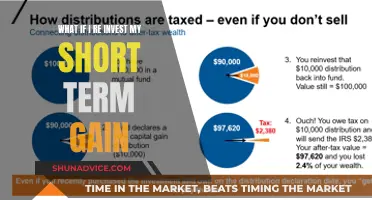

The term for determining the loss beyond further investment is sensitivity analysis. This technique is used to assess the impact of potential changes in input values on the output of a model or system. By varying key variables and observing the resulting changes in the output, analysts can identify the thresholds or tipping points beyond which further investment would lead to losses. Sensitivity analysis is a valuable tool for decision-making, risk management, and understanding the robustness of a project or investment strategy.

What You'll Learn

- Discounted Cash Flow (DCF) Analysis: Evaluating future cash flows and their present value

- Net Present Value (NPV): Measuring the profitability of an investment by comparing cash inflows and outflows

- Internal Rate of Return (IRR): Identifying the rate at which an investment breaks even

- Payback Period: Determining the time it takes for an investment to generate enough cash to cover its initial cost

- Profitability Index (PI): Assessing the profitability of an investment by comparing its present value to its initial cost

![]()

Discounted Cash Flow (DCF) Analysis: Evaluating future cash flows and their present value

Discounted Cash Flow (DCF) analysis is a powerful financial tool used to evaluate the attractiveness of an investment by assessing the future cash flows it will generate and determining their present value. This method is particularly useful for long-term investments, projects, or businesses, as it provides a clear picture of the potential returns and risks associated with an investment over time. The core concept behind DCF analysis is to discount future cash flows to their present value, allowing for a comparison of different investment options on a like-for-like basis.

The process begins with forecasting the future cash flows that an investment will generate. These cash flows can be either incoming (positive cash flows) or outgoing (negative cash flows), such as capital expenditures, operating expenses, or debt payments. It is crucial to be as accurate as possible in these forecasts, as they form the basis of the entire analysis. Once the cash flow stream is determined, the next step is to select an appropriate discount rate, which represents the cost of capital or the minimum rate of return an investor expects. This discount rate is applied to each future cash flow to calculate its present value. The present value of a cash flow is a measure of its worth at the current time, taking into account the time value of money.

Mathematically, the present value (PV) of a future cash flow can be calculated using the formula: PV = CF / (1 + r)^n, where CF is the cash flow, r is the discount rate, and n is the number of periods until the cash flow is received. By applying this formula to each cash flow in the forecast, you can determine the total present value of the future cash flows. The sum of these present values represents the net present value (NPV) of the investment, which is a key metric in DCF analysis. A positive NPV indicates that the investment is expected to generate returns greater than the cost of capital, while a negative NPV suggests a potential loss beyond further investment.

DCF analysis also provides insights into other important financial metrics. For instance, the internal rate of return (IRR) can be calculated, which is the discount rate at which the NPV of the investment becomes zero. The IRR represents the project's expected annualized rate of return. Additionally, the analysis can be used to determine the payback period, which is the time it takes for the cumulative cash inflows to cover the initial investment. These metrics collectively help investors and analysts make informed decisions about the viability of an investment.

In summary, Discounted Cash Flow analysis is a comprehensive approach to evaluating investments by assessing future cash flows and their present value. It enables investors to make informed choices, compare investment opportunities, and determine the potential profitability of a venture. By considering the time value of money and applying appropriate discount rates, DCF analysis provides a robust framework for financial decision-making, especially in complex and long-term investment scenarios.

Navigating Cash Flow: Short-Term Investments: A Balanced Approach

You may want to see also

![]()

Net Present Value (NPV): Measuring the profitability of an investment by comparing cash inflows and outflows

Net Present Value (NPV) is a financial metric used to determine the profitability of an investment by comparing the present value of cash inflows to the present value of cash outflows over a specified period. It is a powerful tool for evaluating the financial viability of projects or investments, providing a clear picture of the potential return on investment. NPV takes into account the time value of money, which means that cash received today is worth more than the same amount received in the future due to its potential earning capacity.

The calculation of NPV involves several steps. First, you need to estimate the future cash flows that the investment will generate, including both the initial investment and the expected cash receipts over the investment's lifetime. These cash flows are then discounted to their present value using an appropriate discount rate, which represents the cost of capital or the minimum rate of return expected by investors. The discount rate is crucial as it reflects the time value of money and the risk associated with the investment.

Next, you sum up the present values of all the cash inflows and outflows to arrive at the NPV. If the NPV is positive, it indicates that the investment is expected to generate returns greater than the initial investment and the cost of capital, making it an attractive option. Conversely, a negative NPV suggests that the investment may result in losses beyond the initial investment, and further investment in that project may not be financially prudent.

The concept of NPV is particularly useful in capital budgeting decisions, where companies evaluate multiple investment opportunities. By comparing the NPVs of different projects, businesses can identify the most profitable ventures. Projects with a higher NPV are generally preferred as they are expected to provide greater value to the company. This analysis helps organizations make informed decisions about resource allocation and long-term growth strategies.

In summary, Net Present Value (NPV) is a critical financial concept for assessing investment opportunities. It provides a quantitative measure of the profitability of an investment by evaluating the present value of cash flows. By considering the time value of money and the cost of capital, NPV enables businesses to make sound financial decisions, ensuring that investments are aligned with the organization's goals and objectives. Understanding NPV is essential for anyone involved in financial analysis and investment management.

Navigating the Game of Life: Unlocking Long-Term Investment Strategies

You may want to see also

![]()

Internal Rate of Return (IRR): Identifying the rate at which an investment breaks even

The Internal Rate of Return (IRR) is a financial metric used to evaluate the profitability of an investment. It is a crucial tool for investors and analysts to determine the rate at which an investment project is expected to generate returns that exceed the cost of the investment. In simpler terms, IRR identifies the point at which an investment's net present value (NPV) is zero, indicating that the investment has reached its break-even point.

To calculate IRR, you need to follow a step-by-step process. First, you must determine the initial investment amount and the expected cash flows at regular intervals. These cash flows can be either incoming or outgoing and are typically represented as a series of positive and negative values. The next step involves discounting these cash flows to their present value using a predetermined discount rate. This discount rate is often the cost of capital or the minimum acceptable rate of return for the investment. By doing so, you can compare investments with different time horizons and assess their profitability.

The IRR is then calculated as the discount rate that makes the NPV of the investment equal to zero. It is the rate at which the investment's future cash flows, when discounted, equal the initial investment cost. For example, if an investment has an IRR of 15%, it means that the investment is expected to generate a 15% return on the initial investment amount.

It's important to note that IRR has certain limitations. One of the main drawbacks is that it doesn't consider the time value of money over multiple periods. Additionally, IRR may not accurately reflect the true profitability of an investment, especially when comparing projects of different durations. In such cases, other metrics like Net Present Value (NPV) or Payback Period can provide a more comprehensive analysis.

In summary, the Internal Rate of Return (IRR) is a valuable tool for assessing investment opportunities. It helps investors identify the break-even point and the potential rate of return. However, it should be used in conjunction with other financial metrics to make well-informed investment decisions, especially when dealing with complex projects and long-term investments. Understanding and applying IRR can significantly contribute to evaluating and managing investment portfolios effectively.

Understanding Investment Liabilities: A Comprehensive Guide for Investors

You may want to see also

![]()

Payback Period: Determining the time it takes for an investment to generate enough cash to cover its initial cost

The Payback Period is a crucial financial metric used to evaluate the profitability and efficiency of an investment. It represents the time required for an investment to generate enough cash inflows to cover its initial cost or outlay. This method of analysis is particularly useful for assessing the short-term viability of an investment and its potential to recover the initial investment amount.

To calculate the Payback Period, you need to determine the total cash inflows generated by the investment over time and then identify the point at which these cash inflows equal the initial investment cost. This can be done by dividing the initial investment by the annual cash inflows. For example, if an investment yields a cash inflow of $5,000 per year and the initial investment is $20,000, the Payback Period would be 4 years ($20,000 / $5,000 = 4).

This metric is valuable for investors and business owners as it provides a quick assessment of the investment's liquidity and its ability to recover capital. A shorter Payback Period indicates a more efficient investment, as it takes less time for the investment to pay for itself. This is especially important for projects or ventures that require immediate returns or for investors seeking quick capital recovery.

However, it's important to note that the Payback Period has its limitations. It doesn't consider the time value of money, which means that cash inflows received later in the investment's life may be worth less than those received earlier. Additionally, it doesn't provide information about the investment's profitability beyond the payback period, as it only focuses on the recovery of the initial investment.

To address these limitations, investors often use the Payback Period in conjunction with other financial metrics such as the Internal Rate of Return (IRR) and the Net Present Value (NPV). These metrics provide a more comprehensive analysis by considering the time value of money and the overall profitability of the investment over its entire lifespan. By combining these methods, investors can make more informed decisions and better assess the potential of their investments.

Trading Investment: Navigating Short-Term Gains or Long-Term Wealth

You may want to see also

![]()

Profitability Index (PI): Assessing the profitability of an investment by comparing its present value to its initial cost

The Profitability Index (PI), also known as the Benefit-Cost Ratio, is a financial metric used to evaluate the viability of a project or investment. It provides a clear indication of the profitability of an investment by comparing its present value (PV) to its initial cost. This ratio is particularly useful for assessing the attractiveness of different investment opportunities, especially when multiple projects are being considered.

To calculate the PI, you divide the present value of the future cash flows of an investment by its initial investment cost. The formula is:

PI = (Present Value of Future Cash Flows) / (Initial Investment Cost)

A PI value greater than 1 indicates that the investment is profitable, as the present value of the cash flows exceeds the initial cost. For example, if a project has a PI of 1.5, it means that for every dollar invested, the project will generate $1.50 in value over time. This is a strong indicator of a successful and profitable venture.

On the other hand, a PI less than 1 suggests that the investment may not be financially viable. In this case, the present value of the cash flows is lower than the initial investment, resulting in a loss. For instance, a PI of 0.8 means that the project will generate $0.80 for every dollar invested, indicating a potential loss.

The PI is a valuable tool for decision-making as it provides a standardized way to compare different investment options. It allows investors and analysts to quickly assess the relative profitability of various projects, helping them make informed choices. By considering the PI alongside other financial metrics, such as the Internal Rate of Return (IRR), investors can gain a comprehensive understanding of the potential outcomes of their investments.

In summary, the Profitability Index is a critical concept in investment analysis, offering a straightforward method to determine the profitability of an investment. It enables investors to make informed decisions by providing a clear comparison of the present value of cash flows to the initial investment cost, thus facilitating the identification of successful and unprofitable ventures.

Understanding Long-Term Investment Strategies: Key Features and Benefits

You may want to see also

Frequently asked questions

The term you are looking for is "Opportunity Cost." This concept refers to the value of the next best alternative that is foregone when a decision is made. In the context of investment, it represents the potential returns or benefits that could have been gained by choosing a different investment option.

Opportunity Cost can be calculated by comparing the returns or benefits of the chosen investment against the returns or benefits of the next best alternative. It is essentially the difference in value between the two options. For example, if you invest in Stock A and could have instead invested in Stock B, the Opportunity Cost would be the potential returns of Stock B minus the actual returns of Stock A.

Let's say you have $10,000 to invest and decide to put it into a high-risk, high-reward stock. At the same time, you could have used that money to buy a government bond, which is generally considered a safer investment. If the stock returns 20% in a year, but the bond yields 5%, the Opportunity Cost of choosing the stock over the bond is 15% (20% - 5%). This means you could have earned an additional 15% by choosing the bond.

Understanding Opportunity Cost is crucial because it helps investors make more informed choices. By considering the potential losses or benefits of alternative investments, investors can assess the true cost of their decisions. This awareness can lead to better risk management, more balanced portfolios, and a clearer understanding of the trade-offs involved in investment strategies.