term and long-term investments. Short-term investments are easily convertible to cash, providing quick access to funds, while long-term investments may take longer to liquidate and are often less liquid. This distinction is vital for investors to consider when evaluating their investment options and managing their financial portfolios.

Long-Term Investments: Separating Fact from Fiction

You may want to see also

![]()

Tax Implications: Short-term capital gains are taxed at a higher rate than long-term gains, impacting investment strategies

Understanding the tax implications of short-term and long-term investments is crucial for investors as it significantly influences their financial decisions and overall investment strategies. When it comes to capital gains, the duration of the investment plays a pivotal role in determining the tax rate applied. Short-term capital gains, which are profits realized from the sale of assets held for a short period, typically one year or less, are generally taxed at a higher rate compared to long-term gains. This tax differential is an essential consideration for investors, as it can impact their overall returns and the attractiveness of different investment options.

In many jurisdictions, short-term capital gains are often taxed at the investor's ordinary income tax rate. This means that the tax rate applied to these gains can be significantly higher than the rates for long-term capital gains. For instance, in the United States, short-term capital gains are taxed at the investor's regular income tax rate, which can vary depending on the investor's income level. This higher tax rate can be a strong incentive for investors to hold investments for the long term, as it may result in a more favorable tax treatment.

On the other hand, long-term capital gains, which are profits from assets held for more than a year, are usually taxed at a lower rate. This reduced tax rate is designed to encourage long-term investment strategies. Investors who adopt a long-term perspective often benefit from this tax advantage, as it allows them to keep a larger portion of their gains after taxes. As a result, long-term investors may be more inclined to reinvest their profits or use them to fund their retirement or other financial goals.

The tax implications of short-term versus long-term investments can significantly impact an investor's strategy. For instance, investors who frequently buy and sell assets for short periods may face higher tax burdens, potentially reducing their overall gains. In contrast, those who adopt a long-term approach, holding investments for years, can benefit from the lower tax rates on long-term capital gains. This tax differential encourages investors to consider the time horizon of their investments and the potential tax consequences when making trading decisions.

In summary, the tax treatment of short-term and long-term capital gains is a critical aspect of investment planning. Short-term gains are often taxed at a higher rate, which may prompt investors to reconsider their holding periods. Long-term gains, with their lower tax rates, provide an incentive for investors to adopt a more patient approach. Understanding these tax implications is essential for making informed investment choices and optimizing the tax efficiency of an investment portfolio.

Unlocking the Secrets: How Long is Long-Term Investing?

You may want to see also

![]()

Strategy: Investors use short-term investments for quick access to funds, while long-term investments are for wealth accumulation

Understanding the distinction between short-term and long-term investments is crucial for investors aiming to optimize their financial strategies. Short-term investments are typically characterized by their liquidity and relatively low-risk nature, making them an attractive option for investors seeking quick access to their funds. These investments are often used as a means to bridge gaps in cash flow, cover unexpected expenses, or take advantage of short-term market opportunities. Examples of short-term investments include money market funds, certificates of deposit (CDs), and high-yield savings accounts. These assets offer relatively stable returns with minimal risk, ensuring that investors can quickly convert their investments back into cash without significant loss.

On the other hand, long-term investments are designed with the primary goal of wealth accumulation over an extended period. This strategy involves a higher level of risk but also the potential for substantial returns. Long-term investors often focus on building a diversified portfolio of assets, such as stocks, bonds, mutual funds, or real estate, which are held for several years or even decades. The idea is to ride out short-term market fluctuations and benefit from the long-term growth potential of these investments. By investing for the long haul, individuals can take advantage of compound interest, allowing their wealth to grow exponentially over time.

The key difference lies in the time horizon and risk tolerance. Short-term investments cater to those who need immediate access to funds and are willing to accept lower returns for liquidity. In contrast, long-term investments are suitable for investors with a higher risk tolerance who are committed to a longer-term financial strategy. Diversification is a critical aspect of long-term investing, as it helps mitigate risk by spreading investments across various asset classes and sectors.

In practice, a strategic approach often involves a combination of both short-term and long-term investments. For instance, an investor might use short-term investments to maintain an emergency fund, providing a safety net for unexpected expenses. Simultaneously, they could allocate a larger portion of their portfolio to long-term investments, aiming for substantial wealth accumulation over time. This balanced approach allows investors to manage their cash flow effectively while also working towards their long-term financial goals.

In summary, short-term investments provide liquidity and quick access to funds, making them ideal for short-term financial needs and opportunities. In contrast, long-term investments are geared towards wealth creation, offering higher potential returns over an extended period. A well-rounded investment strategy often incorporates both approaches, ensuring investors can meet their immediate financial requirements while also building a robust financial future.

Quantitative Strategies: Unlocking Long-Term Investment Potential

You may want to see also

Frequently asked questions

Short-term investments are assets that are expected to be converted into cash or sold within a short period, typically one year or less. These investments are often used to meet immediate financial goals, such as covering daily expenses, emergency funds, or short-term savings. Examples include money market accounts, certificates of deposit (CDs), and short-term government bonds. On the other hand, long-term investments are those held for an extended period, usually with a time horizon of more than a year. They are often aimed at growing wealth over the long term and may include stocks, real estate, mutual funds, and retirement accounts.

Short-term investments are crucial for liquidity and accessibility, providing a safety net for unexpected expenses or short-term financial goals. They offer a more conservative approach, ensuring your capital is readily available. Long-term investments, however, are designed for wealth accumulation and growth. By investing in long-term assets, you can benefit from compound interest, allowing your money to grow exponentially over time. This strategy is essential for retirement planning, education funds, or any financial goal that requires significant growth over an extended period.

Yes, there are tax considerations for both types of investments. Short-term capital gains, which are profits from the sale of assets held for less than a year, are typically taxed at your ordinary income tax rate. Long-term capital gains, from assets held for more than a year, often qualify for a lower tax rate, which varies depending on your income level. Additionally, certain tax-advantaged accounts, like traditional IRAs or 401(k)s, offer tax benefits for long-term investments, allowing your money to grow tax-deferred or tax-free until withdrawal. It's essential to understand these tax implications to make informed investment decisions.