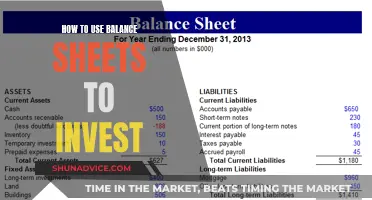

A company's financial health can be assessed by looking at its cash flow, or the movement of money in and out of the business. Positive cash flow indicates that a company's liquid assets are increasing, enabling it to cover obligations, reinvest in its business, and return money to shareholders. Conversely, negative cash flow indicates that a company's liquid assets are decreasing, which may be a cause for concern. However, negative cash flow is not always a warning sign, as it could be due to significant investments in the company's long-term health, such as research and development.

One way to assess cash flow is through a cash flow statement, which is a standard financial statement that shows a company's sources and use of cash over a specified period. There are three sections on the cash flow statement: cash flow from operating activities, cash flow from investing activities, and cash flow from financing activities.

This topic will specifically focus on the percentage of cash flows invested in repairing local licenses, which falls under the cash flow from investing activities section. This section includes any sources and uses of cash from a company's investments, such as purchases or sales of assets.

What You'll Learn

![]()

Local license repairs as a capital expenditure

Local license repairs can be classified as capital expenditures, depending on the nature of the repairs.

A capital expenditure is an amount paid to acquire, produce, or improve tangible real and personal property. It is considered a long-term investment in the company's operations and is typically depreciated over several years. On the other hand, a repair expense is a one-time cost incurred to maintain the property in proper working condition.

To determine whether local license repairs are capital expenditures or repair expenses, it is essential to consider the extent and nature of the repairs. If the repairs involve fixing a defect or design flaw, creating an addition or expansion, increasing capacity or efficiency, rebuilding property, or replacing major components, they would likely be classified as capital expenditures.

For example, if the local license repairs involve replacing a significant portion of the license, such as 30% or more, it would be considered a capital improvement. This is because it increases the value of the property and extends its useful life.

However, if the repairs are minor and only involve maintaining the current value of the property, they would likely be classified as regular repair and maintenance expenses. These are expenses necessary for managing and maintaining the business and can be deducted in the same year.

It is important to note that the classification of expenses as capital expenditures or repair expenses has significant tax implications. Capital expenditures are depreciated over several years, while repair expenses can be deducted in full in the current year. Therefore, it is crucial to understand the specific guidelines provided by tax authorities, such as the IRS in the United States, to make the correct classification and comply with tax regulations.

Investing: How Cash Flow Affects Your Bottom Line

You may want to see also

![]()

Repairs as a cash outflow

Repairs are a crucial aspect of maintaining and enhancing the value of a property asset. They can range from minor fixes to major renovations, and understanding how they impact cash flow is essential for effective financial management.

When considering repairs as a cash outflow, it's important to distinguish between routine and emergency repairs. Routine repairs are planned and budgeted for in advance. These may include painting, fixing broken fixtures, or addressing minor issues that arise over time. On the other hand, emergency repairs are unexpected and often involve significant costs. Examples include a burst pipe, roof damage due to a storm, or structural issues that need immediate attention.

The impact of repairs on cash flow can be significant, especially for real estate investors. When purchasing a property, it's common to allocate a certain percentage of the total cash invested for future repairs. This is often referred to as a "repair reserve" and can vary depending on the property's age, condition, and location. For instance, an older property may require a larger repair reserve to address potential issues with outdated systems or structural problems.

Let's consider an example to illustrate the impact of repairs on cash flow. Suppose an investor purchases a property for $250,000 and expects annual cash flow of $25,000. If repairs costing $50,000 are required in the first year, the cash flow will be impacted as follows:

- Annual cash flow: $25,000

- Repair costs: -$50,000

- Net cash flow: $20,000

In this case, the repair costs have reduced the net cash flow to $20,000, which is a significant difference from the expected cash flow of $25,000. It's important to note that repair costs can vary greatly depending on the specific situation and may include labour, materials, and other related expenses.

To manage cash outflow due to repairs effectively, it's advisable to build a contingency fund or budget for unexpected expenses. This ensures that funds are available when repairs are needed and helps to reduce the impact on cash flow. Additionally, regular maintenance and proactive property management can help identify potential issues early on, reducing the likelihood of costly emergency repairs.

Land Cash Purchase: An Investment Activity?

You may want to see also

![]()

Repairs as a non-cash item

Repairs and maintenance expenses are a common example of non-cash items. When a company incurs costs for repairing equipment, vehicles, or other assets, these expenses are recorded in the income statement as deductions. This reduces the reported net profit for the period. However, no cash flow is involved in these transactions because the repairs may be conducted using existing resources or through an exchange of assets without a direct cash payment.

For example, consider a company that owns a fleet of delivery trucks. Over time, these trucks may require maintenance and repairs to keep them in good working condition. The company may choose to perform these repairs in-house using their own mechanics and spare parts, or they may exchange services with another business that specialises in vehicle repairs. In both cases, there is no direct cash outflow involved in the transaction.

It is crucial to distinguish between repairs and capital expenditures. While repairs are considered non-cash items, capital expenditures involve the purchase or improvement of long-term assets and are recorded as cash outflows in the cash flow statement. For instance, if the company decides to upgrade their delivery trucks by purchasing newer models, this would be classified as a capital expenditure and would impact the cash flow.

In summary, repairs are treated as non-cash items in financial reporting because they affect net income but do not involve a direct cash transaction. By separating these non-cash items from the cash flow statement, investors and analysts can gain a clearer understanding of a company's liquidity and financial health.

Cash Investments: Revenue or Not?

You may want to see also

![]()

Repairs as a long-term asset transaction

Repairs and maintenance are essential expenses for a company to restore an asset to its previous operating condition or to maintain its current operating condition. While ordinary repairs are considered regular maintenance, extraordinary repairs are extensive repairs that prolong an asset's useful life and increase its book value.

Extraordinary repairs are treated as capitalized expenses, which means they increase the book value of the fixed asset. They must extend the useful life of the asset beyond one year and be materially significant in value. These repairs are recorded as a debit to the fixed asset account and a credit to accounts payable or cash. This will increase the fixed asset value on the balance sheet and decrease cash or accounts payable.

For example, if a company spends $20,000 on extraordinary repairs to extend the useful life of an asset by four years, the journal entry would be a debit of $20,000 to the fixed asset account and a credit of $20,000 to cash or accounts payable. The depreciation expense for each year would be $5,000 ($20,000/4 years), recorded as a debit to depreciation expense and a credit to accumulated depreciation.

On the other hand, ordinary repairs are treated as operating expenses and are expensed immediately. They are recorded as a debit to the repairs and maintenance expense account and a credit to cash or accounts payable. This type of repair does not extend the useful life of an asset but is necessary to maintain its current operating condition.

It is important to correctly classify repairs as either extraordinary or ordinary, as this will impact the financial statements. Misclassifying repairs as expenses will reduce profit and understate assets, while misclassifying them as assets will increase profit and overstate assets.

In summary, repairs can be classified as long-term asset transactions when they are considered extraordinary repairs that extend the useful life of an asset. These repairs are capitalized and increase the book value of the asset, impacting the company's balance sheet and income statement through depreciation.

Understanding Non-Cash Investing and Financing Activities

You may want to see also

![]()

Repairs as a cash-in item

When considering the financial aspects of maintaining a local license, repairs can be viewed as both a necessary expense and an opportunity to reinvest in the value of that license. Repairs can be categorized as a cash-in item when they are treated as an investment, strategically enhancing the worth of the licensed entity. This perspective is particularly relevant for licenses associated with tangible assets, such as vehicles, equipment, or property, where repairs are essential to maintain functionality, safety, and compliance with regulations.

By investing in repairs, license holders can ensure the continued operation and utilization of their licensed assets. Well-maintained equipment or vehicles tend to have longer lifespans, reducing the need for premature replacement and the associated costs. Regular repairs can also help prevent unexpected breakdowns or failures, minimizing disruptions to business operations and potential losses in productivity or revenue.

From a cash flow perspective, repairs can be managed as a cash-in item by incorporating them into the overall financial planning for the license. This involves setting aside a dedicated budget for repairs and maintenance, ensuring that funds are available when needed. By allocating resources efficiently, license holders can avoid the financial strain of unexpected repair bills and benefit from more predictable cash flow management.

Additionally, repairs can add value to a license by enhancing its marketability and resale potential. Well-maintained assets tend to retain their value better and may even appreciate over time. This is particularly advantageous when the license or asset is transferable or has the potential for future sale. Prospective buyers are often attracted to well-maintained items with a history of proper repairs, as this reduces their risk and the likelihood of incurring immediate repair costs upon acquisition.

Strategic repairs can also lead to cost savings and improved cash flow in the long run. By addressing issues promptly and efficiently, license holders can prevent minor problems from escalating into major, costly repairs. Regular maintenance and timely repairs can optimize the performance of the licensed entity, reducing operating costs associated with inefficiency or increased fuel consumption due to poor maintenance.

In summary, repairs can be considered a cash-in item when they are approached as a strategic investment in the value and longevity of a local license. By allocating resources effectively and treating repairs as a financial priority, license holders can benefit from improved cash flow management, enhanced asset value, and reduced costs associated with unexpected breakdowns or inefficient operations. This perspective highlights the importance of proactive maintenance and the potential for repairs to be a valuable component of financial planning.

Cash App Investing: Free or Fee-Based?

You may want to see also