Investing can be a daunting task, especially if you are unsure about what you are doing. This is where investment advisors come in. They can help you manage your money and plan for the future, but it is important to choose the right one. There are several red flags to be aware of when selecting an investment advisor, such as them doing most of the talking, not being transparent about their fees, background, and credentials, and you not trusting them. On the other hand, a green flag is an advisor who asks for your tax returns and acts as a fiduciary, meaning they have a legal duty to act in your best interest. While it is possible to invest without the help of an advisor, seeking advice from a financial expert can help you stay on track and make informed choices.

What You'll Learn

![]()

The benefits of using a financial advisor

Using a financial advisor can bring numerous benefits, from creating a comprehensive financial strategy to acting as a "project manager" for your investments and other financial goals. Here are some key advantages to consider:

Comprehensive Financial Strategy:

Financial advisors can provide a holistic approach to your finances, considering your entire financial picture, including investments, insurance, estate planning, and more. They can help you develop a customised, comprehensive plan that aligns with your short-term and long-term goals, risk tolerance, and personal values.

Strategy Based on Your Needs:

A good financial advisor listens to your unique needs and tailors their advice accordingly. They act as project managers, guiding you through various financial aspects, such as investments, Medicare, long-term care, Social Security, and more. They can also help you stick to your financial plan during turbulent times, providing discipline and emotional support.

Time and Freedom:

By offloading the stress of managing your finances to a financial advisor, you gain freedom and time to focus on what you love doing. A financial advisor can save you from the administrative headaches of managing investments, tax returns, estate planning, and other complex financial tasks.

Emotional Guardrails:

A financial advisor can provide emotional guardrails, helping you make rational financial decisions by reminding you of your long-term plan and goals. They can help you avoid rash decisions driven by fear or excitement, especially during volatile market conditions.

Champion for Your Success:

A dedicated financial advisor gets to know you, your family, your dreams, and your goals. They are invested in your success and can provide valuable support and encouragement throughout your financial journey. They can help you navigate complex financial landscapes and make decisions with confidence.

Plan for the Unexpected:

Life is full of surprises, and a financial advisor can help you prepare for the unexpected. They guide you in planning for accidents, market downturns, job losses, property damage, major illnesses, and other unforeseen events, ensuring that you stay on track financially despite life's challenges.

Limit Tax Liabilities:

Financial advisors can help you navigate the complex world of taxes. They can identify taxable accounts, assist with tax-loss harvesting, and guide you through changing tax laws and regulations to minimise penalties and maximise your wealth.

Long-Term Relationship:

Building a long-term relationship with a financial advisor you trust is invaluable. Over time, they gain a deeper understanding of your financial goals and personal situation, enabling them to provide more accurate and tailored advice. This relationship can provide peace of mind and support your overall well-being.

Calculating Initial Investment: Using IRR to Guide Decisions

You may want to see also

![]()

How to choose a financial advisor

A financial advisor can help you manage your money and reach your financial goals. Here are some steps to help you choose the right one for you:

Identify your financial needs:

Before starting your search, reflect on what you want from the relationship with your financial advisor. Financial advisors provide a wide range of services, from holistic help with savings goals and budgeting to specialised advice on investing, debt, tax strategy, retirement, or estate planning.

Know what credentials to look for:

Financial advisors go by many names, but not all titles are tied to specific credentials. Look for advisors with fiduciary duty, which means they are obligated to act in their client's best interest. Credentials to look out for include Certified Financial Planner (CFP) and Registered Investment Advisors (RIA).

Review financial advisor service types:

There are several ways to get financial advice, including robo-advisors, online financial planners, and traditional, in-person financial planners. The right option will depend on your preferences, the services you need, and your budget.

Consider the cost:

Financial advisors have a reputation for being expensive, but there are options for every budget. Robo-advisors are usually the cheapest option, followed by online financial planners, and then traditional financial advisors, which are often the most costly.

Research their background:

It's important to vet the advisor's credentials and experience. Check their Form ADV, employment record, and disciplinary history.

Set up a first meeting:

Once you've narrowed down your options, set up an initial meeting to discuss your financial situation, goals, risk tolerance, and communication style. This will help you decide if the advisor is a good fit.

Ask questions:

Practical questions about the services offered, investment products, client communication, and available tools and resources can help you understand how the advisor runs their business. Relational questions about their investing approach and your financial goals can also help ensure you and the advisor are a good match.

Hire the financial advisor:

If you're happy with the advisor's background and feel they are a good match, you can start working with them. This will typically involve signing a contract and legal documents, providing financial information, and having follow-up conversations.

Alpari Invest: A Guide to Getting Started and Making Profits

You may want to see also

![]()

When to be cautious of a financial advisor

While a financial advisor can be a great asset to help you manage your money, it's important to be cautious and do your research before hiring one. Here are some red flags to look out for when considering a financial advisor:

- Lack of professional designations: Anyone can call themselves a financial advisor, so it's important to look for professional designations such as CFP (Certified Financial Planner), CFA (Chartered Financial Analyst), or CPA (Certified Public Accountant). These designations indicate that the advisor has met certain educational, ethical, and experience standards.

- Not acting as a fiduciary: A fiduciary is legally obligated to act in their client's best interests. If a financial advisor is not upfront about whether they act as a fiduciary, or if they change hats and sell you products that only meet a suitability requirement, be cautious.

- Aggressively pushing investment products: Be wary of advisors who seem more interested in selling you investment products than giving you unbiased advice. A good advisor will take the time to understand your financial goals and risk tolerance before making any recommendations.

- Unresponsive to inquiries: A financial advisor should be responsive and communicative. If you find yourself waiting a long time for responses or not getting clear answers to your questions, it may be a red flag.

- Lack of transparency about fees: Financial advisors can charge fees in different ways, such as a percentage of assets under management, an hourly rate, or a fixed fee. Be cautious of advisors who are not upfront about how they charge for their services.

- High-pressure sales tactics: Be wary of advisors who use high-pressure sales tactics to get you to make decisions without giving you time to consider your options. A good advisor will give you the space to make informed choices.

Remember, it's important to do your due diligence before hiring a financial advisor. Ask for referrals from friends and family, interview multiple candidates, and always check their credentials and regulatory status.

EM Cash: Investing Strategies for Beginners

You may want to see also

![]()

The importance of investing early

Investing early is important because it allows you to harness the power of compound interest. Compound interest is the phenomenon of earning interest on interest. The earlier you start putting money away, the less you will need to contribute later, and the more time your money has to grow. For example, if you invest $1,000 in an account with a 10% annual return, you will earn $100 in interest in the first year, and $110 in the second year (assuming the same rate of return). These annual gains add up significantly over time.

Another benefit of investing early is that it allows you to take calculated risks. When you are young, you can afford to take on more risk because you have more time to recover from any potential losses. This can lead to higher returns on your investments.

Investing early also means that you will not need to contribute as much later on. For example, if you start investing at 20 years old and invest $250 each month with an 8% annual rate of return, by the time you reach 65, over 50% of your total portfolio will have come from money that you invested in your 20s.

In addition to the financial benefits, investing early can also give you peace of mind. It can be stressful to think about saving enough money for retirement, but by starting early, you can be confident that you are on the right track. It also allows you to take a long-term view of your investments and not worry about short-term market fluctuations.

Finally, investing early gives you more flexibility in your investment choices. When you start early, you have the option to invest in riskier assets that have the potential for higher returns. You can also take advantage of tax-advantaged investment vehicles such as 401(k)s, 403(b)s, and IRAs, which offer tax benefits that can help your savings grow even more.

In summary, investing early is important because it allows you to take advantage of compound interest, take calculated risks, contribute less overall, and have more flexibility in your investment choices. It also gives you the peace of mind that comes with knowing you are on track for a comfortable retirement.

Investment Casting: Art of Molding Liquid Metals

You may want to see also

![]()

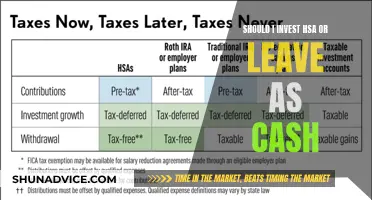

The risks of holding cash

Holding cash might feel like the safest option, but it can introduce new risks. Here are some of the dangers of holding too much cash:

Inflation

Inflation is a silent killer of cash holdings. It is defined by the Federal Reserve as "the increase in the prices of goods and services over time". While you won't lose dollars by holding cash, you will lose significant spending power. Inflation can deteriorate your purchasing power over time, and cash does not generate returns to combat this loss.

Opportunity Cost

By holding cash, you are foregoing potential returns from other investments. Historical data shows that stocks have outperformed cash in 59% of months and 73% of years since 1928. Holding cash means you risk missing out on substantial market gains, which could hurt your long-term investing goals.

Reinvestment Risk

Existing interest rates on cash instruments may not last. Most economists expect short-term interest rates to decline, and if rates drop significantly, those holding cash will either continue to lose to inflation or be forced to reinvest in stocks and bonds at higher prices.

Poor Timing Decisions

Holding cash can lead to emotional and impulsive investment decisions. For example, you may fear volatility or a market downturn and decide to hold cash until stocks are at a bargain. However, this strategy rarely works out, as it is extremely difficult to time the market correctly. You may end up buying stocks at a high or missing out on market gains, ultimately impacting your long-term financial goals.

Subpar Returns

Cash yields are likely to be significantly lower when existing cash instruments mature, making reinvesting challenging. Historical data shows that stocks and bonds have generated higher returns than cash over time.

While holding some cash is essential for emergency funds or short-term needs, holding too much cash beyond these requirements can introduce risks to your financial plan.

Ally Invest App: A User's Guide to Trading

You may want to see also